QuantRead

A structured reading path from crypto trader to quantitative systems builder.

This book is a curated collection of articles organized into a deliberate learning sequence. Each phase builds directly on the one before it — skipping ahead will leave gaps that compound into confusion later.

Who This Is For

Anyone who wants to:

- Trade crypto with a systematic, data-driven edge rather than gut feel

- Understand the mathematical foundations that institutional quants use

- Eventually build a personal quant system that generates trading signals automatically

The Five Phases

| Phase | Focus | Goal |

|---|---|---|

| 1 — Trading Foundations | Markets, price action, risk | Understand how markets work and how to survive in them |

| 2 — Trading Strategies | Momentum & mean-reversion | Execute real trades with clear edge and rules |

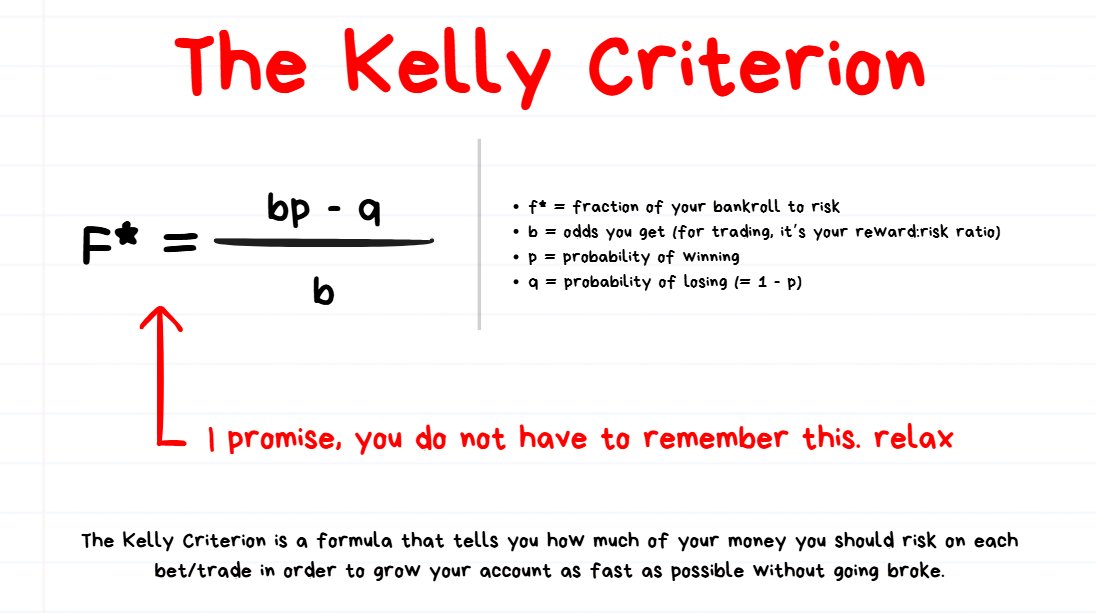

| 3 — Portfolio Construction | Diversification, Kelly, risk parity | Think in systems, not individual bets |

| 4 — Quant Foundations | Math, statistics, programming | Build the mathematical toolkit quant firms use |

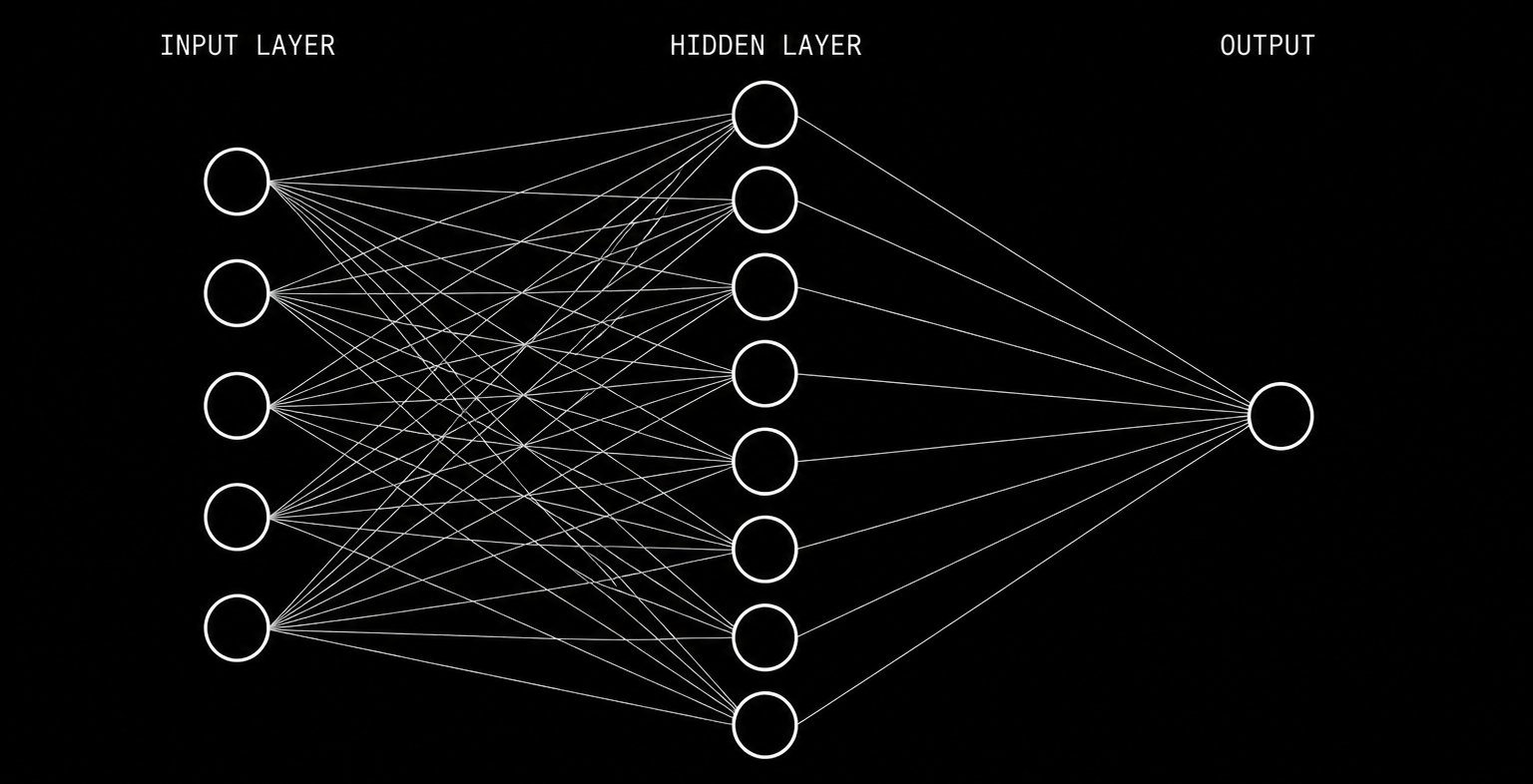

| 5 — Quant Systems | Markov Chains, Neural Networks | Code systematic signal-generation models |

How to Use This Book

Read in order. Each article is a standalone piece but the sequence is intentional.

As you go through each phase, ask yourself: “Can I explain this concept to someone else without looking at notes?” If yes, move on. If not, re-read.

Phases 1–3 are about becoming a trader. Phases 4–5 are about becoming a quant.

The goal is to be both.

How to Start Learning to Trade

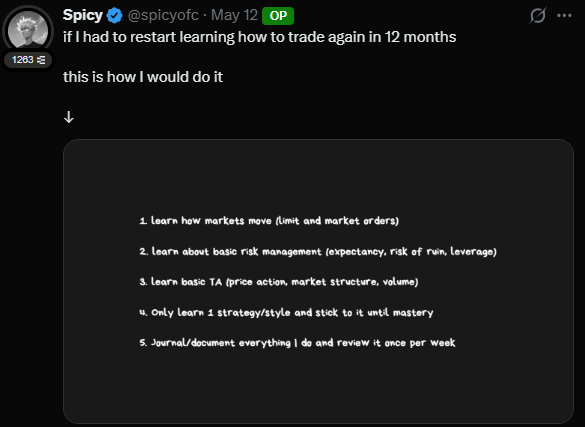

If I had to restart learning how to trade again in 12 months

- learn how markets move (limit and market orders)

- learn about basic risk management (expectancy, risk of ruin, leverage)

- learn basic TA (price action, market structure, volume)

- only learn 1 strategy/style and stick to it until mastery

- journal/document everything I do and review it once per week

1. Learn how markets move (limit and market orders)

Markets run on buyers and sellers placing orders. There are two basic order types:

- Market order — buy/sell immediately at the current price. Fast, but you have no control over your entry price.

- Limit order — place an order waiting at a specific price. More deliberate, lets you get a better price, but the order may never fill.

👉 Understanding these two order types = understanding how money flows in and out of the market.

2. Basic risk management (expectancy, risk of ruin, leverage)

- Expectancy — On average, does each trade make or lose money? A good strategy needs positive expectancy: profits outweigh losses over the long run.

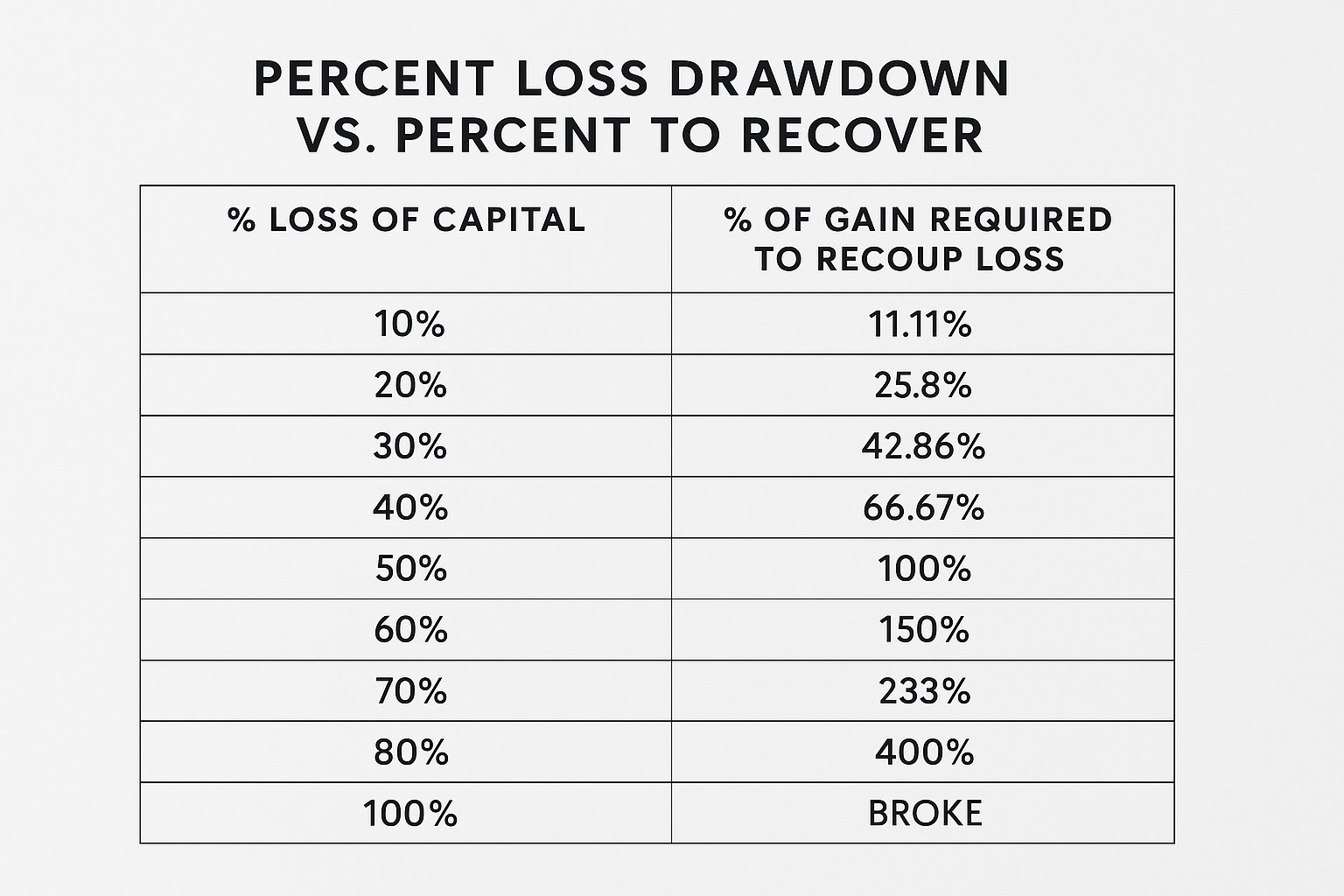

- Risk of ruin — If you keep losing, how long before you run out of capital? Risk too much per trade → blow up fast, even with a good strategy.

- Leverage — Lets you trade with more than your actual capital. Bigger potential gains, but losses are multiplied equally. Misuse it and you self-destruct.

👉 Risk management matters more than strategy — lose less, stay in the game longer, and you give yourself a real chance to win.

3. Basic technical analysis (price action, market structure, volume)

- Price action — Read candlestick charts to understand market psychology: who is in control, buyers or sellers?

- Market structure — Is the market trending up, trending down, or ranging? Identify the bigger trend before entering a trade.

- Volume — Trading volume confirms the strength of a move. Price up + high volume = real move. Price up + low volume = be skeptical.

👉 These three elements help you read the market’s “language” instead of guessing.

4. Learn only one strategy/style and stick with it until mastery

Beginners often fall into “strategy hopping” — jumping to whatever looks good, never committing to anything long enough to get results.

Pick one approach (e.g. breakouts, support/resistance, trend following) → practice long enough → only then will you know if it actually works for you.

👉 Discipline matters more than finding the “perfect strategy.”

5. Document everything and review it once a week

A trading journal is the most powerful tool for improvement. Log: your reason for entering, your emotions at the time, the outcome, what went wrong. At the end of each week, sit down and review to find patterns in your own behavior.

👉 No journaling = no idea where you’re going wrong = repeating the same mistakes forever.

These five points are not about finding a “winning tip” — they are about building the foundation to survive and improve in trading over the long run.

Profitable Trading: Reverse Engineered

There are 5 Stages I went through from Unprofitable → Profitable.

I’m going to explain each of them below but in reverse.

I believe it will be easier to retain the information this way.

In this article I’m going to explain:

- Help you understand what a “constraint” is

- Explain each of the 5 stages starting from top to bottom.

- I will also explain what was the constraint that had to be solved in order to ascend to next stage

- Present my solution to each constraint at every single stage

I’m going to go pretty in-depth with everything here.

Let’s get started ↓

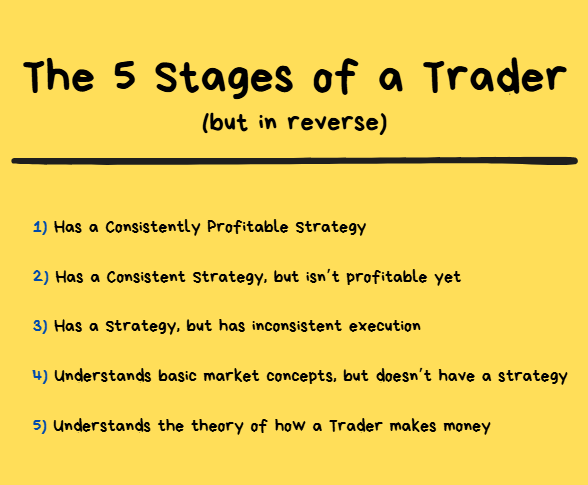

The 5 Stages and the Theory of Constraints

Remember we’re going to go in reverse with this article.

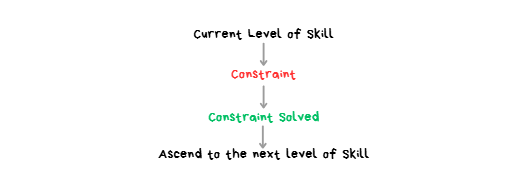

Defining “Constraint”:

CONSTRAINT: The single biggest bottleneck holding a trader back from advancing to the next level of skill.

- It’s the one biggest problem that, if solved, makes everything else easier or unnecessary.

- An effective approach for improving at anything is identifying the biggest constraint and then pouring all focus, attention and resources into solving that specific constraint.

- This means tunnel vision focusing on solving 1 problem while ignoring all other problems.

In summary, at every stage a trader will need to identify their biggest constraint and continue to chip away at it until it is solved before they can ascend to the next stage.

Below I will get into each of the 5 Stages, their Constraints and how to Solve them. ↓

Stage 1 — Profitable Strategy

gentle reminder that we are reverse engineering this process and going backwards ;)

How to know you are at Stage 1:

• You have a strategy which can generate profits over a large # of trades.

• You have data to show that your strategy has a positive expectancy.

• You have some kind of process for improving your strategy and you have used this process many times already.

Stage 2 — Consistent but Not Yet Profitable

Let’s talk about the Stage that comes right before crossing over to becoming Profitable.

Every trade is being executed in the same way. The only issue is that the strategy isn’t actually making any money.

The point right before having a Consistently Profitable Strategy is having a Consistent Strategy but not necessarily Profitable.

How to know you are at Stage 2:

- You have a “consistent” trading strategy

- entry is the same on every trade

- exit is the same on every trade

- If you were to review 100~ trade screenshots they would all look pretty much the same.

This is the point where you have the skills to do market analysis + you have a strategy but money just isn’t coming in.

It can feel frustrating because it feels like “something is missing”.

That “something” is an “Improvement Process”

Explained below ↓

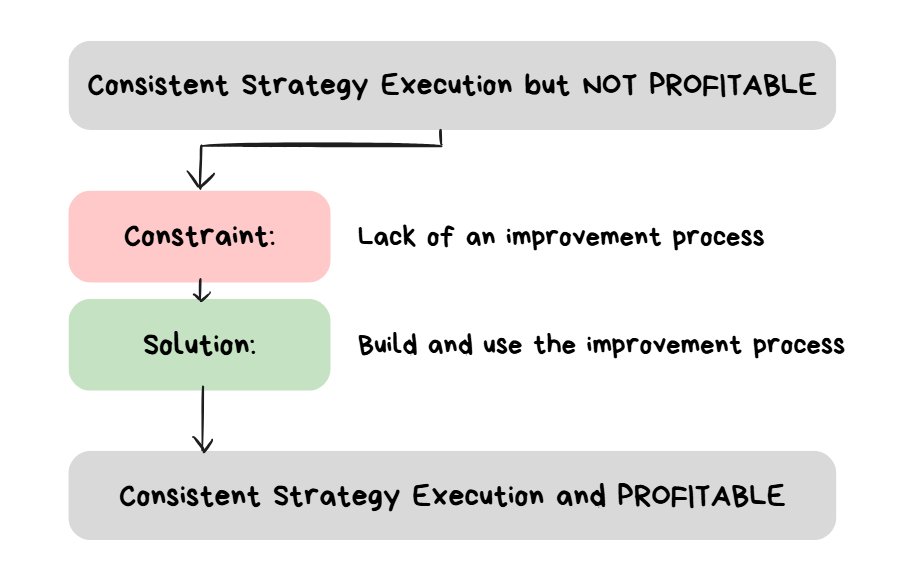

identifying the constraint and solution for Stage 2

QUESTION: What is the thing that MUST OCCUR in order to go from “a consistent strategy but it loses money” to “a consistent strategy but it makes money”?

