Neural Networks — ML Signal Framework

I am going to break down how hedge funds use neural networks to extract edge before the trade even happens & share the exact implementation framework you can build today. Let’s get straight to it.

Bookmark This - I’m Roan, a backend developer working on system design, HFT-style execution, and quantitative trading systems. My work focuses on how prediction markets actually behave under load. For any suggestions, thoughtful collaborations, partnerships DMs are open.

The way most traders lose money has nothing to do with their market thesis. They are right about direction more often than they think. The problem is they are operating on one signal, one indicator, one gut feeling. They are making probability decisions without a probability framework. And markets punish that mistake reliably and repeatedly. Neural networks solve a fundamentally different problem. They do not predict the future. What they do is learn the expectation function hidden inside historical data. The mathematical relationship between what you can observe right now and what the market is statistically most likely to do next. And they do this across thousands of variables simultaneously in ways no human eye can see and no single indicator can capture.

The largest funds already know this. Two Sigma runs over 10,000 live signals through machine learning models simultaneously. Citadel’s quantitative research division deploys deep learning architectures across equity, options, and macro strategies. Renaissance Technologies built the Medallion Fund entirely on this framework decades before anyone else understood what they were doing. The fund returned 66 percent annually before fees over 30 years. That is not luck. That is the systematic application of statistical learning at scale.

The entry level quant researcher building these models at those firms earns between $350,000 and $650,000 in total compensation. Not because the job is glamorous. Because finding a reliable edge in financial data using mathematics is genuinely one of the hardest unsolved problems in applied science.

If you have not yet read the complete quant roadmap covering the mathematical foundation underneath everything in this article, start there first.

Apr 28

AI and machine learning hiring in quantitative finance accelerated sharply through 2025. Every major systematic fund is building signal generation infrastructure powered by deep learning. And yet most traders who try to implement neural networks into their strategy fail at the same predictable step for the same predictable reason.

This article tells you exactly what that step is and exactly how to avoid it. Then it gives you the complete implementation framework from data preparation through live signal deployment.

By the end of this article you will understand exactly how neural networks learn from data and what they are actually computing when they make a prediction, why applying them directly to price charts is guaranteed to fail and what the correct input is, which architecture works best for sequential market data and why, the complete rigorous training framework that separates real edge from self-deception and the full implementation pipeline to deploy your first neural network trading signal.

Note: This article is deliberately long. Every part builds on the one before it. If you are serious about adding a genuine quantitative edge to your trading, read every single word. If you are looking for a shortcut, this is not for you.

Part 1: What a Neural Network Actually Computes

Before you build anything, you need to understand what is actually happening when a neural network trains on data. Most explanations skip this and go straight to code. That is why most implementations fail.

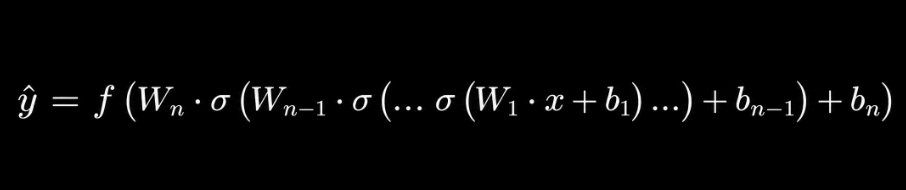

A neural network is a parameterized composite function. You give it a vector of inputs. It applies a sequence of linear transformations interleaved with non-linear activation functions. It produces an output. The formal structure is:

Where W_i are weight matrices, b_i are bias vectors, and σ is a non-linear activation function applied element-wise. This is the mathematical reality underneath every neural network regardless of how it is visualized.

The power is in training. You have a dataset of input-output pairs. The network starts with random parameters. It makes a prediction. It computes the error between that prediction and the actual observed output. It adjusts the parameters in the direction that reduces the error. It repeats this millions of times.

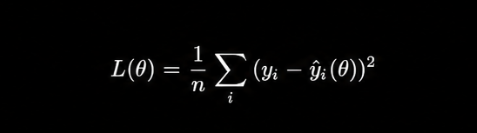

The formal objective is minimizing a loss function. For regression tasks the standard choice is mean squared error:

Where θ represents all learnable parameters, yᵢ is the actual observed value, and ŷᵢ is the model prediction. The optimization proceeds by computing the gradient of the loss with respect to the parameters and taking a step in the negative gradient direction: θ ← θ - α · ∇_θ L(θ) Where α is the learning rate. This is stochastic gradient descent. Every modern deep learning optimizer is a variation of this with adaptive step sizes, momentum terms, or second-order approximations layered on top.