ANSWER: An improvement process being used multiple times

Explanation

- Imagine a car is at Town A and needs to get to Town B which is 100km away.

- The car MUST BE MOVING in order to get to Town B. If it is standing still then it will not get to Town B.

- If the car is moving, regardless of how slow it is, it will eventually get to Town B.

The Point

- The ONE THING that matters the most at this stage is building an improvement process for your strategy and then using it as much as possible until eventually reaching profitability.

- It’s like having software which has 100 bugs in it. Build a process to identify each bug and fix each bug 1 at a time and eventually your software will work.

- This is a volume game. It’s unlikely that you are going to fix 1 issue with your strategy and magically become profitable.

- It’s more likely that you may need to fix 100+ things

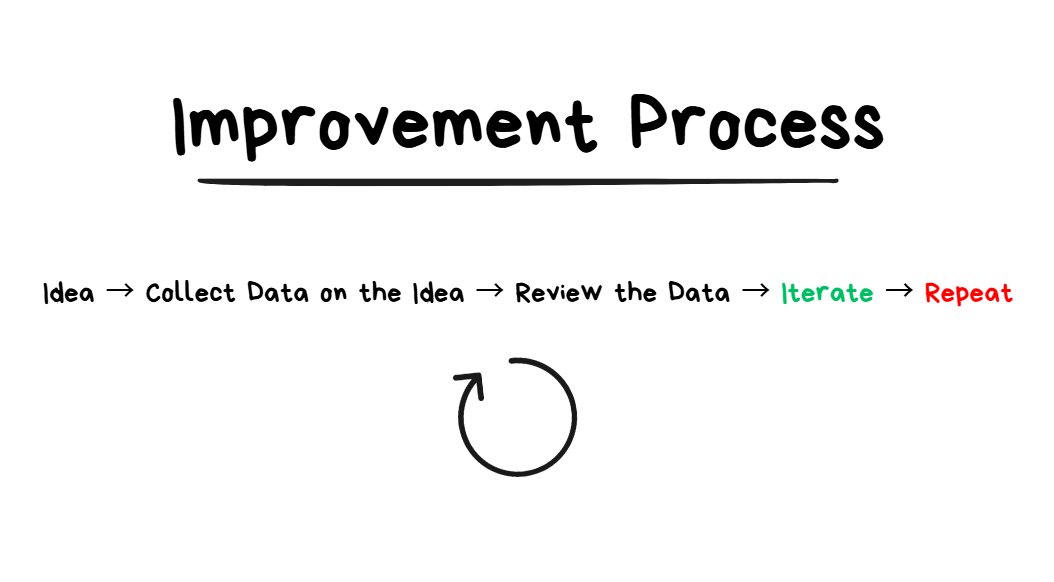

The Solution: Building the Improvement Process

more repetitions with this loop = better ideas

better ideas = better iterations

There are 4 components to the improvement process:

- Idea (“I wonder if X will improve my winrate?”)

- Data Collection (see how many times X appeared in your trades)

- Review Data (see how much impact X had on the winrate)

- Iterate (based on the review, make a change to the trade execution next time X appears for a trade)

If you go through this feedback loop enough times then it is inevitable that you will perform better.

NON-TRADING EXAMPLE:

- Pretend I want to make a “cookie shop” which sells tasty cookies

- I bake 1 batch of cookies.

- I taste them, but feel like they’re not salty enough.

IDEA: I think they’re not salty enough. If I made them more salty then more people would like them.

DATA: I’m going to give my normal cookies and “slightly saltier” cookies to 100 different people and see which one they prefer.

REVIEW DATA: 73% of people prefer the salty cookies.

ITERATE: I will make a small adjustment to the recipe so that the cookies have a bit more salt in them based on the review of my data.

THE POINT: if I was to go through this same process and make 1,000,000 iterations I would have incredibly good tasting cookies by the end of it.

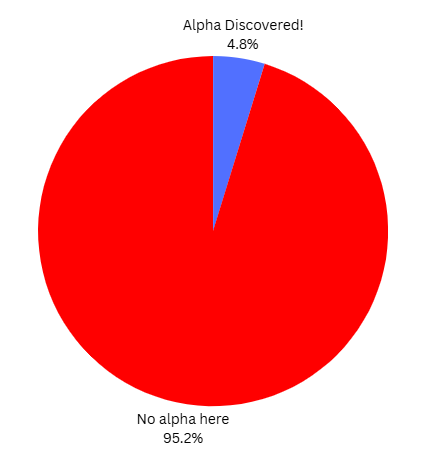

Important Reminder: Not All Reviews Will Find Alpha

Only X% of your reviews will lead to finding “alpha” (a potential improvement in your strategy).

X is going to be a low number.

When you go through this “improvement process” multiple times you may find that a lot of the time you find yourself empty handed.

You had an idea, collected data on the idea, reviewed the data and it turns out there’s nothing special about the idea.

This doesn’t mean that “you suck” or that “your process is broken”.

This is just how things are. Edge is like a needle in a haystack. The sooner you accept this, the easier everything else will be.

When the above is understood, it then becomes clear that there are 4 things to be optimizing for:

- QUANTITY of data (how much data do you have)

- QUALITY of data (how statistically significant is the data)

- QUANTITY of reviews (how many reviews are you performing each month)

- QUALITY of reviews (increasing the likelihood of finding alpha within a review)

If you make ANY of these 4 go up, you will find MORE alpha.

This is a game of brute force.

Let’s use an extreme example:🤓

- You have 1,000,000,000 ideas about the market.

- You collect 1,000,000,000 data points on EACH idea.

- You review all 1,000,000,000 data sets

- 999,999,000 reviews end up going nowhere

- 1000 reviews end up finding real alpha

- If you have 1000 pieces of real alpha, you will become very profitable.

This should make it crystal clear that this is a game of brute force.

Get MORE ideas, TEST more ideas, REVIEW more ideas and you WILL FIND MORE ALPHA.

It sounds simple but it is hard and time consuming.

A Practical Improvement Process

So there’s really only 2 things that we can do to make more money:

- Option 1: Make MORE profitable decisions

- Option 2: Make LESS unprofitable decisions

The 2nd one is generally a lot easier to start with.

You can do literally EVERYTHING the same in your process but if you just make LESS MISTAKES then you will make MORE MONEY as a result of it.

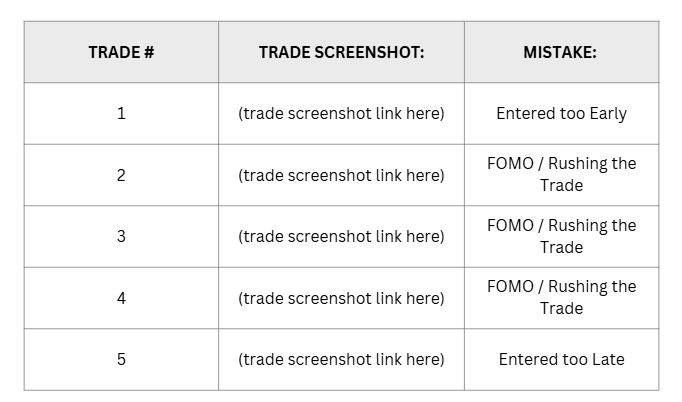

the easiest trade screenshot review you start with:

- finding trade execution mistakes

Before you start looking for super duper new Alpha, start with the raw basics.

- Identify every trade where you broke the rules of your trading strategy. Put all of those screenshots in a column of a spreadsheet. (it doesn’t even matter if the strategy is profitable or not. The point is you need to stick to the rules)

- Find the most common mistake

- Introduce an input which decreases the chance of the same mistake happening again.

Two Examples:

Entering too early? - use a checklist for all criteria that needs to be met

Entering too late? - use more alerts to give you more of a heads up that a potential trade is coming

Taking This Even Further

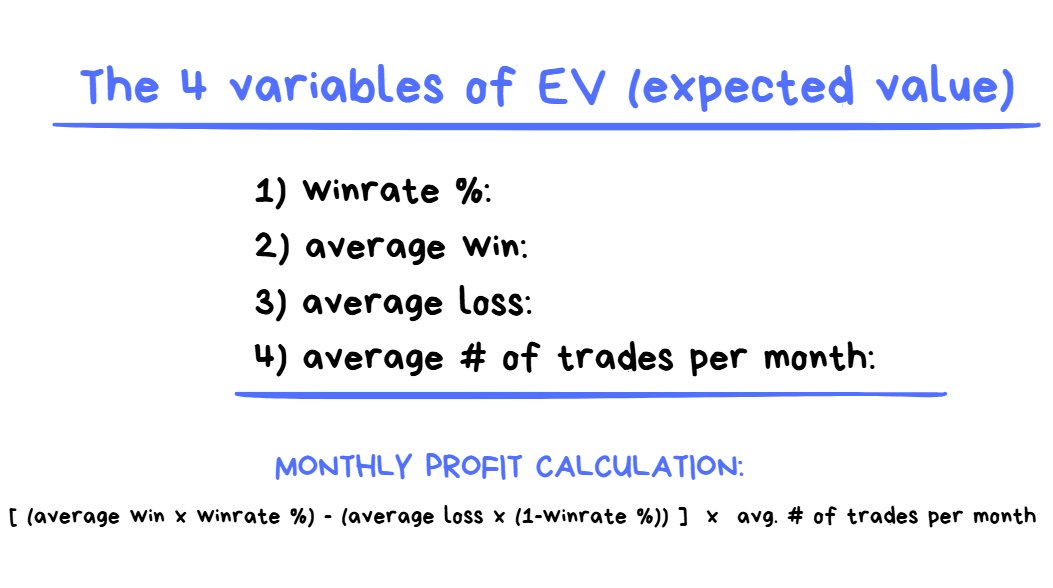

“the 4 variables of EV” and “the monthly profit equation”

After you have eliminated all mistakes from your execution the next step is to get creative.

You’re going to have to come up with ideas which impact any of these 4 variables in your strategy execution:

- Improve Winrate %:

This can be done by taking MORE GOOD TRADES or LESS BAD TRADES

2. Increase Average Win

This can be done by RISKING MORE ON GOOD TRADES or INCREASING THE WIDTH OF YOUR TARGETS

3. Decrease Average Loss

This can be done by CUTTING LOSERS EARLIER or REDUCING COSTS (fees/slippage)

4. Increase Trade Frequency

This can be done by INCREASING SCREENTIME , MORE/BETTER ALERTS and/or introducing MORE STRATEGIES into your toolbox.

From personal experience, this is the specific order I have found most effective to take for strategy improvement (based on amount of effort it takes to collect/review the data relative to the ROI of the insights gained from the dataset) :

- make fewer mistakes (increases winrate)

- take fewer low quality trades (increases winrate)

- cut losers faster on A+ setups (decreases avg. loss)

- risk more on A+ setups (increases avg. win)

- wider TP on A+ setups (increases avg. win)

- more/better alerts (increases frequency)

- introduce more strategies into toolbox (increases frequency)

If you use the Improvement Process Loop for 100 ideas on each of these 7 things it would be unreasonable to not find improvements within your execution.

Yes, this means coming up with 700 ideas, collecting 700 data sets, performing 700 reviews and iterating accordingly.

It’s simple but it takes effort and time.

Summary of Stage 2

If you have a strategy and you’re consistent with executing it but you’re NOT profitable yet, the thing that you’re missing is an improvement process. Use the “idea , collect data , review , iterate” loop to eliminate mistakes. Once all mistakes are eliminated, use the loop over and over again to make improvements to any of the big 4 variables in the EV equation which make up your monthly profit.

If you keep going through the loop you WILL find improvements and you WILL make more money.

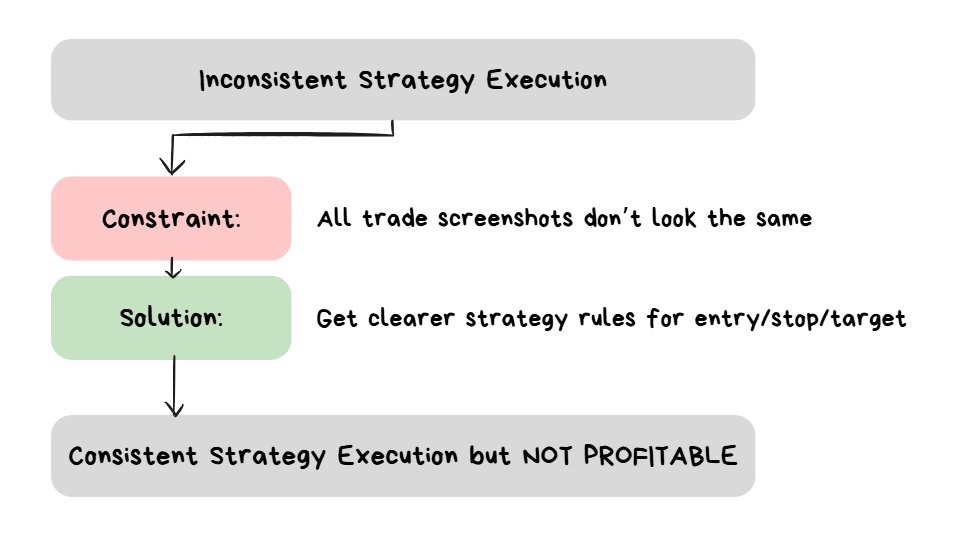

Stage 3 — Inconsistent Strategy

Before having a consistent strategy, you must have an inconsistent strategy.

How to know you are at Stage 3:

You have a strategy but none of the trades look the same.

This is a problem because it makes Stage 2 harder to pass.

If every trade has different rules for entry, stoploss, target and management then it’s going to be really hard to find improvements.

Let’s use the Cookie Shop analogy again to explain how this is a problem:

- Imagine you bake 20 cookies.

- Each cookie has a different shape, size, color and flavor.

- If you try to put your cookies through the Improvement Process it will be too challenging to know what variable needs to be improved.

- 5 people might say too salty, 8 people might say too sweet, 3 people might say not sweet enough … the feedback from the data you collect will be all over the place and cannot be reliable because none of the cookies are the same.

- But if you bake the IDENTICAL cookie with ALL variables kept equal, you will be able to trust the data if 80% of people say “not salty enough”.

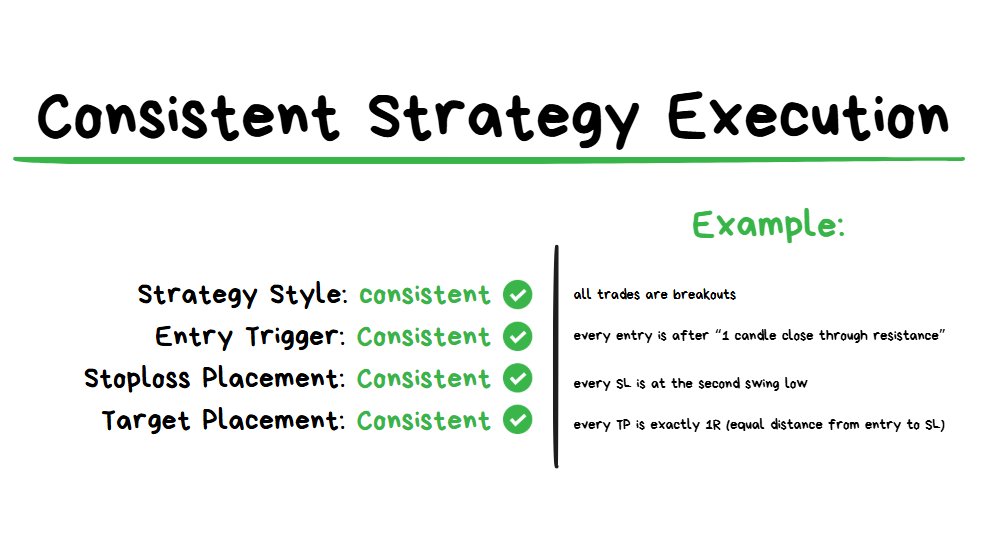

The Solution: Consistent Trade Execution

When all trade screenshots look pretty much the same, then the constraint has been solved.

Consistency > Quality

FIRST make everything the same. You can optimize each of these LATER.

These problems I was facing while I was in this stage:

- I was trading BOTH breakouts and reversals, instead of just 1 style.

- I would be entering trades based on gut feel, instead of a clear entry trigger

- My stoploss would be placed at a place which “felt right” , instead of using a specific location every time.

- My target would also be based on gut feel, instead of using a specific target every time

The issue was that I was too short-sighted. I wanted to make money immediately and wanted to just skip over this step. If I thought it was good to trade reversals I would just trade reversals, if I thought it was good to trade breakouts I would trade breakouts… but from doing so many different things at the same time I was average at everything.

Mediocrity in Trading = NOT PROFITABLE.

🧠 SOLUTION = consistency. MAKE EVERYTHING THE SAME, DON’T WORRY ABOUT SHORT TERM RESULTS.

Eventually I realized that the only way that I could improve was to keep literally every single variable THE SAME and as SIMPLE AS POSSIBLE.

This means optimizing for CONSISTENCY rather than optimizing for RESULTS.

If execution IS NOT CONSISTENT but getting good results: then improving this strategy is going to be a really hard and slow process. I don’t want this. ❌

If execution IS CONSISTENT but not getting good results: then improving this strategy is going to be a fairly straightforward process. Even though short term results might suck, there’s a clear path forward for continuous iterations and fast learning/improvement. I want this. ✅

CONSISTENCY > SHORT TERM RESULTS

Summary of Stage 3

At this stage you have a strategy but the execution of the strategy is inconsistent and all over the place. In order to get over this stage you’re going to need consistent execution. This means same strategy style, same entries, same stoploss placement and same targets. If you want to get over this stage you’re going to have to let go of “perfection”. Accept that the short term results will suck, this is fine. The point is to make the strategy as EASY AS POSSIBLE to improve (by collecting lots of consistent data). The more identical your trade screenshots look, the easier the strategy will be to improve.

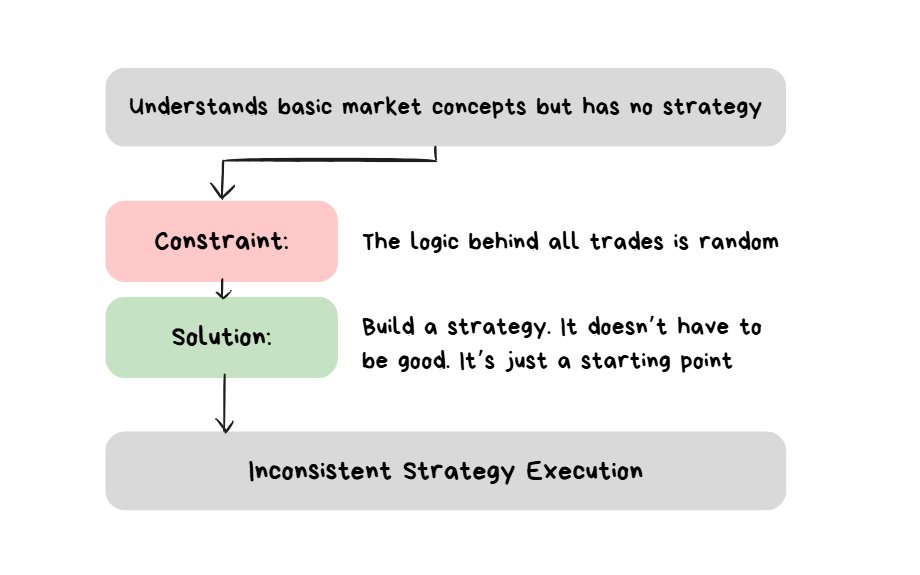

Stage 4 — No Strategy

Before having an inconsistent strategy, this is the stage of “having no strategy”.

at this stage understands basic technical analysis + risk management. The issue is just doesn’t know “what to actually do” in order to execute.

There are a lot of traders at this stage.

How to know you are at stage 4:

- You know some basic price action principles (e.g. bullish/bearish market structure)

- You know how to use an exchange and execute trades

- You know risk management basics

- But you DO NOT have any strategy with clearly defined rules for entry/stop/target/management.

The Solution: Having Some Strategy Rather Than None

something is better than nothing. This is not the time to worry about “quality” … (yet).

Without a strategy, throwing on longs/shorts blindly is really no different to going to a casino to gamble.

“Red or Black” v.s. “Up or Down” - same game, different name.

To overcome this stage a strategy needs to be built. Just SOMETHING. It doesn’t even have to be good. You can always “make it good” later.

Trying to immediately “make something good” with absolutely no reference points is foolish.

The Clay Pottery Class Analogy:

- A pottery teacher splits his class into 2 groups. Group A and Group B.

- Group A: their goal was to make the best looking clay pot in 30 days.

- Group B: their goal was to make as many clay pots as possible in 30 days.

- Result: Group B inevitably ended up making better looking clay pots (without even trying to) just because they had more repetitions and iterations.

- The point: get a high volume of reps FIRST. Do optimization SECOND.

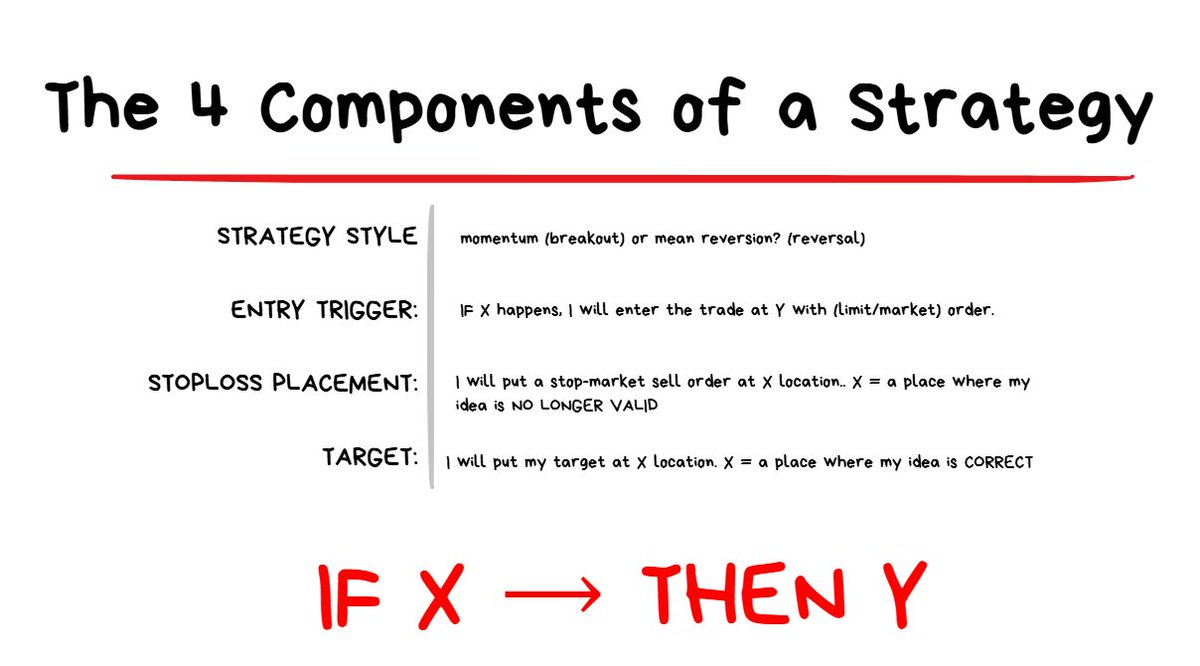

The Four Components of a Trading Strategy

each component of a strategy follows a “IF X –> THEN Y” framework.

If X happens –> then I will do Y action.

If X does not happen –> then I will not do Y action.

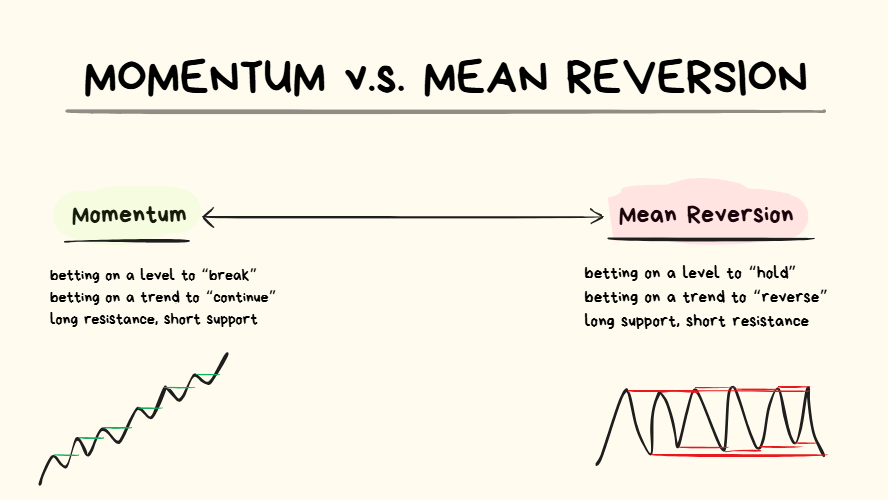

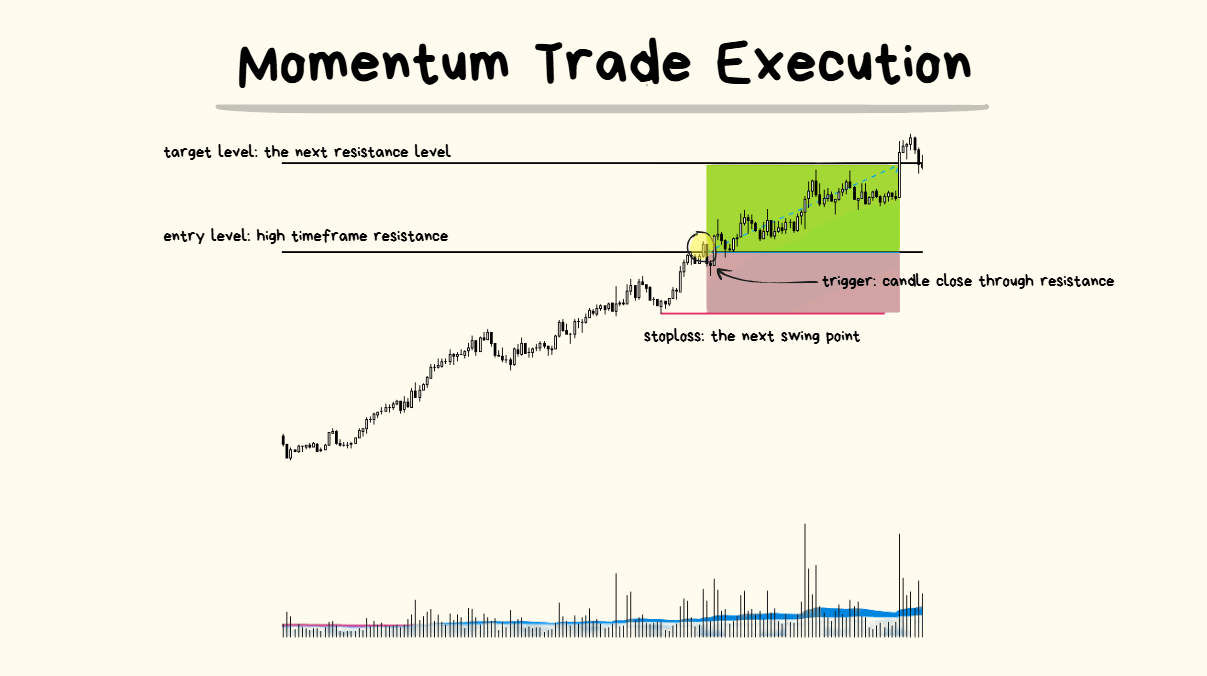

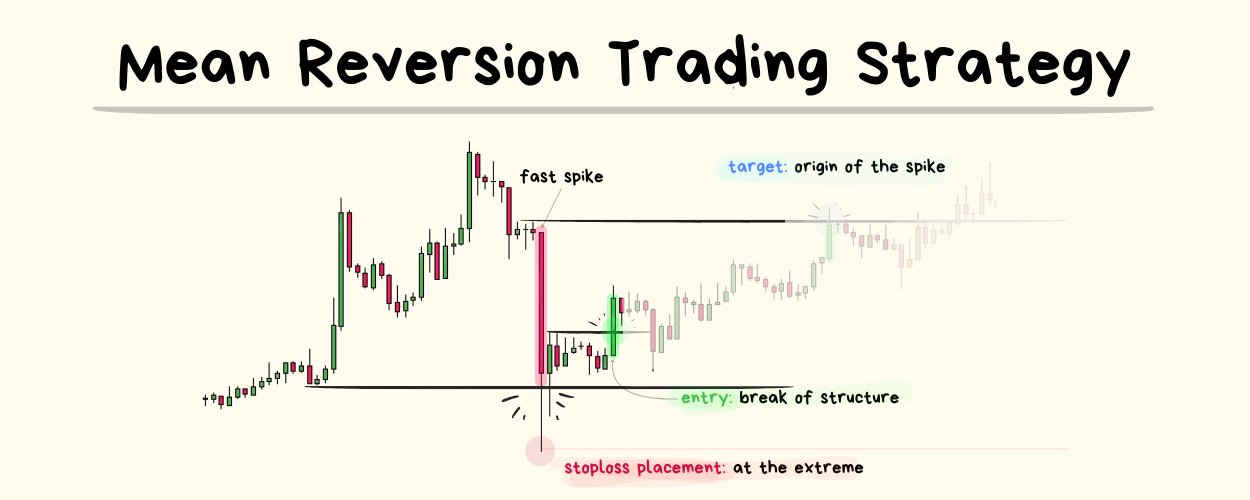

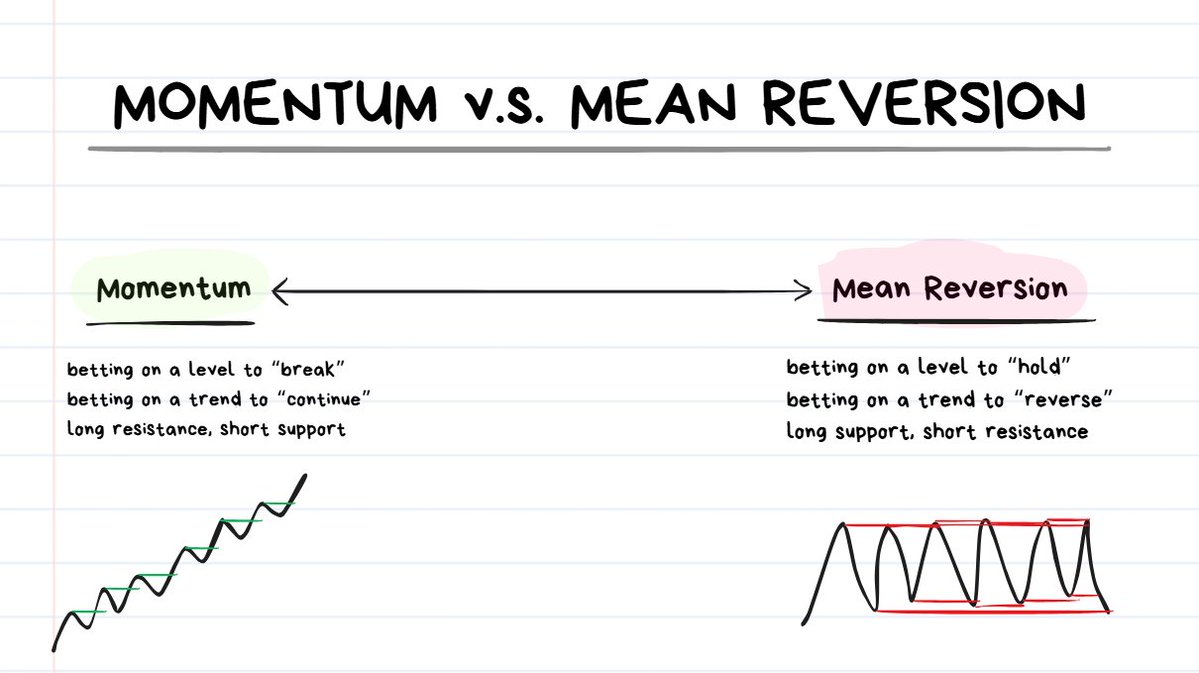

STRATEGY STYLE: Momentum or Mean Reversion

- Momentum = betting that price will “break” a level

- Mean Reversion = betting that price will “reverse” from a level

- You’re going to have to pick if you want to trade Momentum or Mean Reversion to start off with.

- It doesn’t matter which one you pick because in the long term you will inevitably learn how to trade both.

- I recommend starting with Momentum because it’s easier and there are less variables you have to consider.

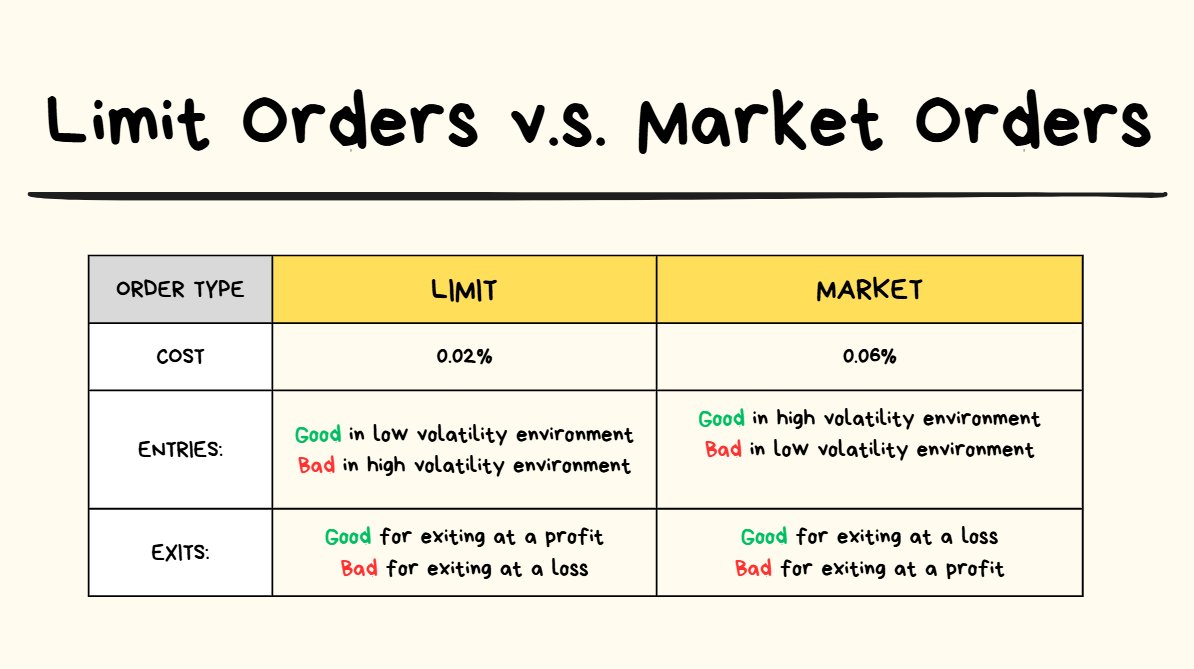

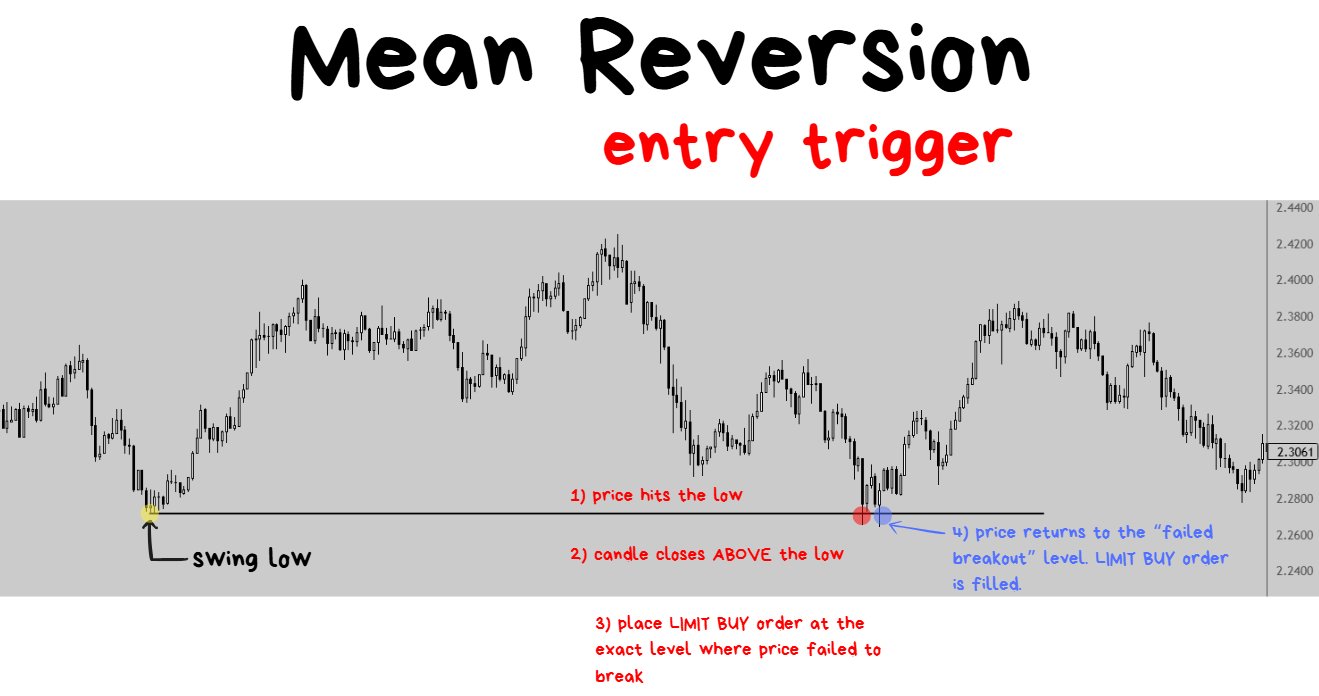

ENTRY TRIGGER: if X happens, I will place my entry at Y using (limit/market) order.