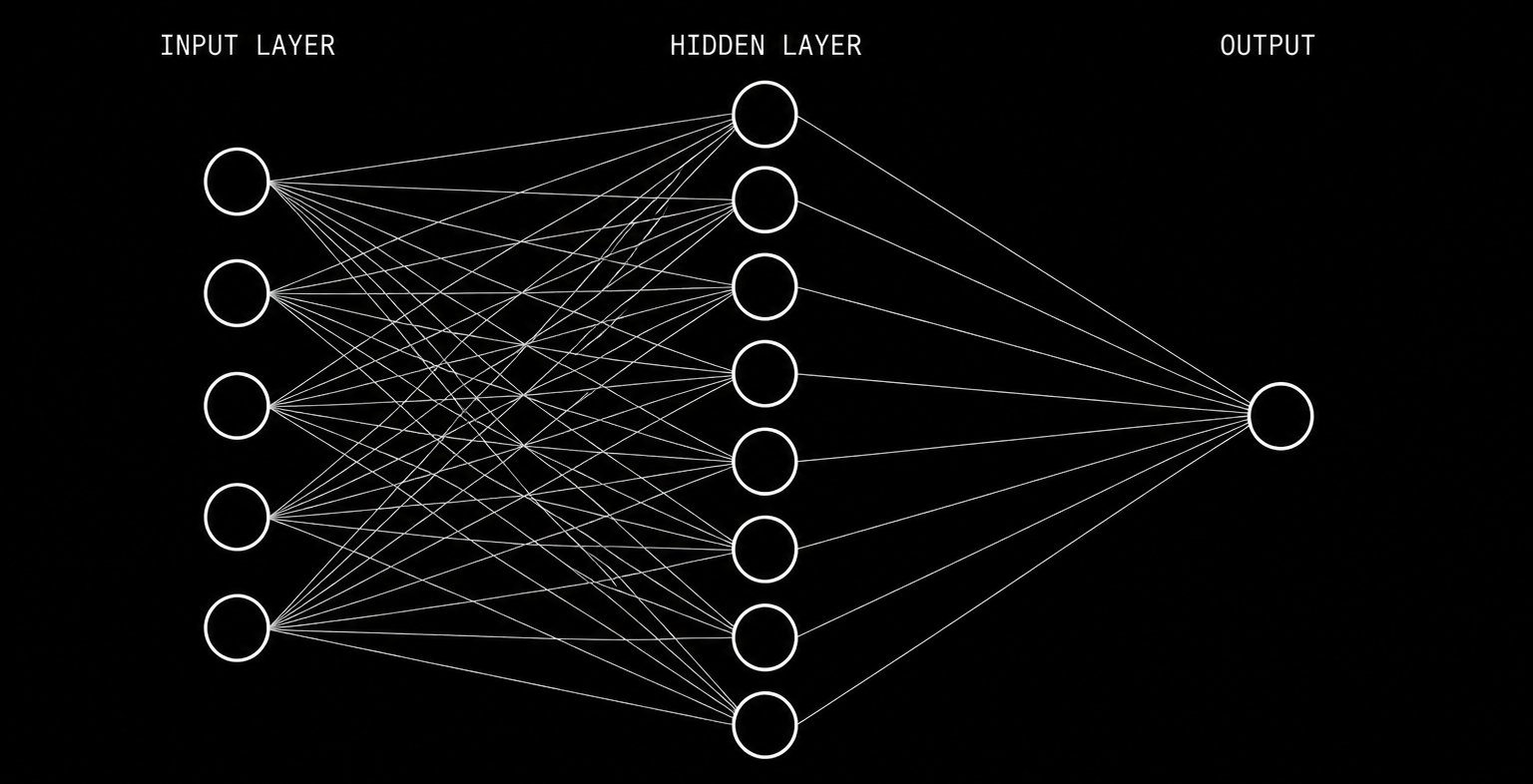

A feedforward neural network passes inputs through weighted layers to produce an output that approximates the conditional expectation of the target variable.

Now here is the insight that changes how you interpret everything a neural network produces.

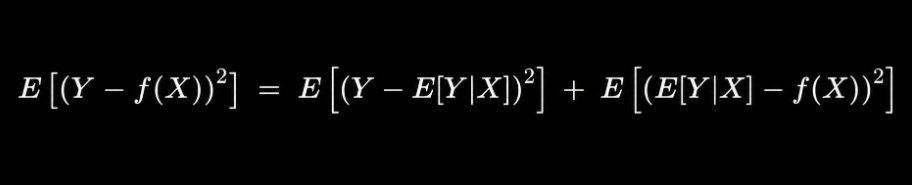

When you train a network to minimize squared error against a target variable, what does it learn? It learns the conditional expectation of that variable given your inputs. The function that minimizes E[(Y - f(X))²] is exactly E[Y|X]. This is not a prediction in the colloquial sense. It is a mathematical expectation. The weighted average outcome across all scenarios consistent with the observed inputs.

The proof of this is straightforward. Expand the squared loss:

The first term is irreducible variance. The second term is minimized by setting f(X) = E[Y|X]. The optimal predictor under squared error is the conditional mean.

This has a profound practical implication. When you roll a fair die 10,000 times and train a neural network to minimize squared error against the outcomes, it will predict 3.5. Can a die land on 3.5? No. But 3.5 is the value that minimizes the expected squared error. The network is computing the expectation, not the next realization.

Why does neural networks specifically outperform simpler models at learning this conditional expectation? The universal approximation theorem. A feedforward network with a single hidden layer containing sufficient neurons can approximate any continuous function on a compact subset of Rⁿ to arbitrary precision. For deep networks with multiple layers, the approximation becomes exponentially more efficient in terms of the number of parameters required.

This means: if there is any smooth mathematical relationship between your input features and your target variable, a properly architected neural network can find it. The question is never whether the network can learn the function. The question is whether the function you want it to learn is actually stable enough across time to be worth learning.

Part 2: Why Price Prediction Fails and What to Do Instead

This is the most important section in the article. The mistake described here is made by virtually every trader who tries to implement neural networks for the first time. Understanding why it fails is the prerequisite for everything that works.

The failure mode is this: take 500 days of closing prices, feed them into an LSTM, ask it to predict day 501.

In-sample, the predictions look smooth and close to actual prices. Out-of-sample, the model predicts something roughly constant or reverts to a recent mean while prices move somewhere completely different. The model appears to have learned nothing useful.