- The more simplistic the approach you have for defining X and Y, the easier everything else will be.

- Remember, simple is best at this stage. It’s not about finding the winning combination yet. It’s about having something that will be EASY to collect data on and EASY to iterate/improve.

- I suggest starting with limit order entries.

- Accept that you will miss some winning trades when using limit orders for entry. This is a feature, not a bug.

- As long as missed trades are journaled it will be easy to review them and easy to introduce market orders to start catching some of those missed trades.

STOPLOSS PLACEMENT: If X happens, I will put my stop-market sell order at Y location.

If going LONG = place stoploss at a swing low.

If going SHORT = place stoploss at a swing high.

❗️NOTE TO READER: will discuss market structure + price action concepts a bit further down below.

TARGET PLACEMENT: If price reaches X = my idea is correct.

- Assume that the first attempt of creating this rule for your target placement is NOT GOING TO BE OPTIMAL.

- It’s either going to be TOO WIDE or TOO TIGHT.

- Question: If I had to pick, would I rather have a TP that is too wide or too tight?

- Answer: Too tight.

- Reasoning: to improve a tp that is too tight you just have to look at winning trade screenshots where price extended beyond the TP by “N units of R” and then optimise from there. It’s straightforward. However to improve a tp that is too wide you have to look at losing trade screenshots where price went N units of R onside and then turned around and turned into a losing trade. It’s a tougher process.

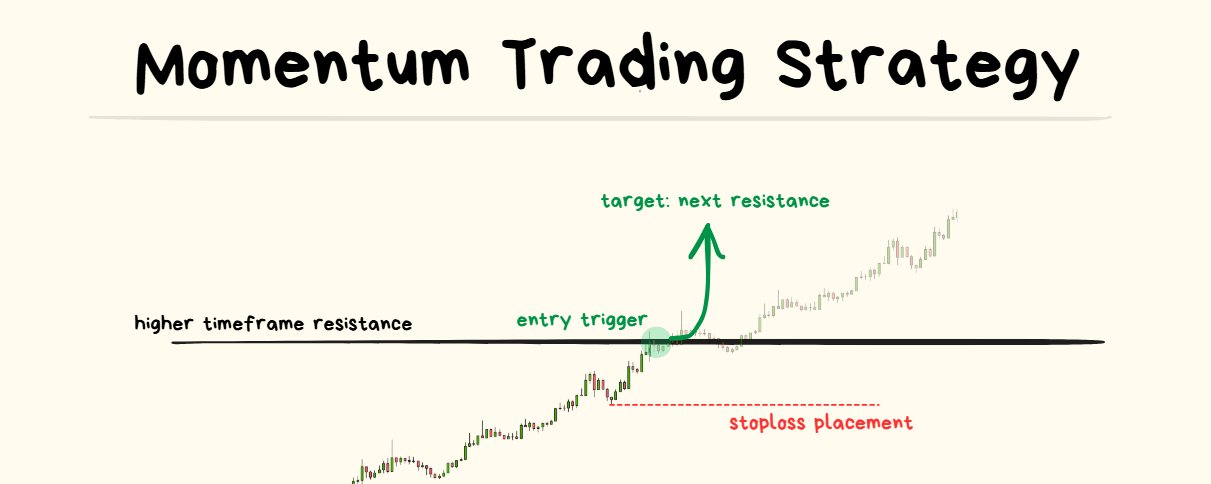

Further Reading: Momentum Trading Strategy

Jul 31, 2025

Summary of Stage 4

If you have no strategy, the only way to move forward is to build a strategy. Something is better than nothing. Get some rules in place for the Strategy Style, Entry Trigger, Stoploss Placement and Target Placement. Don’t waste time trying to optimize it or make it perfect. Just build SOMETHING. After you have SOMETHING, you can go and optimize it AFTER you collect some data with using it.

The constraint is solved as soon as you can clearly state the rules of your strategy.

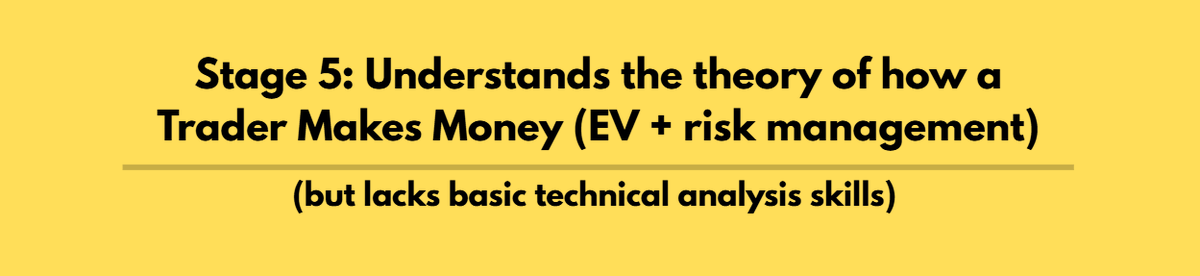

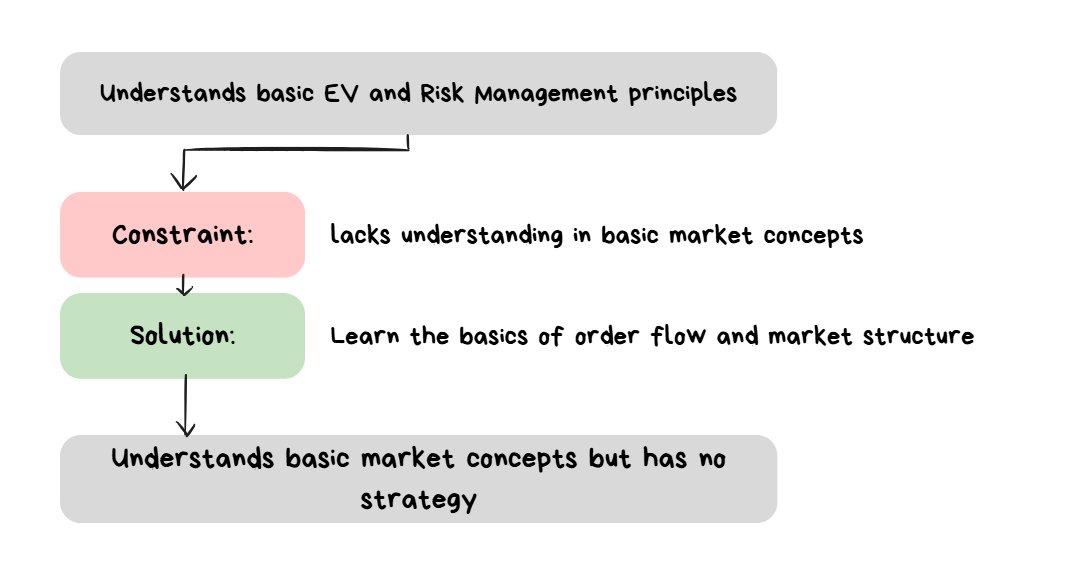

Stage 5 — Learning the Basics

The trader knows what “expected value” is and understands that the goal of a trader is to capture as much of it as possible.

The trader just has no idea where to start with the basics of the technicals.

It’s not about winning the next trade. It’s about having a profit over the next N number of trades, where N is a large value.

How to know you are at Stage 5:

- You understand the importance of having an Edge

- You understand what Expected Value (EV) is

- You know basic Risk Management concepts

Before building a strategy, a Trader has to at least understand the basics of how markets move and some basic price action concepts.

The Solution: Learning Market Structure + Price Action Basics

Before getting into the practical (actually doing stuff), one has to learn at least some basic theory (how stuff works).

These are the 2 Topics I will cover below:

-

- How do markets move (market/limit orders basics)

-

- market structure + regimes basics

You don’t have to remember each and every single detail. It is more important to just understand the basic concepts.

After a basic understanding of the concepts is achieved does it make sense to start looking into building a strategy.

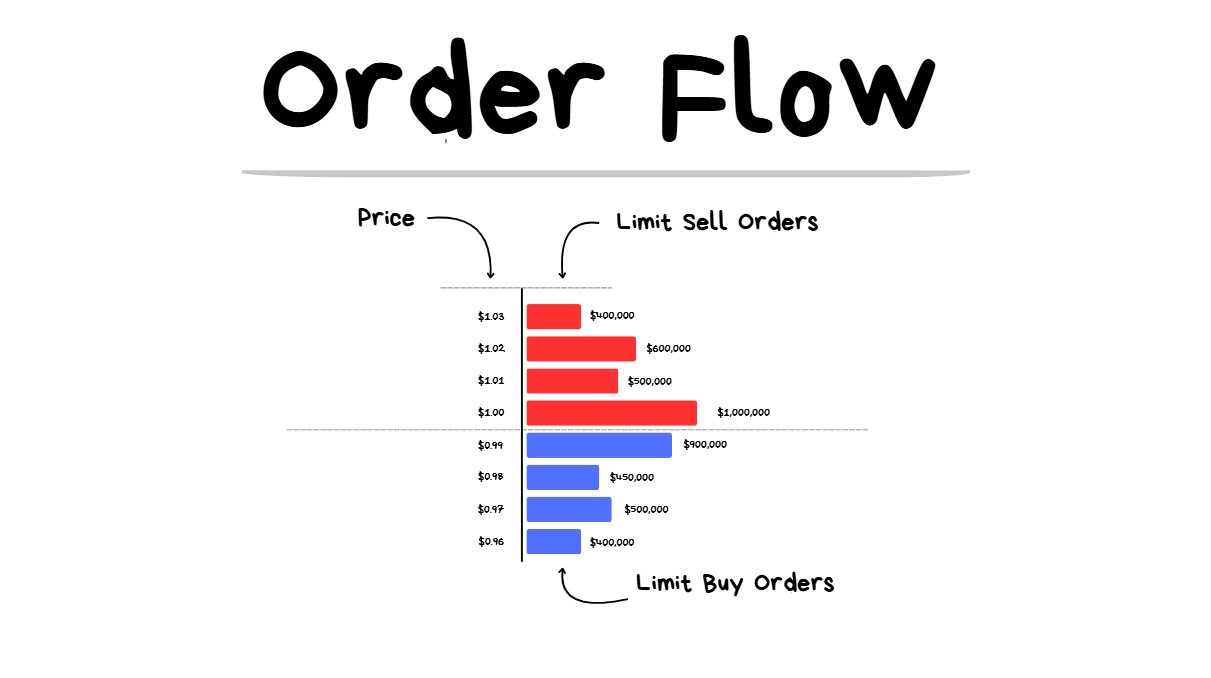

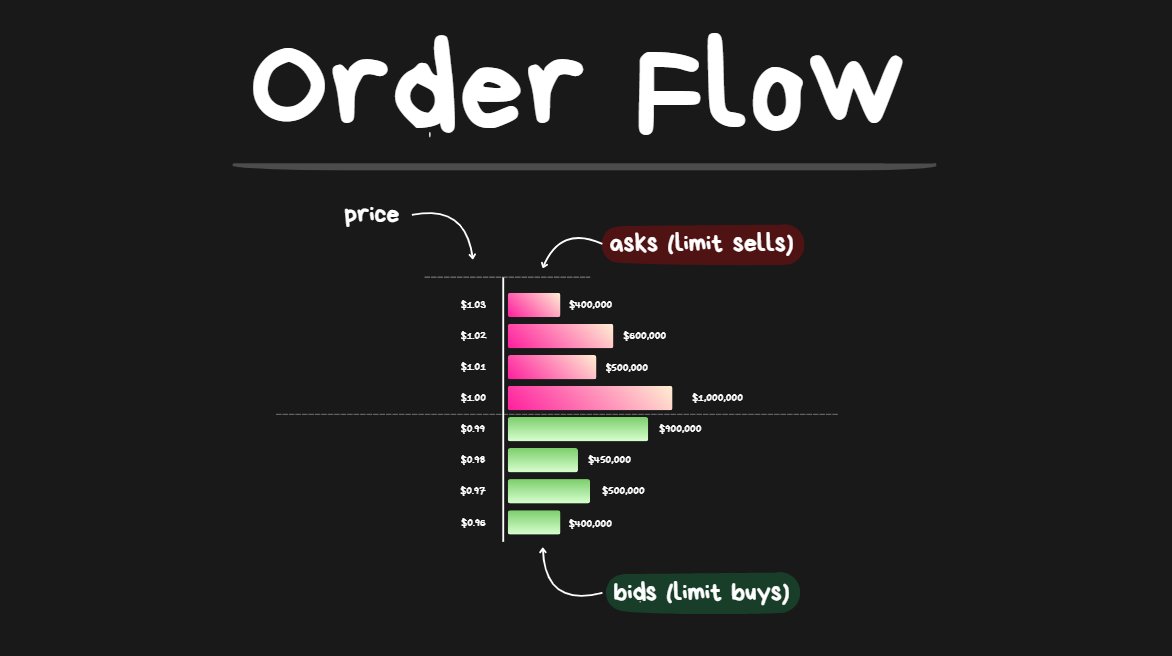

1) How Do Markets Move?

order book

The two order types:

- Limit Orders (I am advertising to execute a trade at X price. My trade will only execute if another participant wants to execute at my price.)

- Market Orders (I want to execute a trade NOW. I will pay an extra fee to get my trade executed immediately at whatever the best available current price is.)

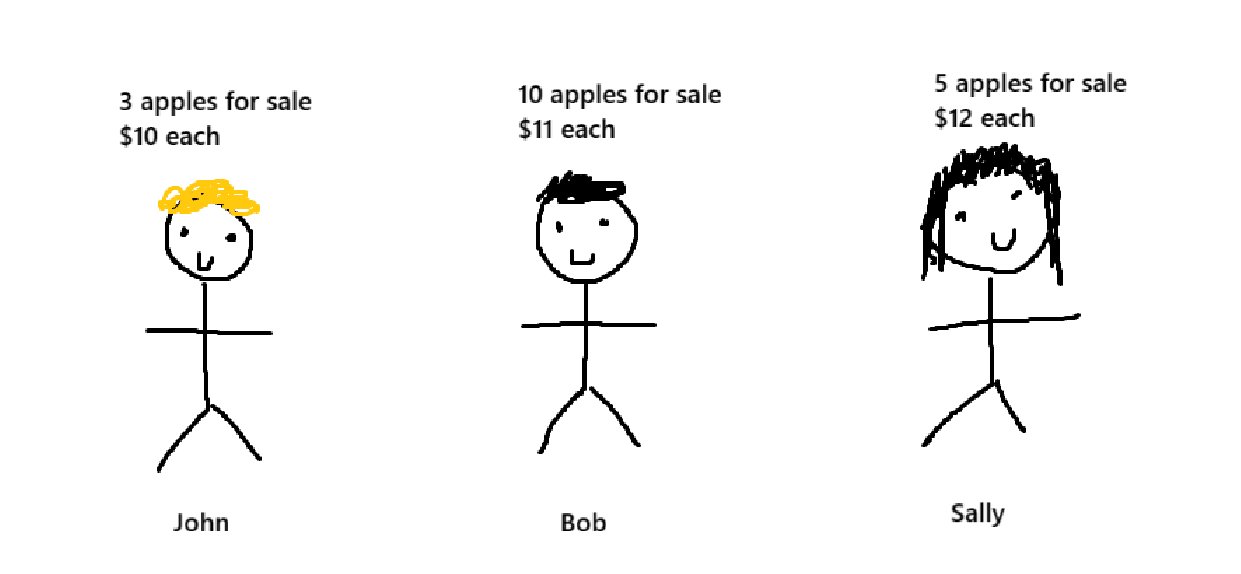

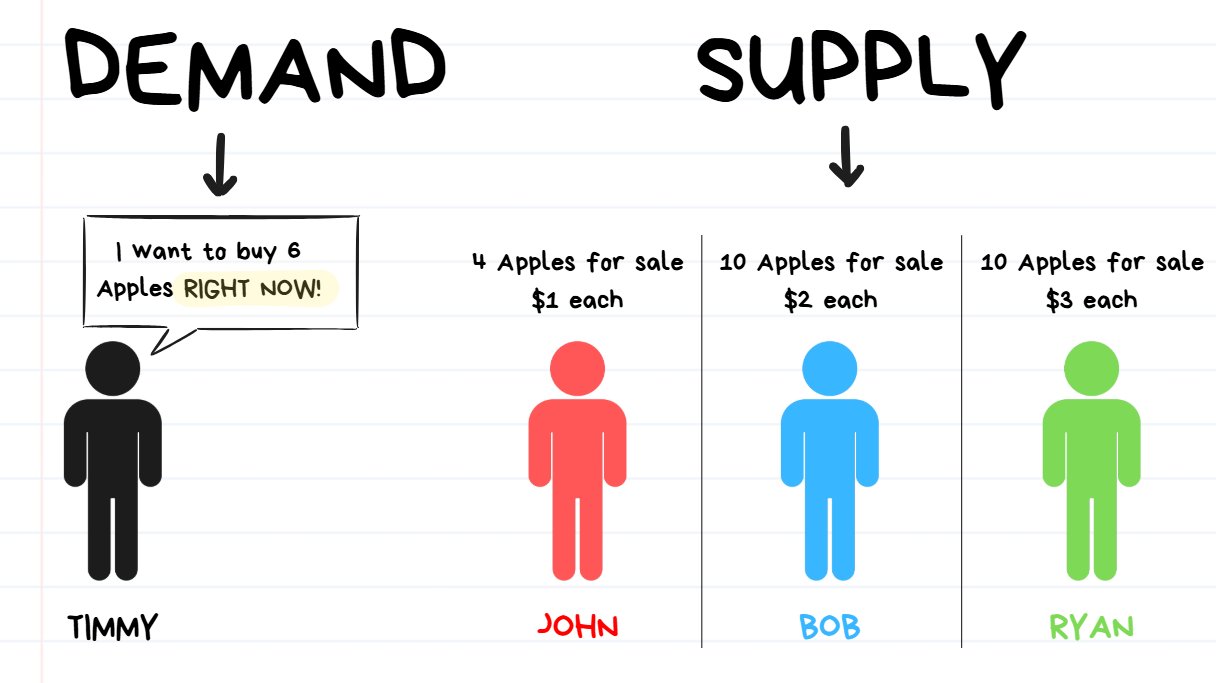

Example using Apples: 🍎🍎🍎🍎🍎

admire my beautiful creation on MS paint while you learning about order flow basics