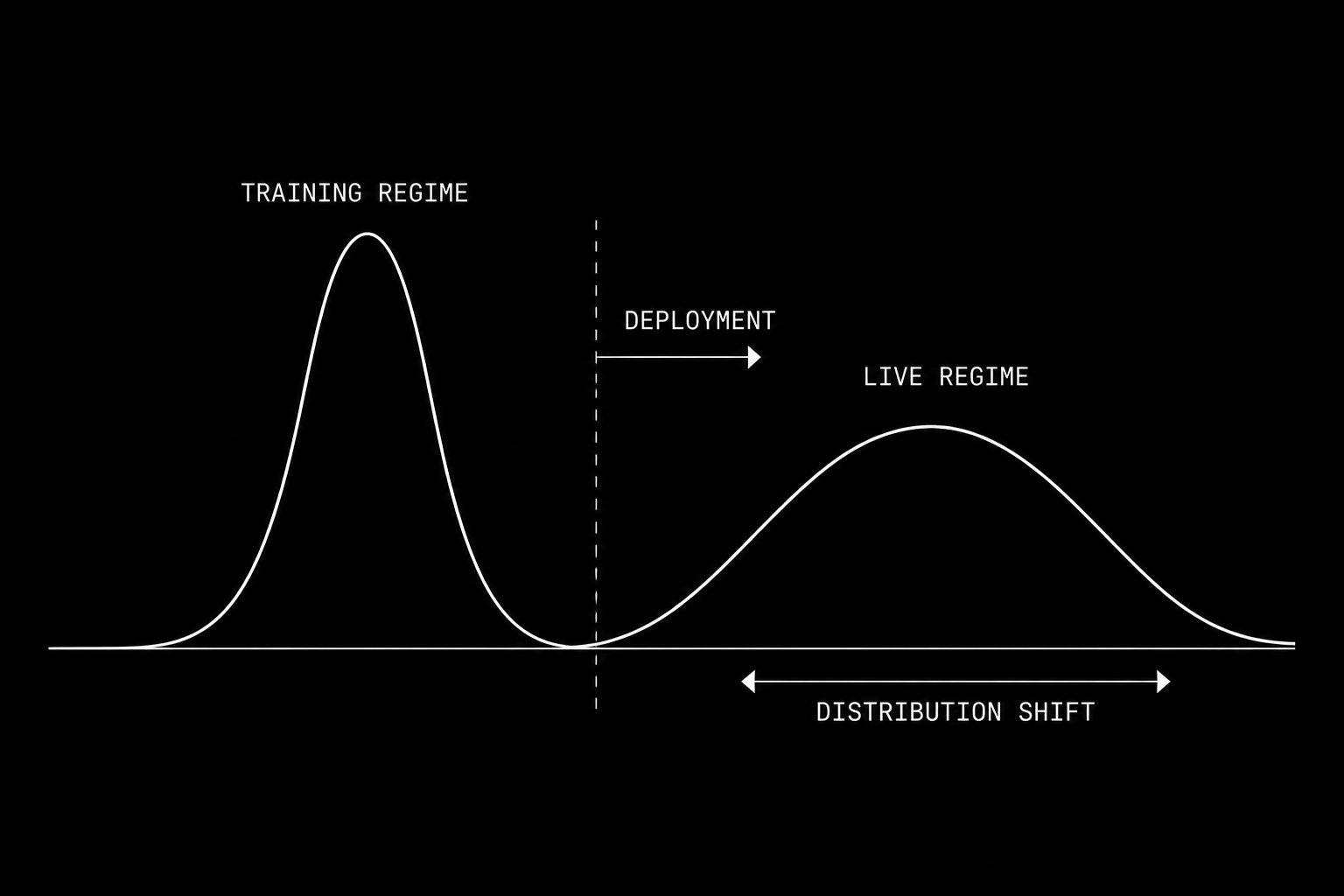

This is not a model failure. It is a data distribution failure.

The distribution governing market returns shifts continuously over time. A model trained on the left regime learns the wrong expectation function for the right regime.

Recall from Part 1: a neural network learns E[Y|X], the conditional expectation of Y given X. This expectation is only meaningful if the data generating distribution P(Y|X) is stable over time. If that distribution shifts, the conditional expectation the model learned from historical data no longer describes the expectation in the present.

Formally, this is the problem of non-stationarity. A time series {Xₜ} is stationary if its joint distribution P(Xₜ₁, Xₜ₂, …, Xₜₙ) is invariant to time shifts. Financial price series are non-stationary in the strongest possible sense. The distribution governing equity returns in 2008 is structurally different from the distribution governing them in 2021. Mean, variance, autocorrelation, and tail behavior all shift as a function of regime, liquidity, volatility clustering, and macro conditions.

The consequence is visible in any backtest of a price-predicting neural network. The model trained on 2015 to 2019 data learns the expectation structure of that regime. When the distribution shifts in 2020, the model is fitting a moving target. Its predictions are always wrong in a systematic way that reveals it is modeling the past distribution, not the present one.

What is the solution?

Feature engineering to produce stationary or near-stationary inputs. The target variable itself should also be constructed to be approximately stationary.

For inputs, the features that have exhibited reasonable stationarity across market regimes include:

Log returns over multiple windows: r_t = ln(P_t / P_{t-k}) for k in {1, 5, 20}

Volatility ratios: σ_short / σ_long where each σ is rolling realized volatility over different windows

Momentum signals normalized by volatility: r_t / σ_t, the return scaled by realized risk

Volume z-score: (V_t - μ_V) / σ_V computed over a rolling window

Spread-based signals: bid-ask spread relative to its historical distribution, or effective spread computed from trade price versus midpoint

Regime indicators: VWAP deviation, distance from rolling high and low, implied versus realized volatility ratio

For the target variable, instead of predicting next period price, predict next period direction as a binary classification problem: will the risk-adjusted return be positive? Or predict next period return z-scored against its recent distribution. Both targets are more stable than raw price or even raw return.

The practical test for whether a feature is useful: run an augmented Dickey-Fuller test on it. A p-value below 0.05 suggests the series is stationary. For features that fail this test, first-difference them or normalize by a rolling standard deviation.

Implementation note: In Python, this looks like:

from statsmodels.tsa.stattools import adfuller

import numpy as np

def check_stationarity(series, name):

result = adfuller(series.dropna())

print(f"{name}: ADF statistic={result[0]:.4f}, p-value={result[1]:.4f}")

return result[1] < 0.05

**Example: Feature Engineering**

returns = df['close'].pct_change()

vol_20 = returns.rolling(20).std()

vol_5 = returns.rolling(5).std()

features = {

'return_1d': returns,

'return_5d': df['close'].pct_change(5),

'vol_ratio': vol_5 / vol_20,

'momentum': returns / vol_20,

'volume_zscore': (df['volume'] - df['volume'].rolling(20).mean()) / df['volume'].rolling(20).std()

}

for name, series in features.items():

is_stationary = check_stationarity(series, name)

Every feature that fails the stationarity test is a feature that will cause your model to learn the wrong distribution.

Part 3: The LSTM Architecture for Sequential Market Data

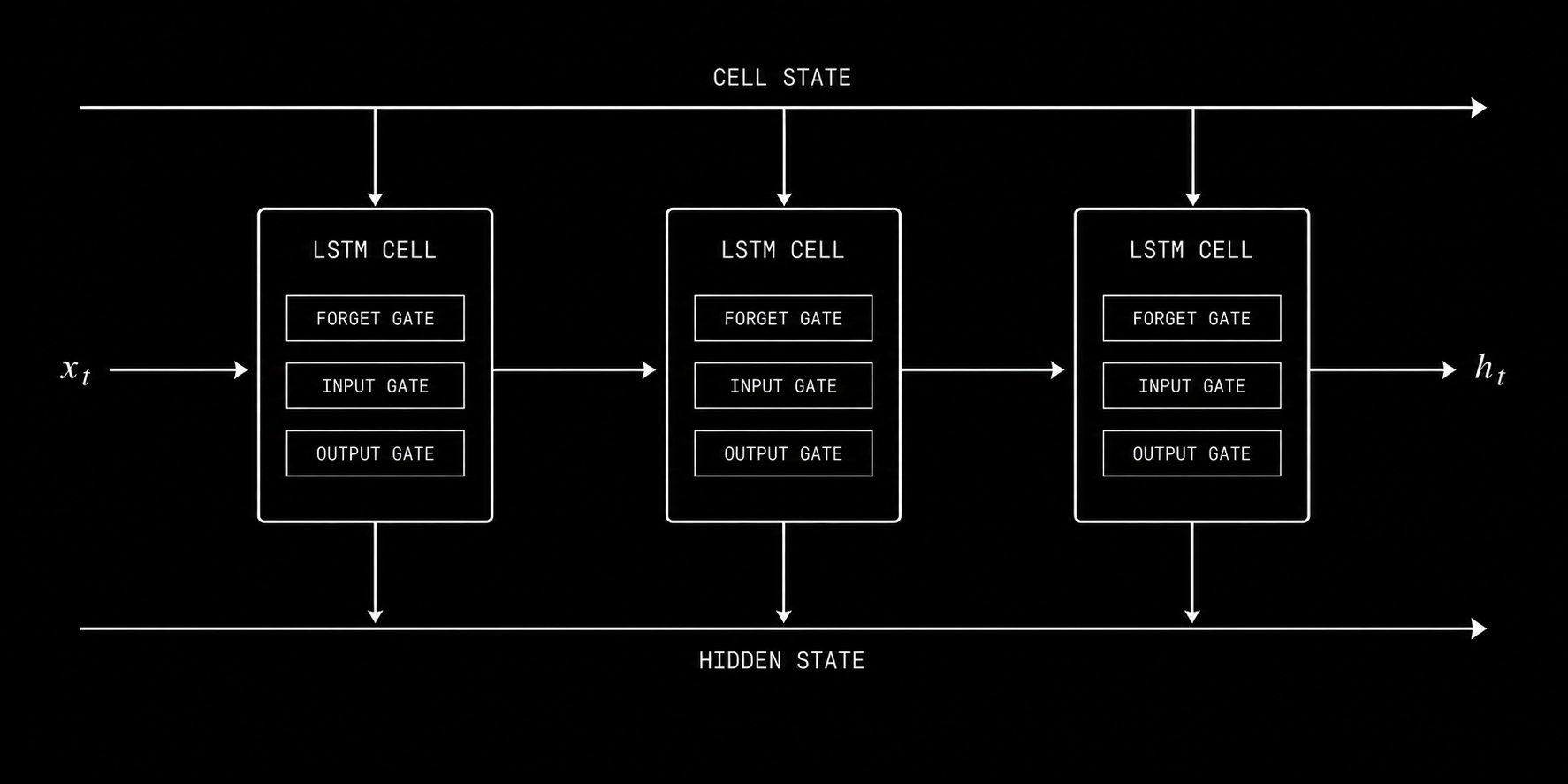

The LSTM forget gate, input gate, and output gate control what information persists across time steps, allowing the model to maintain context across weeks of market data.

Market data is sequential. The order of events carries information that a snapshot does not. What happened in the last five minutes is connected to what happens in the next five minutes through autocorrelation, momentum, mean reversion, and microstructure dynamics. The architecture you use must be capable of learning from this sequential structure.