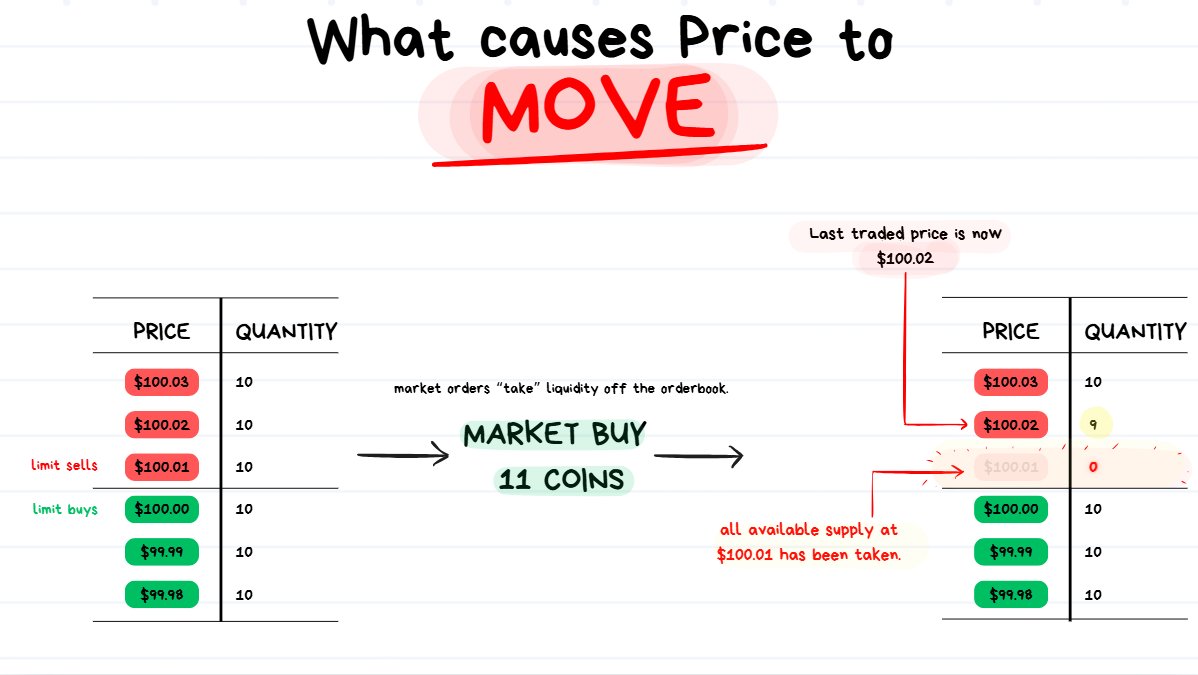

If you want to buy 1 apple NOW (market buy) , you will buy 1 apple from John at $10 since $10 is the cheapest “limit sell order) available at the moment.

The last traded price of “apples” will be $10.

Then you realize you actually needed 4 more apples to bake your apple pie, so you go out and “market buy” 4 apples.

You instantly buy the 2 remaining apples from John at $10 each. John has now sold out of apples.

The next best available price for apples is $11 and Bob has 10 apples for sale. So you buy 2 apples from Bob at $11 each. Bob now has 8 apples remaining at $11 each.

So what happened:

- you “market buy” 1 apple, price = $10

- you “market buy” 2 apples, price = $10 (all available supply is gone now)

- you “market buy” 2 apples, price = $11 (you pushed the price up)

A common Question that is often asked by traders is “Why did the Price go from A to B?”

- The only correct fundamental answer to this question is “because a bunch of market orders came through”

- There are an infinite # of possible reasons as to WHY traders were buying/selling. Some Examples: reacting to news, hedging a position, speculating on price action, arbitraging, blatant gambling etc.

- But we can never truly know the “why” because there will always be X% of information that is unaccountable for and impossible to collect/track/review.

- The only thing that we really know is that “market orders executed against resting limit orders, pushing the price from A to B”

Behind all the fancy indicators and lines on a chart is just an order book filled with makers (people who are advertising to buy/sell with limit orders) and takers (people who bite on the advertisement and execute a market order).

Ultimately, everything comes down to these 2 things:

- How much $ is there in limit orders? (supply)

- How much $ is coming through in market orders? (demand)

2) Market Structure + Regime Basics

Below I’m going to cover the following:

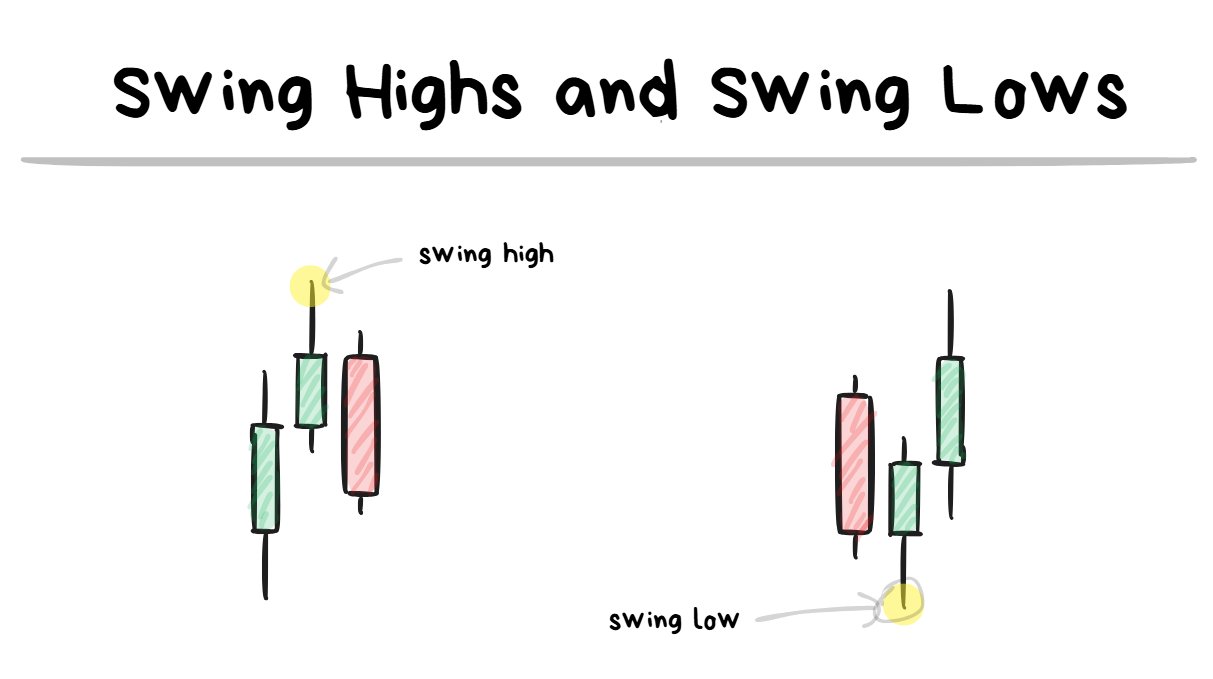

- Swing Highs and Swing Lows

- Bullish/Bearish Market Structure

- Breaks of Market Structure

- What is a Regime (market environment)

- Regimes on a “continuum”

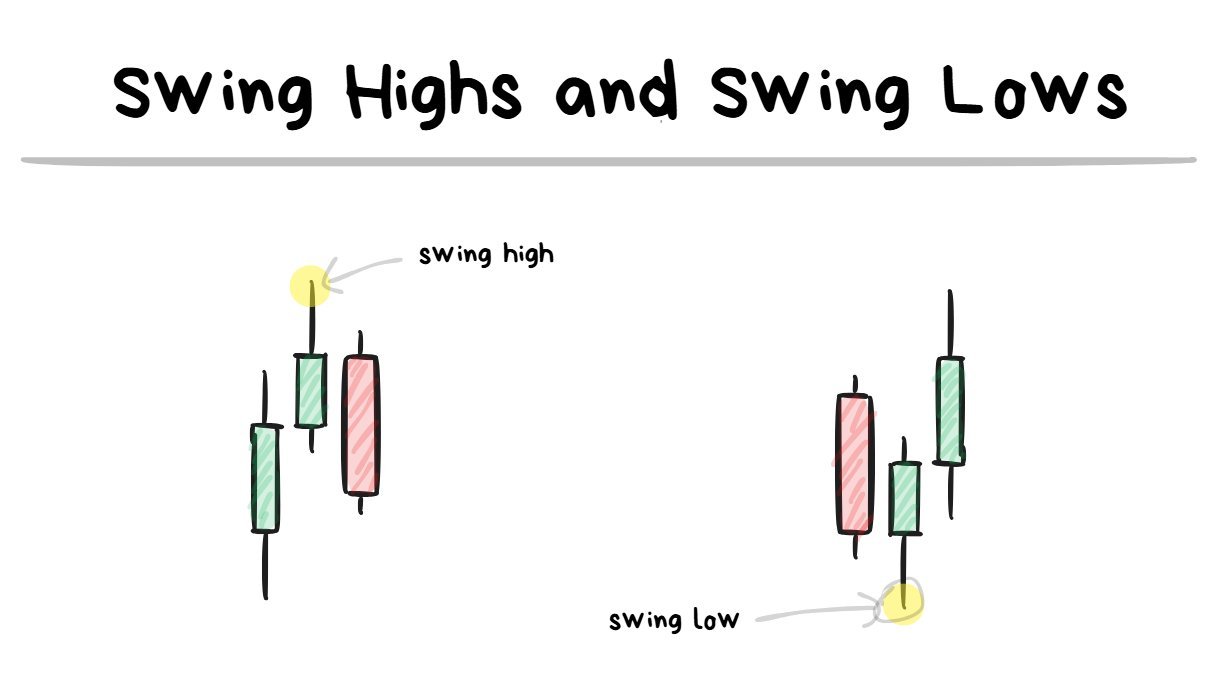

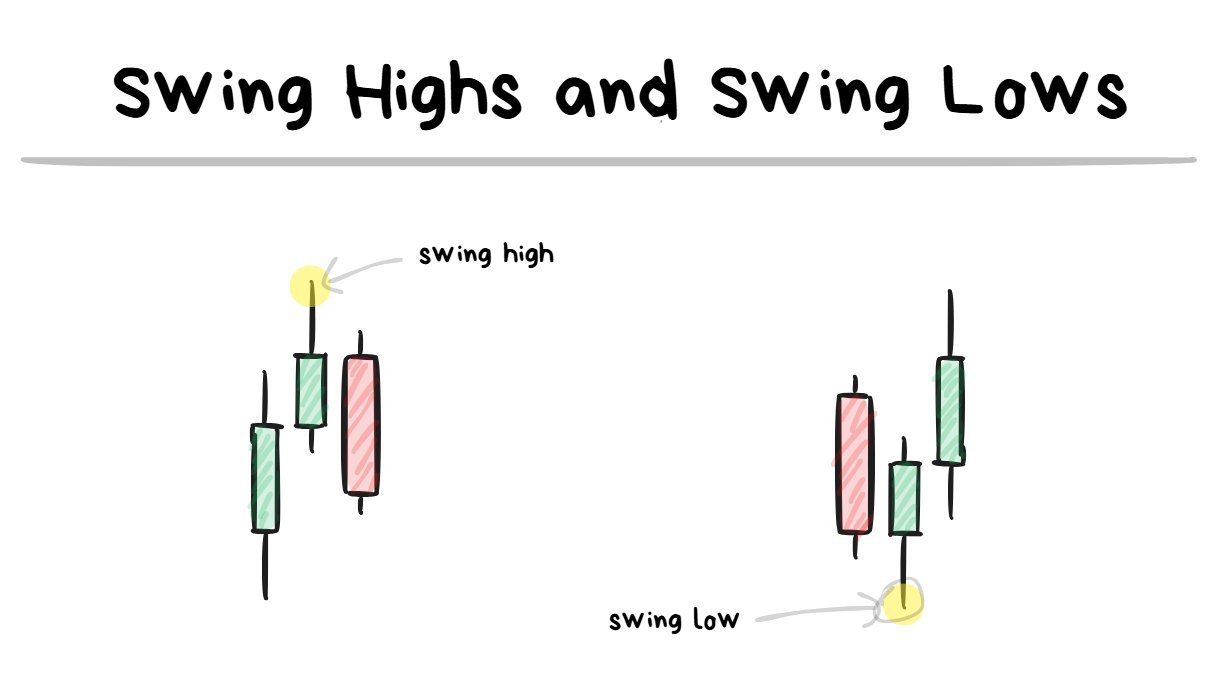

swing high/lows are turning points on the chart.

a low will look like a “V” and a high will look like an “upside-down V”

I believe the swing highs/lows are pretty self explanatory.

They are just previous turning points on the chart.

It requires at least 3 candles to form a swing level with the “extreme” being the level I look at.

the highs/lows in the diagram above are referring to “swing highs” and “swing lows”.

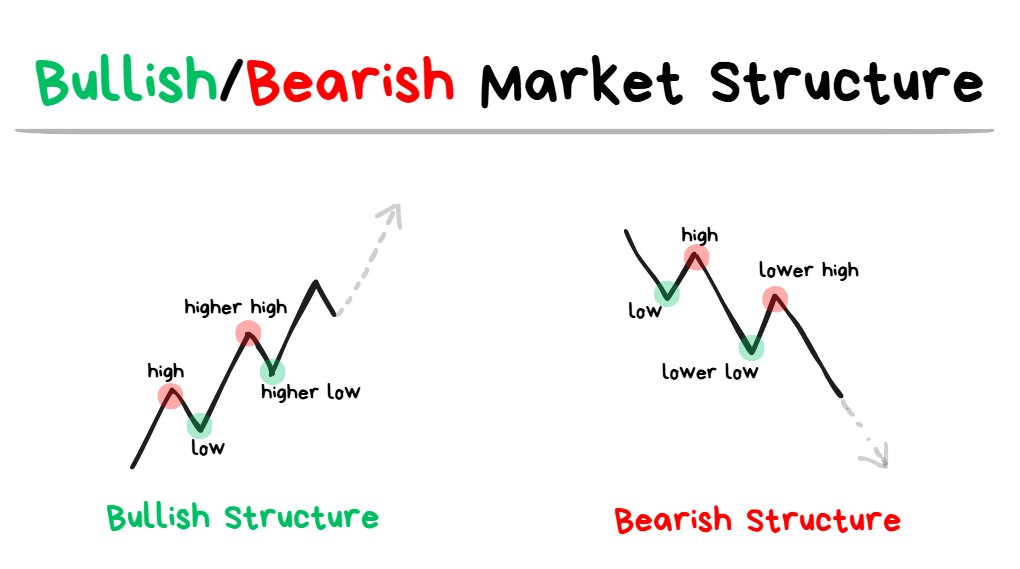

🐂Bullish Market Structure:

- Has higher highs and higher lows

- Expecting higher prices as long as structure remains in tact.

🐻Bearish Market Structure:

- Has lower highs and lower lows

- Expecting lower prices as long as structure remains in tact.

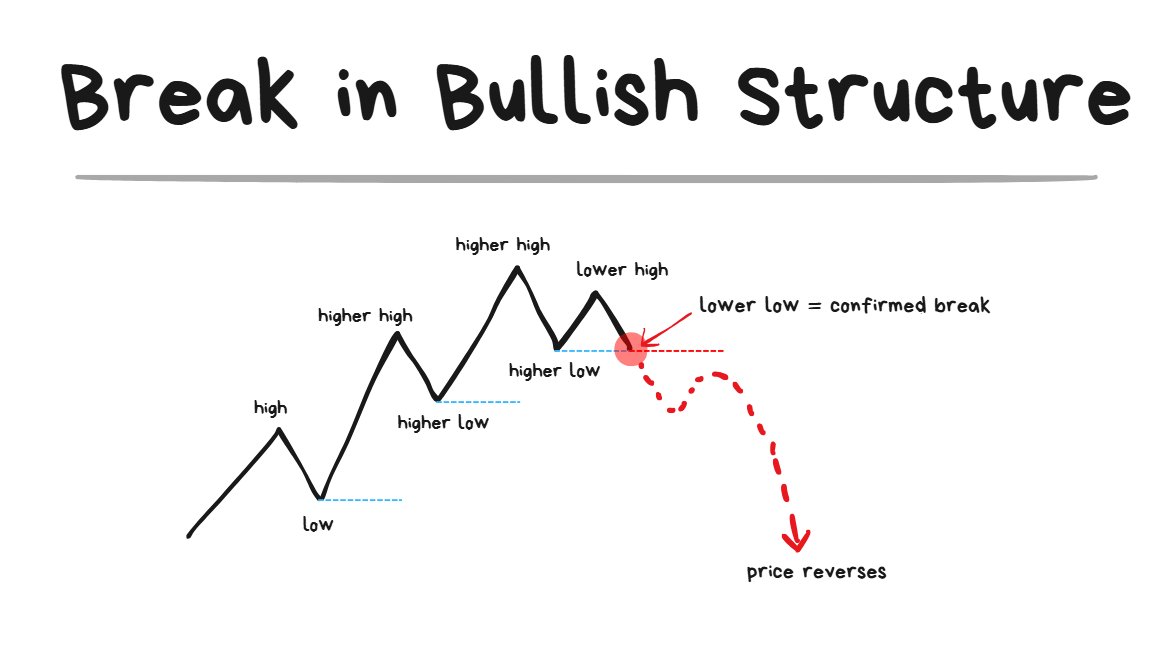

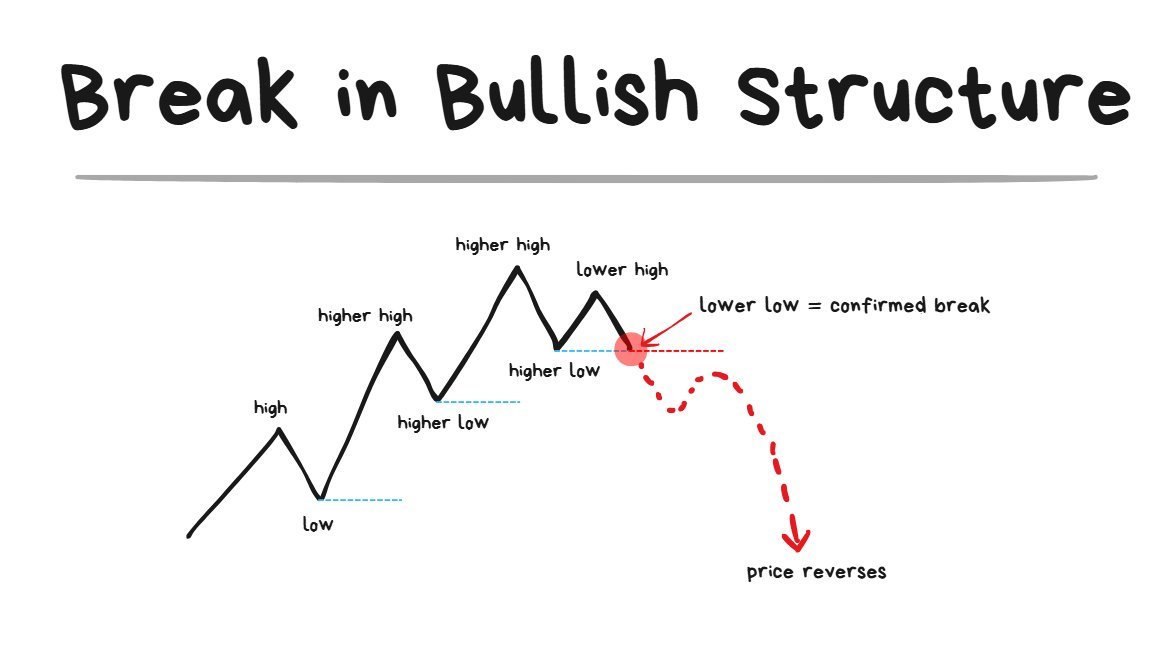

Break of Bullish Structure:

once the Lower Low comes in = the structure has broken.

- Just because a Lower High comes in does NOT mean the structure has broken yet

- The structure is only broken when the Lower Low comes in.

- A Lower Low = the breach of the most recent swing low that was formed.

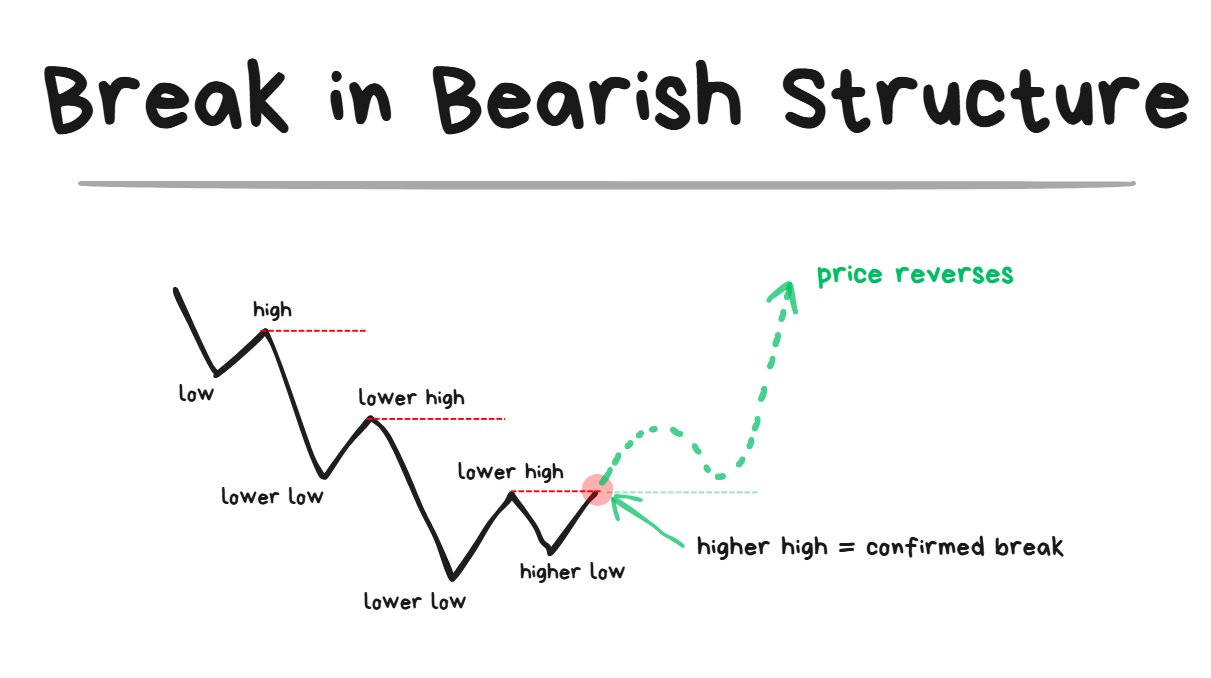

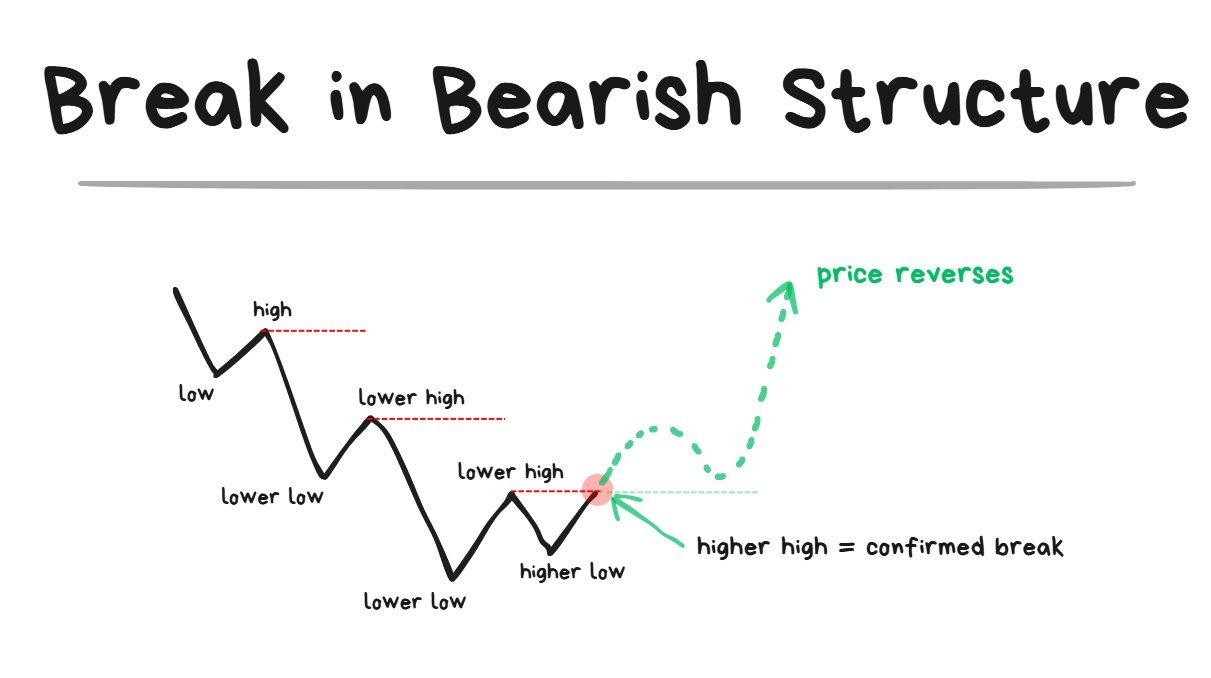

Break of Bearish Structure:

Once the Higher High comes in = the structure has broken

- Just because a Higher Low comes in does NOT mean the structure has broken yet.

- The structure is only broken when the Higher High comes in.

- A Higher High = the breach of the most recent swing high that was formed.

What Is a Regime?

A “Regime” is just a way to define a specific type of market environment.

Some regimes are more suitable for one style of strategies and other regimes are more favorable for other types of strategies.

Since market conditions change all the time, a big part of being a trader is being able to recognize the changes in regimes and adapt accordingly.

Jul 21, 2025

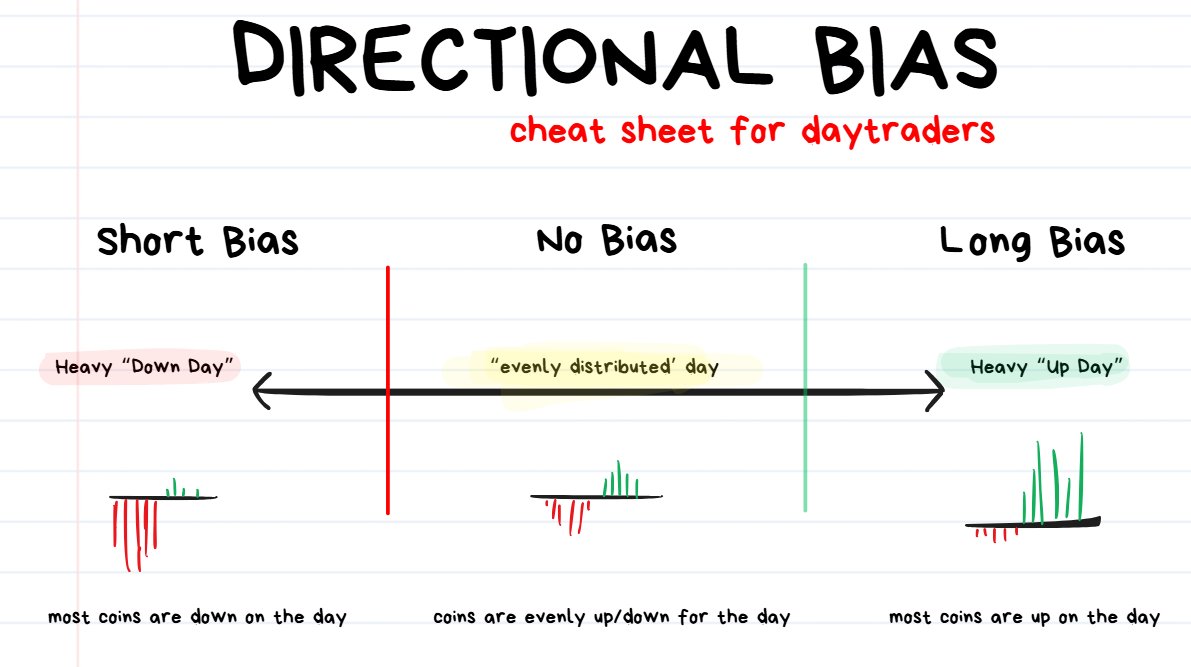

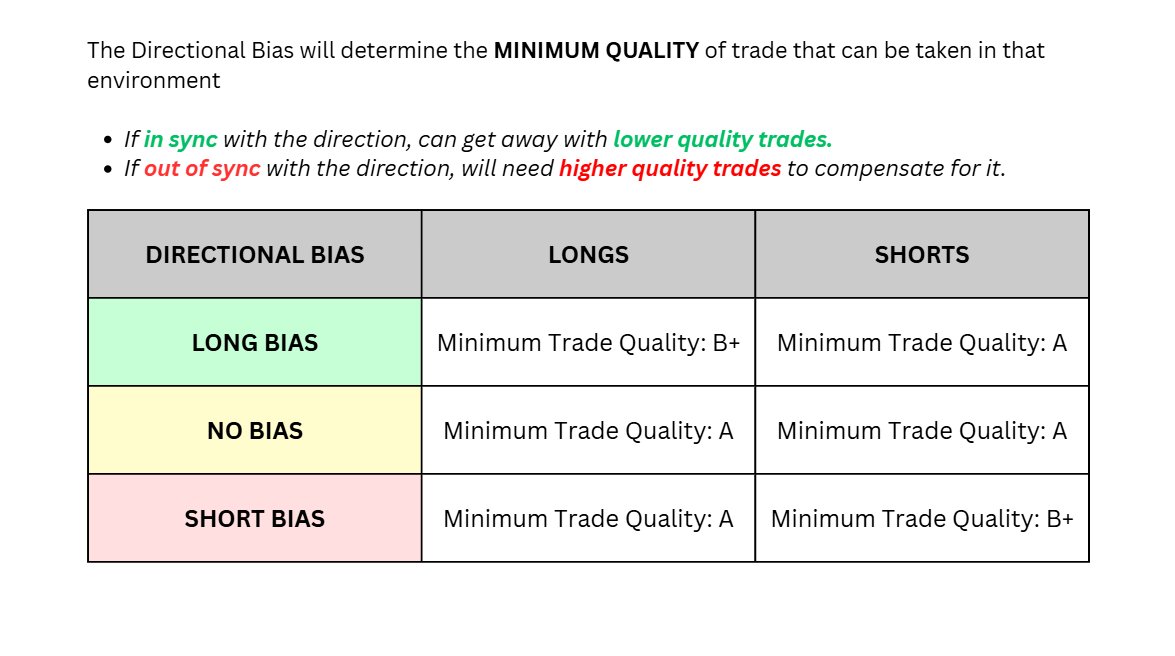

Creating a Market Bias If in sync: • risk more + trade more If out of sync: • risk less + trade less ↓

I like to have 2 types of biases I like to use:

- Directional (favored for longs or shorts?)

- Structural (favored for breakouts or reversals?)

If you were to look at any price action chart you may notice that a Break of Structure isn’t 100% guaranteed to result in a reversal.

Sep 10, 2025

My 2 favorite Trading setups ↓

In a Strong Bullish Trend: ❌

- as soon as price comes into the swing low, traders will quickly jump in to buy the discounted coin and price will accelerate higher.

- Betting on a reversal on a break of structure will NOT be ideal.

- Same logic applies to strong bearish trends too.

In a Weak, Sideways Choppy Range: ✅

- Price will continuously fail to break out of the major key levels

- As soon as the break of structure comes after the failure, the reversal is a lot more reliable.

The point: don’t obsess and try trade every single structural break. You’ll get burnt doing this in the wrong market environment. These work best in sideways environments.

Regimes on a Continuum

Sep 2, 2025

The 2 main Trading Styles I rely on explained↓

It’s not as simple as labelling a regime in a binary way. I’ve found it more helpful to think in terms of a continuum.

Examples:

- Sure a regime can be good for longs, but HOW GOOD is it?

- Sure a regime can be favorable for momentum trades, but HOW FAVORABLE is it?

- Sure price action can look choppy, but HOW CHOPPY is it?

The more clearly you can define the start/end points of a regime and also the changes in regimes = the easier trading will be.

Most traders obsess about optimizing their trading strategy but optimizing how you read the current market conditions (regime) is going to take you much further.

Summary of Stage 5

Once you understand the basics of Expectancy and Risk Management the next step is to learn the basics of price action.

Understanding how markets move with limit/market orders + market structure + regimes is a solid foundation to have.

Just remember:

- Directional Bias: up/down

- Structural Bias: trendy/choppy

If you can get a basic read on both then you can start developing a trading strategy to specifically take trades in 1 of those regimes.

Conclusion

Before you can have a profitable trading strategy, you will need a consistent trading strategy (which doesn’t need to be profitable yet).

In order to get from consistent strategy (unprofitable) to consistent strategy (profitable) you will need an “improvement process” where you come up with ideas, collect data on those ideas, review the data and make iterations accordingly.

Before you can have a consistent strategy (unprofitable) you will need to have some kind of strategy (but it doesn’t have to be consistent). The way to go from inconsistent to consistent is to get clearer definitions on your entry/exit rules + get a bit more systematic with the trade execution.

Before building a strategy you’re going to need to learn the absolute basics of how markets move (limit/market orders) and some price action basics. Your strategy should be built around performing well in ONE specific regime.

Final Words

Well done for pushing through this article. This was a pretty lengthy one.

Now you should have a bit more clarity on how my own trading journey looked like and maybe you can use parts of it as inspiration to replicate in your own.

If you really did take the time to read through this, then don’t hesitate to comment any questions.

I will take my time to go through ALL questions you guys put into the comments. Don’t be shy.

Good luck trading~ 🤝

Source

Written by @spicyofc · View original post · Published: 2025-07-31 �������������������������������������������������������������������������������������������

Price Action + Market Structure Masterclass

I’m a former Prop Trader and I’ve been trading Crypto for 8 years.

Basic understanding of price action concepts is something that every good trader that I’ve spoken to has in common.

So the goal of this article is to try simplify the basics and pass it over to you. 🤝

Here is everything that you’re going to get in this Article ↓

- Lesson 1: How does Price actually move?

- Lesson 2: Support and Resistance

- Lesson 3: Ranging Structure and Trending Structure

- Lesson 4: Live Trade Examples + 5 Bonus Resources

**🤓**NOTE TO READER: I have done my best to simplify all of these concepts as much as possible. Enjoy~

Lesson 1: How Does Price Actually Move?

orderbook

🤓NOTE TO READER: There is a reason why I want to cover this lesson first.

Unfortunately the majority of Traders don’t actually understand the causes for price moving up/down.

There are even some Traders out there who believe that the elites of society created a dark secret predatory algorithm which controls all the price movements in the market and it is designed to hunt stoplosses at certain times of the day….(yes seriously… there are surprisingly a large number of people out there who actually believe this.)