A standard feedforward network treats every input independently. When you present it with day 100’s feature vector, it has no knowledge of what days 1 through 99 looked like. For non-sequential data like the football throwing example from Part 1, this is fine. For time series data from financial markets, it throws away the most important information in your dataset.

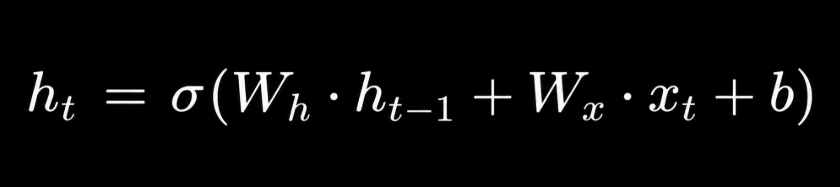

The Recurrent Neural Network addresses this by passing a hidden state forward through time. At each time step t, the hidden state h_t is computed as:

The hidden state encodes everything the network has learned from steps 1 through t-1 and combines it with the current input x_t. This is the memory mechanism. But basic RNNs suffer from the vanishing gradient problem: gradients diminish exponentially as they are backpropagated through time, making it effectively impossible to learn dependencies across more than a few time steps.

LSTM solves this with a gated memory architecture. Rather than a single hidden state, the LSTM maintains both a hidden state h_t and a cell state c_t. The cell state is the long-term memory. The hidden state is the working memory. Three learned gates control information flow:

Forget gate: f_t = σ(W_f · [h_{t-1}, x_t] + b_f) This gate decides what fraction of the previous cell state to discard. When markets transition between regimes, the forget gate allows the model to release outdated patterns and reset its understanding.

Input gate: i_t = σ(W_i · [h_{t-1}, x_t] + b_i), g_t = tanh(W_g · [h_{t-1}, x_t] + b_g) These gates decide what new information to write into the cell state.

Output gate: o_t = σ(W_o · [h_{t-1}, x_t] + b_o), h_t = o_t ⊙ tanh(c_t) This gate decides what to output from the cell state.

The cell state update combines forgetting and new writing: c_t = f_t ⊙ c_{t-1} + i_t ⊙ g_t

This architecture allows LSTM to maintain relevant context across sequences of 50, 100, or more time steps without the gradient vanishing problem. For daily trading strategies, this means the model can learn that a particular pattern of volatility compression three weeks ago predicts a specific type of breakout behavior today. No indicator-based system can capture relationships at that complexity.

Complete LSTM implementation in PyTorch:

import torch

import torch.nn as nn

import numpy as np

from sklearn.preprocessing import StandardScaler

class TradingLSTM(nn.Module):

def __init__(self, input_size, hidden_size=64, num_layers=2, dropout=0.2):

super(TradingLSTM, self).__init__()

self.hidden_size = hidden_size

self.num_layers = num_layers

self.lstm = nn.LSTM(

input_size=input_size,

hidden_size=hidden_size,

num_layers=num_layers,

dropout=dropout,

batch_first=True

)

self.dropout = nn.Dropout(dropout)

self.fc = nn.Linear(hidden_size, 1)

self.sigmoid = nn.Sigmoid()

def forward(self, x):

h0 = torch.zeros(self.num_layers, x.size(0), self.hidden_size)

c0 = torch.zeros(self.num_layers, x.size(0), self.hidden_size)

out, _ = self.lstm(x, (h0, c0))

out = self.dropout(out[:, -1, :])

out = self.fc(out)

return self.sigmoid(out)

def prepare_sequences(features, target, lookback=10):

X, y = [], []

for i in range(len(features) - lookback):

X.append(features[i:i+lookback])

y.append(target[i+lookback])

return np.array(X), np.array(y)

The lookback period is a critical hyperparameter. For daily strategies, start with a window of 10 to 20 trading days. For intraday strategies operating on 5-minute bars, a lookback of 24 periods covers two trading hours of context. The optimal lookback depends on the timescale of the patterns you are trying to capture and must be determined empirically through validation performance.

Part 4: Training Without Fooling Yourself

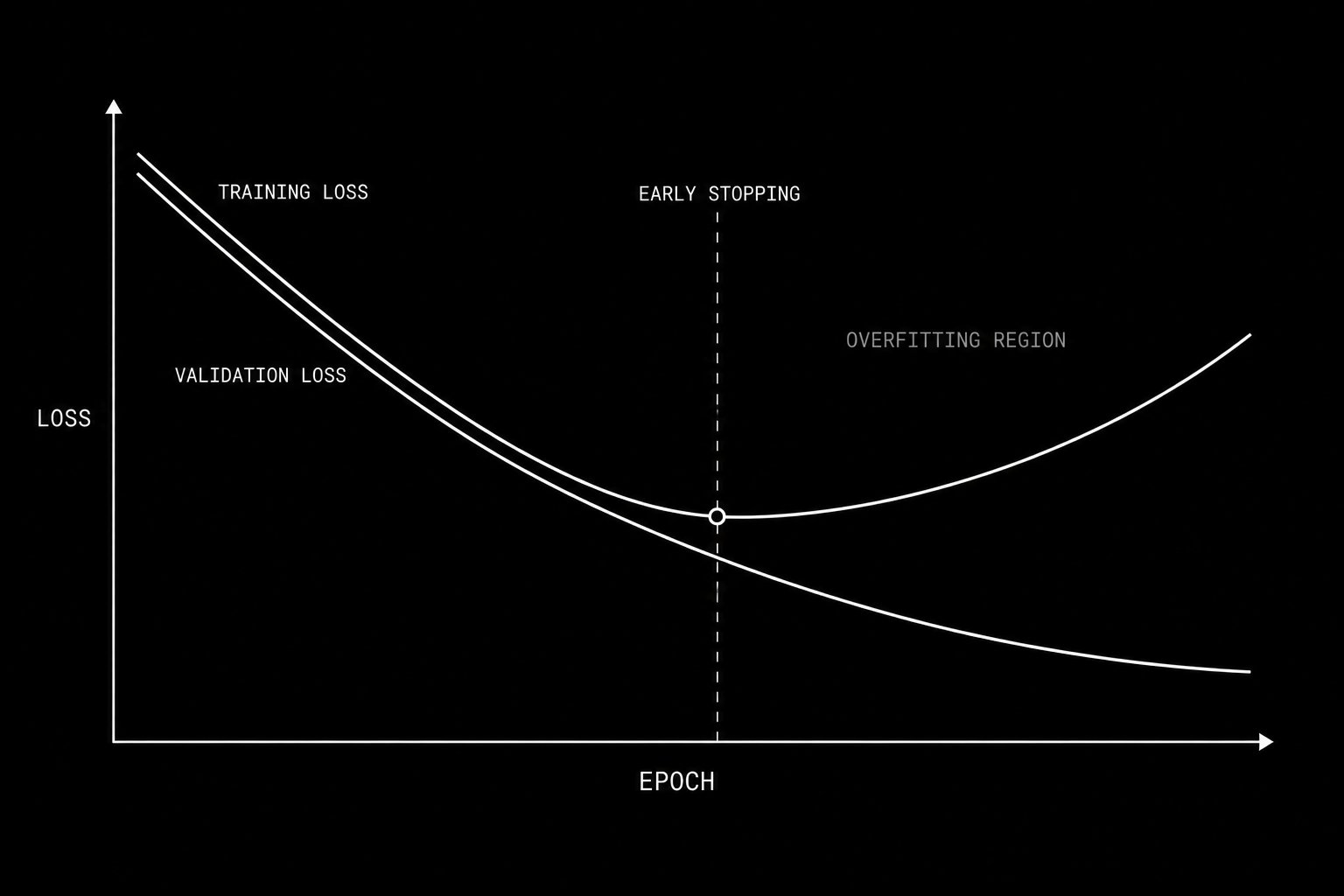

When training loss continues falling while validation loss rises, the model has crossed into overfitting. Early stopping saves the weights at the validation minimum.

Building the model is the easy part. The dangerous part is evaluating whether it actually learned something real versus memorizing the noise in your training data.

Overfitting is the central failure mode of machine learning in finance. An overfit model has found patterns in its training data that do not generalize. On training data it performs beautifully. On new data it performs at chance or worse. The critical problem is that overfit in-sample performance looks identical to genuine edge. You cannot distinguish them by looking at training metrics alone.

The solution is a rigorous three-way data split used in a specific sequential order.

The training set is where gradient descent runs. The model sees this data repeatedly during training and adjusts its parameters based on it. Never evaluate generalization performance on this set.

The validation set is data the model never trains on but that you monitor continuously during training. After each epoch, compute validation loss. The moment validation loss stops improving and begins increasing while training loss continues decreasing, you have found the overfitting threshold. Stop training immediately and save the model weights from the epoch with the lowest validation loss. This is early stopping and it is your primary defense against overfitting.

The test set is data the model has never influenced in any form. You use it exactly once: after all architecture decisions, all hyperparameter choices, and all feature engineering decisions have been finalized using the training and validation sets. The test set result is your honest estimate of live performance. Using the test set to make additional design decisions invalidates it.

For financial time series, these splits must be sequential. The training period comes first in time. The validation period follows. The test period is most recent. Randomizing the split would allow future information to contaminate training, a form of lookahead bias that guarantees your backtest looks better than live performance.

Complete training loop with early stopping:

def train_model(model, train_loader, val_loader, epochs=100, lr=0.001, patience=10):

optimizer = torch.optim.Adam(model.parameters(), lr=lr)

criterion = nn.BCELoss()

scheduler = torch.optim.lr_scheduler.ReduceLROnPlateau(

optimizer, patience=5, factor=0.5

)

best_val_loss = float('inf')

best_weights = None

patience_counter = 0

for epoch in range(epochs):

model.train()

train_loss = 0

for X_batch, y_batch in train_loader:

optimizer.zero_grad()

predictions = model(X_batch).squeeze()

loss = criterion(predictions, y_batch)

loss.backward()

torch.nn.utils.clip_grad_norm_(model.parameters(), max_norm=1.0)

optimizer.step()

train_loss += loss.item()

model.eval()

val_loss = 0

with torch.no_grad():

for X_batch, y_batch in val_loader:

predictions = model(X_batch).squeeze()

loss = criterion(predictions, y_batch)

val_loss += loss.item()

val_loss /= len(val_loader)

scheduler.step(val_loss)

if val_loss < best_val_loss:

best_val_loss = val_loss

best_weights = model.state_dict().copy()

patience_counter = 0

else:

patience_counter += 1

if patience_counter >= patience:

print(f"Early stopping at epoch {epoch}")

break

model.load_state_dict(best_weights)

return model

Gradient clipping is included in this implementation for a specific reason. LSTM gradients can explode during training when the learned sequences are long. Clipping the gradient norm to a maximum value of 1.0 prevents this without significantly affecting convergence speed.

The most rigorous evaluation framework for trading specifically is walk-forward validation. Rather than a single train-validation-test split, you roll a training window forward through time, train, test on the immediately following period, then advance the window and repeat. The concatenated out-of-sample predictions across all windows give you a realistic estimate of how the model would have performed if deployed live at each historical point.