I can assure you, the market is not a “super coded algorithm by the elites”… it is a lot more like an auction at eBay.

If the most basic understanding of markets is incorrect or misguided, then all other ideas that the trader is going to come up with are going to be sitting on a very unstable foundation.

The goal of this lesson is to at least get the basics right. That’s it.

Okay let’s jump into the lesson ↓

This lesson will cover:

- What even is a “Market”

- Makers and Takers (limit orders/market orders)

- What causes the price to move and how does it happen

What Even Is a “Market”?

As soon as someone is willing to buy something, a market now exists for that something.

- If someone wants to buy a specific Pokemon card, then there is a “market” for that specific Pokemon card.

- If someone wants to buy an apple, then there is a “market” for apples.

- If someone wants to buy a burger, then there is a “market” for burgers.

- If someone wants to buy crypto shitcoins, then there is a “market” for crypto shitcoins.

A thing doesn’t need to be listed on an exchange with fancy candlestick charts and liquidity providers for it to have a market.

As long as someone wants to buy something then a market technically exists for it.

Makers and Takers (Limit Orders / Market Orders)

order types cheat sheet

In ALL markets there are Makers and Takers.

Maker:

- someone who is advertising to buy or sell “something” at a specific price.

- Example: “Bob is willing to sell 2 apples for $1 each.”

- The Maker may need to patiently wait for another market participant to see their advertisement and make a transaction with them.

Taker:

- The Taker is someone sees the advertisement of the Maker and agrees to the price.

- They will make the transaction with the Maker at whatever price the Maker wanted.

- But the Taker gets to decide on the quantity of how much of the thing they wanted to transact.

- Example: “Timmy agrees to Bob’s price of apples at $1 each, but Timmy only purchases 1 apple. Timmy gives Bob $1 and immediately receives 1 apple in exchange.”

In the Crypto Markets, “Makers” are those who are putting limit orders onto an orderbook. If you were to put in a “limit buy order for 1 BTC at $90,000” then you order will be sitting on the orderbook until price drops down to it.

❗️TIP: “Liquidity” is just a fancy way of saying “how much money is there sitting in limit orders.”

“Takers” are the ones who will be using market orders to execute against the resting limit orders. When you execute a Market Order, you don’t get to choose the price that you get. If you want to “market sell 1 BTC”, your order for 1 BTC will execute at whatever the best limit buy orders are available at the time.

What Causes Price to Move?

Market moves based on Supply and Demand at certain price points.

- Supply = Limit Orders (from makers)

- Demand = Market Orders (from takers)

Below I’m going to explain Supply/Demand using an analogy with Apples 🍎↓

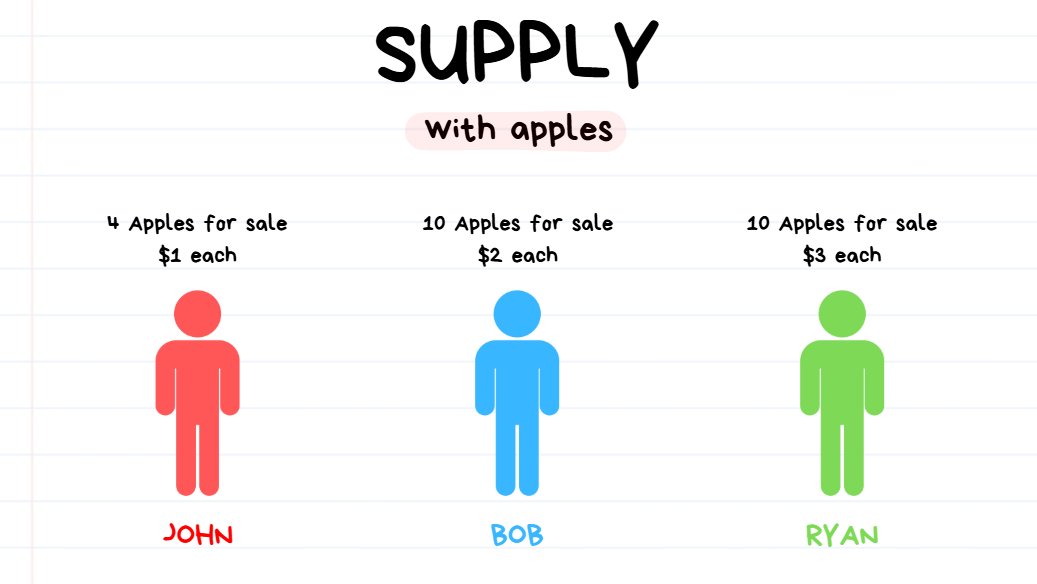

3 traders providing liquidity to apples. (supply)

There are 3 Makers (advertising to sell a specific price/quantity) for Apples:

- John has 4 apples for sale at $1 each.

- Bob has 10 apples for sale at $2 each.

- Ryan has 10 apples for sale at $3 each.

a taker (demand, in the form of market orders) has appeared.

↑ Timmy the Taker has appeared!

Timmy wishes to buy 6 apples immediately. He doesn’t care what price he gets, he just needs 6 apples to cook the best apple pie.

In order for Timmy to act on his intent, he will need to execute a Market Buy for a quantity of 6 apples.

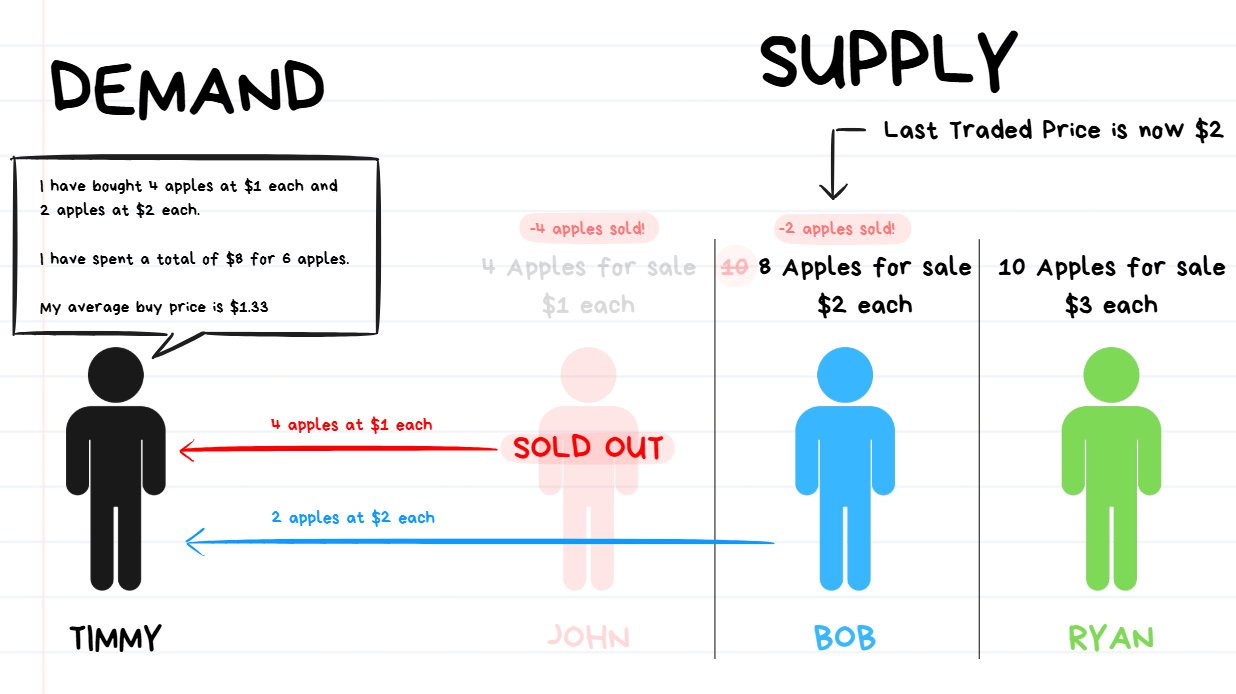

market order for 6 apples has been executed. price moves from $1 up to $2.

Once Timmy executes a Market Order for a quantity of 6 apples, this is what will happen:

- First Timmy’s order will take from the best available limit sell order. This will be the 4 apples from John at $1 each.

- However since John only has 4 apples for sale and Bob wants 6, Bob will eat through ALL of Bob’s supply. Timmy still has 2 apples left to buy.

- The next best available price will be $2 each from Bob. So Timmy will purchase the last 2 apples from Bob.

So Timmy bought 4 apples at $1 each ($4 of liquidity taken) and took all the available supply.

Then Timmy bought another 2 apples at $2 each from Bob ($4 of liquidity taken).

So BEFORE Timmy placed the order, the price of apples was $1.

AFTER Timmy’s Market order finished executing, his order resulted in pushing the price from $1 up to $2 because he ate through all the supply.

❗️TIP: So basically whenever demand exceeds supply at a certain price point, the price will move.

Summary: Lesson 1

Price doesn’t move because of secret algorithms. It moves because of supply and demand between buyers and sellers.

- Markets: A market exists anytime someone wants to buy or sell something. It can be apples, Pokémon cards, or Crypto.

- Makers (limit orders): Provide liquidity by advertising prices they’re willing to buy/sell at.

- Takers (market orders): Remove liquidity by accepting those prices immediately.

Price moves when market orders (demand) consume the available limit orders (supply) at a given price. If a large market buy eats through all sell orders at $1 and starts filling $2 orders, the price rises to $2.

👉 In short: Price = the result of market orders hitting the orderbook.

Lesson 2: Support and Resistance

The topic of support/resistance is a rather simple topic.

Unfortunately, Traders have a unique talent for finding ways to overcomplicate basic concepts and confuse themselves in the mess that they have created.

The goal of this lesson is get crystal clear clarity on Support/Resistance and remove any potential confusions.

This lesson will cover:

- Stop thinking about Magical Lines, start thinking about Limit Orders

- Order Size relative to Volatility

- Swing Highs and Swing Lows

Stop Thinking About Magical Lines, Start Thinking About Limit Orders

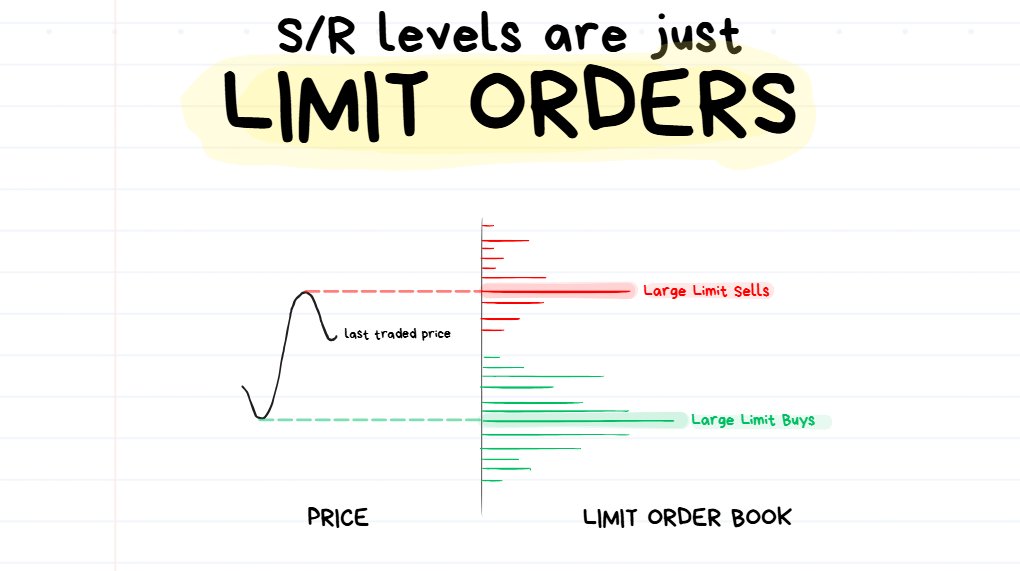

price isn’t bouncing from the lines you draw. It’s bouncing from limit orders in the orderbook.

Out in the vast space of social media are a whole bunch of influencers who try to create fancy-sounding ways of drawing different types of support/resistance levels.

Behind all the fancy “order blocks” and “price delivery zones” (or whatever other terms are used) is literally just a bunch of limit orders.

Ultimately, as discussed in the previous lesson, price moves purely based on Limit Orders and Market Orders.

So price is never bouncing off the “magical lines” (or boxes) that you draw on your chart. It is bouncing off the limit orders on the orderbook.

❗️****TIP: The lines that we draw on the chart are just to help us visualize where large clusters of limit orders are sitting.

You will often find big clusters of Limit Orders near previous big turning points in the price action.

The thing is I could draw a random line anywhere on the chart and behind it are probably going to be some limit orders.

This means you can draw literally any line on your chart and you could technically call it a valid support or resistance level.

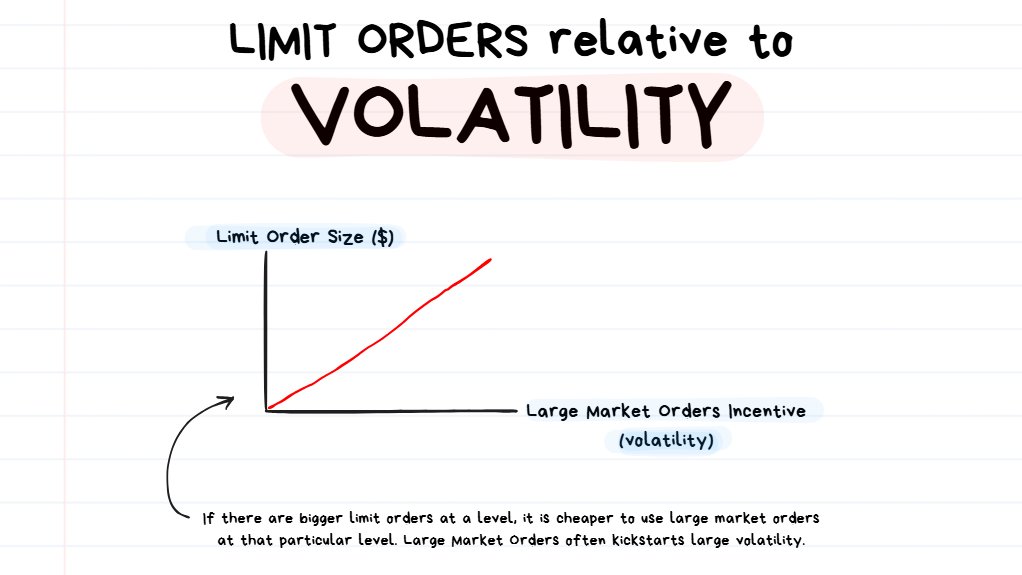

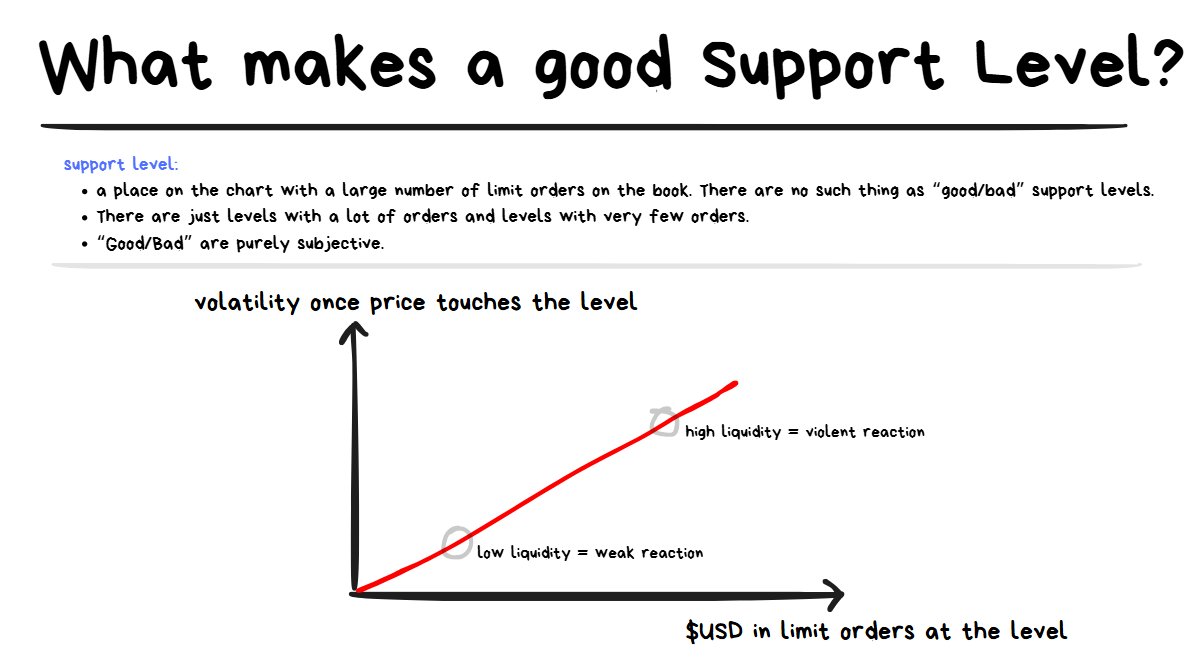

Order Size Relative to Volatility

The bigger the advertisement, the louder the market gets after a sale occurs.

If there’s a lot of money in limit orders at 1 price, there’s more incentive to use market orders at that point since the slippage for large orders is at its lowest.

Since market orders are responsible for moving price up/down, we can expect to see a lot of movement once price hits a large limit order and starts moving away from it.

- This means that sometimes price can come into an “interesting looking” level but it just has very few limit orders there… meaning it’s not likely to have a violent reaction to the level.

- This also means that a big limit order can be placed at a very strange and unexpected place in the chart and have a big impact on price action once the price reaches that point.

Quick Summary (with a Hot Take🔥)

So basically there’s no such thing as “strong levels” or “weak levels”… yep I’ve said it. 🤷♂️

It’s not about “weak” or “strong”, it’s just about how much $$ in limit orders is sitting at a level relative to the other nearby limit orders.

More money sitting at a level in limit orders does not necessarily mean a higher likelihood of a “bounce” from the level (which is most commonly assumed).

It just means that we can expect to see a more volatile reaction once price gets closer to the level since big limit orders often incentivize big market orders to come through, which then cause big price movements.

- This means if a reversal happens from a level with huge orders, it’s likely to be a very violent reversal.

- If a breakout happens at the level with huge orders, it’s likely to be a very violent breakout.