Walk-forward validation:

def walk_forward_validation(features, target, train_size, test_size, step):

all_predictions = []

all_actuals = []

for start in range(0, len(features) - train_size - test_size, step):

train_end = start + train_size

test_end = train_end + test_size

X_train = features[start:train_end]

y_train = target[start:train_end]

X_test = features[train_end:test_end]

y_test = target[train_end:test_end]

scaler = StandardScaler()

X_train_scaled = scaler.fit_transform(X_train.reshape(-1, X_train.shape[-1]))

X_test_scaled = scaler.transform(X_test.reshape(-1, X_test.shape[-1]))

model = TradingLSTM(input_size=X_train.shape[-1])

# train model here

with torch.no_grad():

preds = model(torch.FloatTensor(X_test_scaled))

all_predictions.extend(preds.numpy())

all_actuals.extend(y_test)

return np.array(all_predictions), np.array(all_actuals)

The expected directional accuracy for a well-built model on good features is 52 to 57 percent. This sounds unremarkable. A 54 percent directional signal with a Sharpe ratio above 1.0, applied consistently across hundreds of trades with correct Kelly-derived position sizing, compounds into returns that outperform most discretionary traders over a multi-year horizon. The edge is in the consistency and the scale, not in the magnitude of any individual signal.

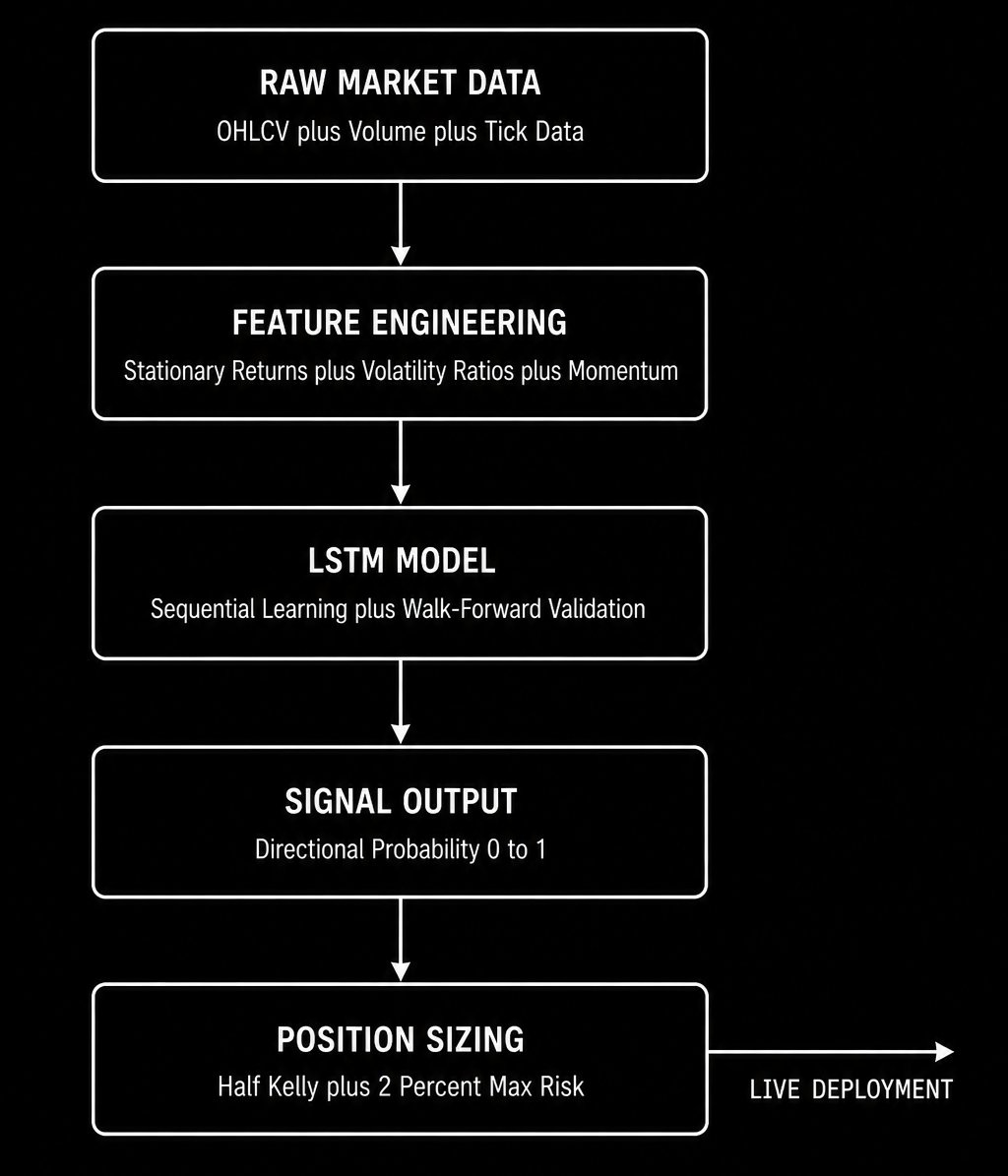

Part 5: The Complete Implementation Pipeline and Deployment

The end-to-end neural network trading signal pipeline from raw data to live position sizing.

This section takes everything from the previous four parts and assembles it into a production-ready signal pipeline. This is the complete end-to-end implementation.

Step 1: Data acquisition and cleaning

Use Polygondotio for institutional-grade tick and OHLCV data. For learning, yfinance is sufficient. Handle missing data, corporate actions, and splits before any feature engineering.

import yfinance as yf

import pandas as pd

ticker = yf.Ticker("SPY")

df = ticker.history(period="5y", interval="1d")

df = df[['Open', 'High', 'Low', 'Close', 'Volume']].copy()

df.dropna(inplace=True)

Step 2: Feature engineering

Build your complete stationary feature set. Every feature must pass the Augmented Dickey-Fuller test.

def build_features(df):

features = pd.DataFrame(index=df.index)

close = df['Close']

volume = df['Volume']

returns = close.pct_change()

features['return_1d'] = returns

features['return_5d'] = close.pct_change(5)

features['return_20d'] = close.pct_change(20)

vol_5 = returns.rolling(5).std()

vol_20 = returns.rolling(20).std()

features['vol_ratio'] = vol_5 / vol_20

features['momentum_norm'] = returns / vol_20

features['volume_zscore'] = (

(volume - volume.rolling(20).mean()) / volume.rolling(20).std()

)

high_low_range = (df['High'] - df['Low']) / close

features['range_norm'] = high_low_range / high_low_range.rolling(20).mean()

sma_5 = close.rolling(5).mean()

sma_20 = close.rolling(20).mean()

features['sma_ratio'] = sma_5 / sma_20 - 1

target = (returns.shift(-1) > 0).astype(int)

features = features.dropna()

target = target.loc[features.index]

return features, target

Step 3: Sequential split and scaling

def prepare_data(features, target, lookback=10, train_ratio=0.6, val_ratio=0.2):

n = len(features)

train_end = int(n * train_ratio)

val_end = int(n * (train_ratio + val_ratio))

scaler = StandardScaler()

features_scaled = scaler.fit_transform(features[:train_end])

features_array = np.vstack([

features_scaled,

scaler.transform(features[train_end:val_end]),

scaler.transform(features[val_end:])

])

X, y = prepare_sequences(features_array, target.values, lookback)

X_train = torch.FloatTensor(X[:train_end - lookback])

y_train = torch.FloatTensor(y[:train_end - lookback])

X_val = torch.FloatTensor(X[train_end - lookback:val_end - lookback])

y_val = torch.FloatTensor(y[train_end - lookback:val_end - lookback])

X_test = torch.FloatTensor(X[val_end - lookback:])

y_test = torch.FloatTensor(y[val_end - lookback:])

return X_train, y_train, X_val, y_val, X_test, y_test, scaler

Step 4: Model evaluation

Beyond directional accuracy, evaluate your model using metrics that matter for trading.

from sklearn.metrics import accuracy_score, roc_auc_score

import pandas as pd

def evaluate_trading_signal(predictions, actuals, returns):

pred_direction = (predictions > 0.5).astype(int)

accuracy = accuracy_score(actuals, pred_direction)

auc = roc_auc_score(actuals, predictions)

signal = np.where(pred_direction == 1, 1, -1)

strategy_returns = signal * returns

sharpe = strategy_returns.mean() / strategy_returns.std() * np.sqrt(252)

cumulative = (1 + strategy_returns).cumprod()

rolling_max = cumulative.cummax()

drawdown = (cumulative - rolling_max) / rolling_max

max_drawdown = drawdown.min()

print(f"Directional Accuracy: {accuracy:.4f}")

print(f"AUC-ROC: {auc:.4f}")

print(f"Annualized Sharpe: {sharpe:.4f}")

print(f"Maximum Drawdown: {max_drawdown:.4f}")

return accuracy, sharpe, max_drawdown

Step 5: Signal to position sizing

A neural network signal alone is not a trading strategy. You need position sizing. The Kelly fraction translates your model’s edge into an optimal bet size:

f* = (p × b - q) / b

Where p is your directional accuracy, q = 1 - p, and b is the average win-to-loss ratio. In practice, use half Kelly to account for parameter estimation error. Never risk more than 2 percent of capital on a single signal regardless of what Kelly recommends.

Step 6: Continuous monitoring and retraining

A model trained on historical data begins degrading the moment it is deployed. Market regimes shift. The conditional expectation the model learned becomes a progressively worse approximation of the current expectation. You must implement a monitoring system that tracks live performance against your validation baseline and triggers retraining when the distribution has shifted beyond an acceptable threshold.

The standard metric is the Kolmogorov-Smirnov statistic comparing your recent live prediction distribution to the historical validation distribution. When the KS statistic exceeds 0.1, retrain on the most recent data and re-evaluate before continuing to deploy.

For prediction markets and crypto specifically, regime shifts are more frequent and more violent than in equity markets. Retraining on a rolling 90-day window with walk-forward re-evaluation every 30 days is a reasonable baseline.

The Summary

Neural networks do not give you a crystal ball. What they give you is a systematic, mathematically rigorous framework for extracting the conditional expectation of market behavior from historical data. When the features are stationary, the architecture is appropriate for sequential data, the training is disciplined and validated correctly, and the signal is sized with proper position management, the result is an edge that is consistent, scalable, and reproducible.

Two Sigma runs 10,000 signals simultaneously through this framework. Renaissance built the highest returning fund in financial history on it. The entry level researcher implementing it earns $650,000 per year.

The complete implementation is in this article. The mathematics is learnable. The code is buildable in a weekend. The only thing that separates the systematic funds from everyone else is knowing the correct framework and the discipline to follow it without cutting corners.

Now you know the framework.

Here is the question I want you to sit with.

A neural network trained on your current indicator set will learn the conditional expectation of market returns given those indicators. But the conditional expectation is only as good as the features you condition on. If you had to add exactly one new feature to your model that you believe no other systematic trader is using, what would it be and why?

Drop your answer in the comments.

There is no wrong answer but there are very revealing ones.

Source

Written by @RohOnChain · View original post