If there’s very small limit orders at a level, then regardless if the price reverses or does a breakout it’s unlikely to be a wild move because there just isn’t “that much fuel for the fire to use.”

🧠3 BONUS TIPS ↓

❗️TIP #1: Big/Round Numbers which are in multiples of 10 (e.g. $1, 10, $10, $50… etc.) often have large limit orders stacked on them. This is why we see frequent violent reactions from these levels.

❗️TIP #2: For more advanced (or curious) Traders, you can use the platform @tapesurfapp to see where the limit orders are. I’m not affiliated with them in any way, I just think their platform is super cool.

❗️TIP #3: The more time that price has spent away from a level = the more time the market as a whole has to place limit orders at that level = the bigger the reaction can be expected once price returns to that level again.

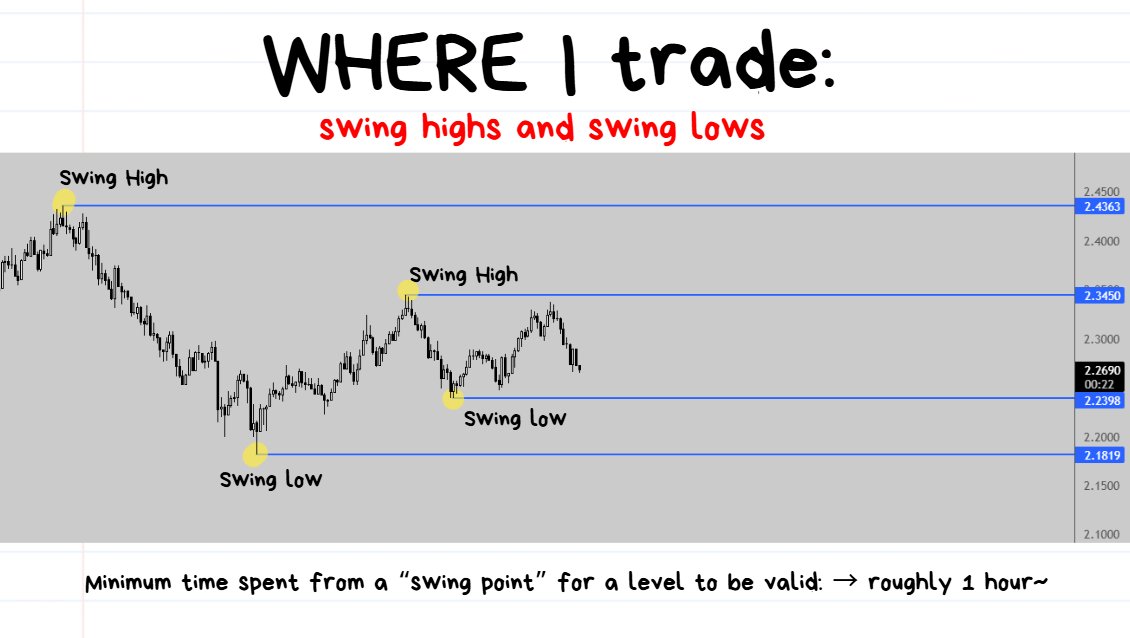

Swing Highs and Swing Lows

**🤓**NOTE TO READER: A swing point (high or low) requires at least 3 candles to be formed. Swing highs is when the 2nd candle has the highest extreme and a swing Low is when the 2nd candle has the lowest extreme.

These are the easiest price-action based support/resistance levels to use because of how simple it is to identify them and be consistent when using them.

I want to give some Simple Examples of using swing highs/lows below ↓

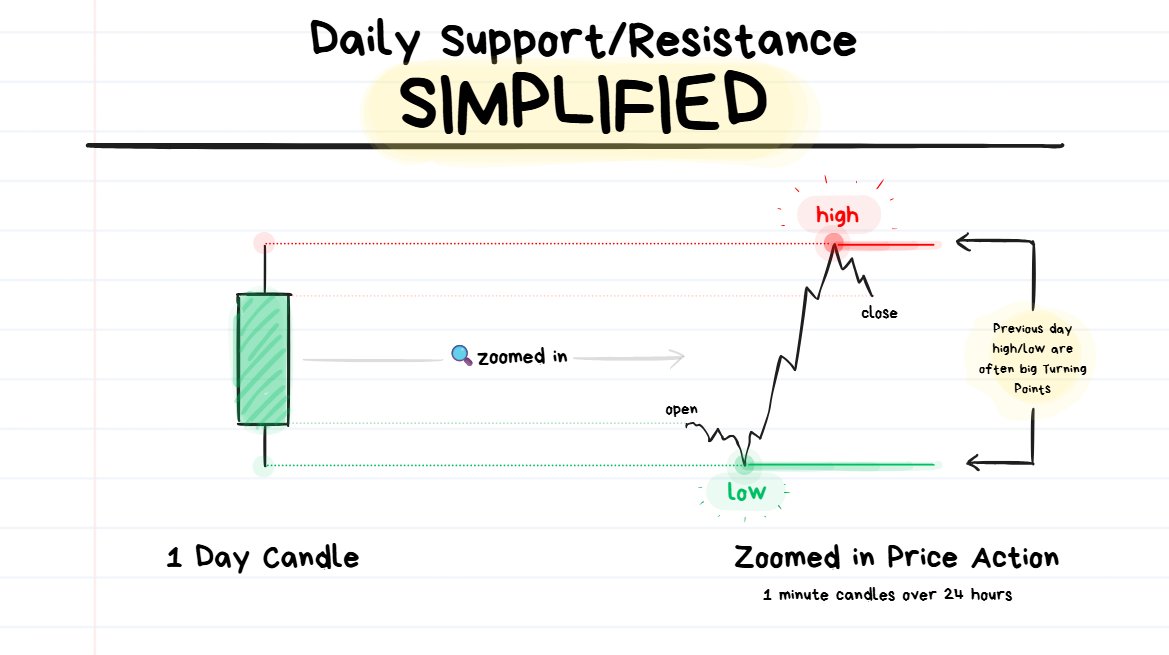

When you are looking at a 1 Day Candlestick and then you zoom into it by changing timeframes, you will get a chart which looks like something on the right hand side of the image above.

The highest and lowest points of the day often have a lot of limit orders placed near them.

A lot of market participants make their decisions based on the highest and lowest points of the day.

It is a frequent used area for traders to enter trades and also exit trades, which often causes there to be a lot of activity around these types of levels.

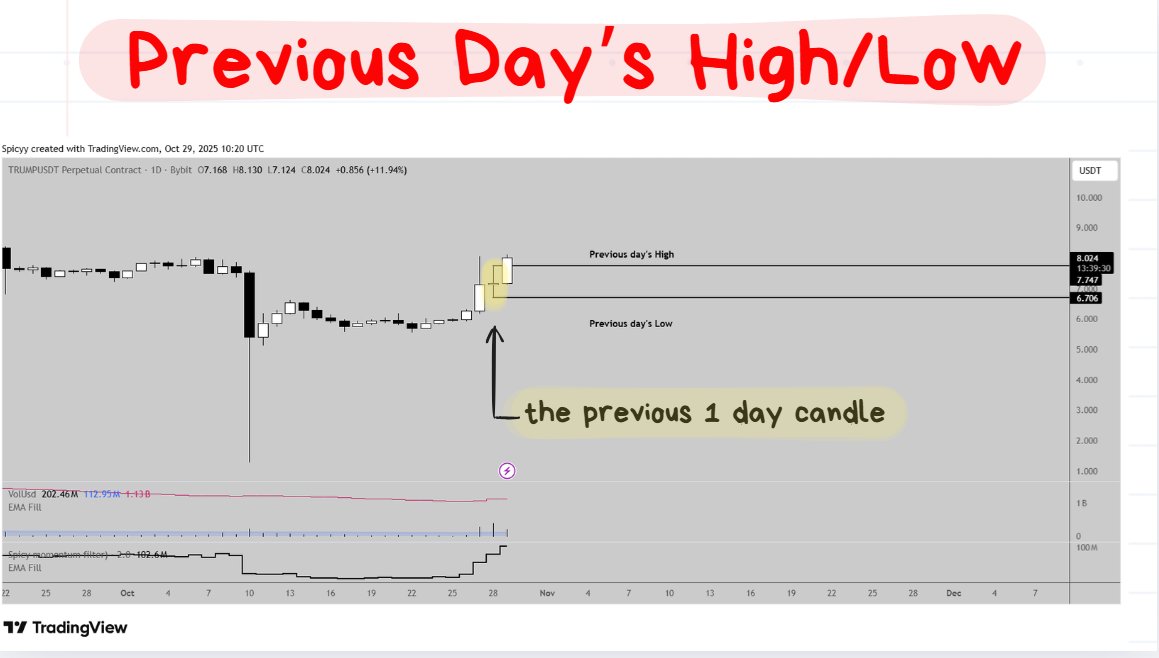

📚EASY EXAMPLE #1: Daily Highs/Lows

https://www.tradingview.com/x/HZgYO69I/

The Previous Day’s High/Low is one of my favorite S/R levels to trade from because of how easy it is to be consistent with execution.

When levels are drawn in the exact same type of way for every single trade, the trades become more consistent.

❗️****TIP: The High/Low of the previous X units of time will always appear as a swing high or a swing low. This is because it is only looking at the extreme points.

As executed trades become more consistent, the trades become easier to review and make improvements to.

green/red dots (previous day’s high/low) were the key turning points for that 24 hours.

When you zoom into the previous day’s candle by switching to a different timeframe you’ll often be able to see how the previous day’s highs/lows were key turning points throughout the day.

When price returns to a place where a lot of volume was previously executed (which are often the key turning points), it often has a lot of volume executed there once again.

This is why we so often see more violent reactions once price reaches one of these key levels.

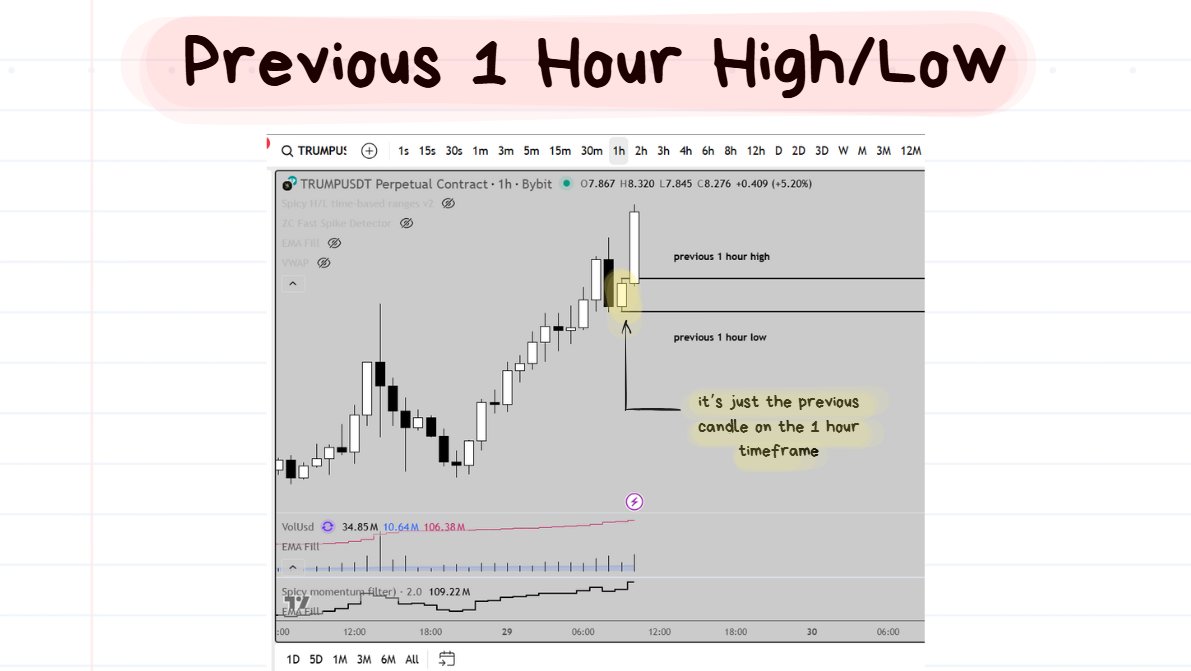

📚EASY EXAMPLE #2: Previous 1 Hour Swing Highs/Lows

timeframe: 1 hour

Super simple:

Switch to the 1 hour timeframe.

Find the high/low of the previous 1 hour.

❗️****TIP: You can use the Magnet Tool (bottom left hand corner of tradingview) to “snap” to the highs/lows.

Then Zoom into the 1 minute timeframe. ↓

https://www.tradingview.com/x/sj72rlov/

The idea here is the same as the 1 day candles. The highest and lowest points of the previous 1 hour can often have violent reactions.

Summary: Lesson 2

Support and resistance aren’t “magical lines”. They are just clusters of limit orders.

- Core idea: Price reacts at levels where large limit orders sit. The lines we draw only visualize these areas of liquidity.

- Order size vs volatility: Bigger limit orders = bigger reactions once hit. It’s not “strong” or “weak” levels. What matters is just how much money is sitting there relative to nearby prices.

- 3 Tips: - tip1) Round numbers (e.g. $1, $10, $100) often have stacked orders. - tip2) Use tools like TapeSurf to see real limit orders on multiple exchanges. - tip3) The longer price stays away from a level, the stronger the reaction when it returns.

- Swing highs/lows: Simple, consistent S/R levels formed by 3 candles (middle one is the extreme). Daily highs/lows → high activity, great for consistency. Hourly highs/lows → good for intraday reactions.

👉 In short: Support/resistance = where real money (limit orders) sits. Trade from clear swing highs/lows and round-number levels if you want to simplify your execution and also make it more consistent.

Lesson 3: Ranging Structure and Trending Structure

Sep 2, 2025

The 2 main Trading Styles I rely on explained↓

In this lesson we’re going to cover:

- Market Structure

- Break in Market Structure

- Mean-Reverting Markets (ranging)

- Momentum Markets (trending)

- **🧠**Margin of Error (important concept)

🤓NOTE TO READER: Before diving into the lesson I want to give some quick context.

When price approaches any support/resistance level we as Traders have 3 types of decisions that we can make:

- 1 ) I bet that price will break through this level (Momentum)

- 2 ) I bet that price will bounce off this level (Mean Reversion)

- 3 ) I don’t want to bet at all. (No Trade Taken)

Before we take a trade, we have to assess multiple variables to see which of these 3 decisions is the most appropriate to make at the time.

As a Trader you have to get used to picking Option 3… a LOT.

Okay let’s get into the Lesson now ↓

Market Structure

Apr 15, 2025

Market Structure a Simple and Easy thread

Before jumping into a trade it can be quite helpful to have a little bit of context.

Looking at the current Market Structure is a good place to start.

- 🐂Bullish Market Structure: higher highs and higher lows.

- 🐻Bearish Market Structure: lower lows and lower highs.

❗️TIP: Look at the swing highs and swing lows created in the price action when trying to judge the market structure.

Break in Market Structure

Just because price currently has Bullish Structure doesn’t mean that it will just go up forever.

There are going to be times where the structure “breaks” and price can potentially turn around and start moving in another direction.

- Just because a Lower High comes in does NOT mean the structure has broken yet

- The structure is only broken when the Lower Low comes in.

- A Lower Low = the break of the most recent swing low that was formed.

- Just because a Higher Low comes in does NOT mean the structure has broken yet.

- The structure is only broken when the Higher High comes in.

- A Higher High = the breach of the most recent swing high that was formed.

Live Trade Example of using a Break of Structure ↓

Oct 17, 2025

$IP Break of structure after spiking (and almost immediately rejecting) the big $6 level. have a tight FTA on this one (lowkey am thinking that X is not the best place for posting setups… )

Mean-Reverting Markets (Ranging)

❗️****TIP: **“**Mean Reversion” means “reverting back to the mean” or “reversing back to the average/middle price.”

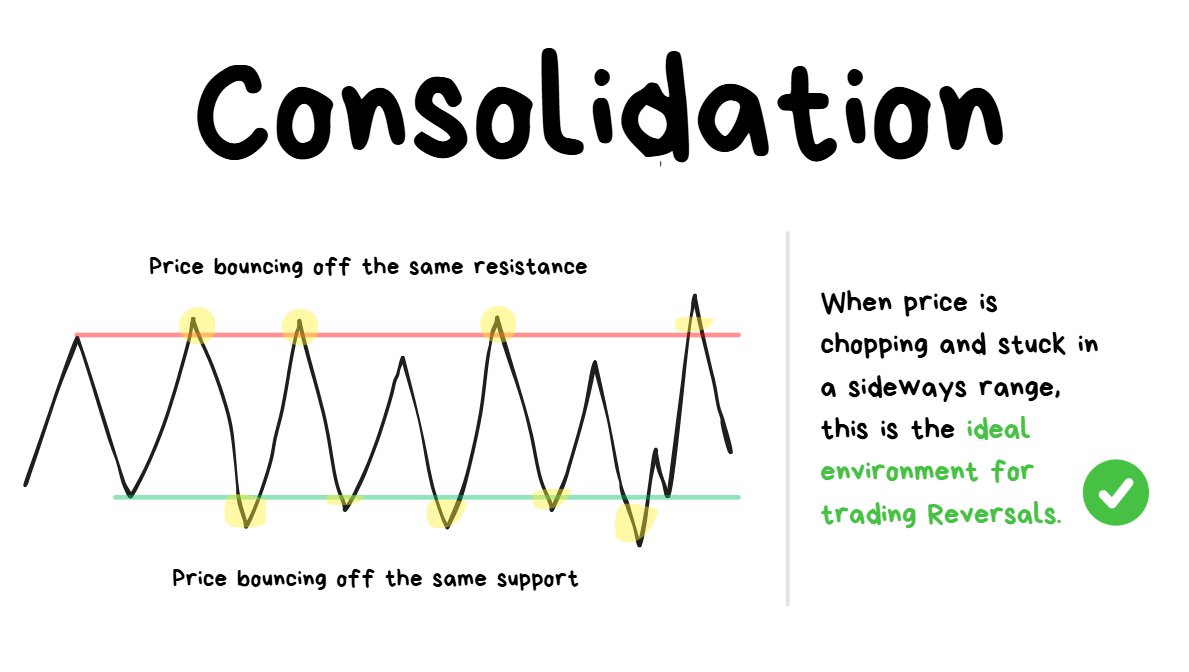

When the direction of price isn’t clear because it just keeps reversing from the same highs/lows over and over again, this is a Mean Reverting Environment.

This type of environment is:

- ✅the BEST for trading reversals

- ❌the WORST for trading breakouts

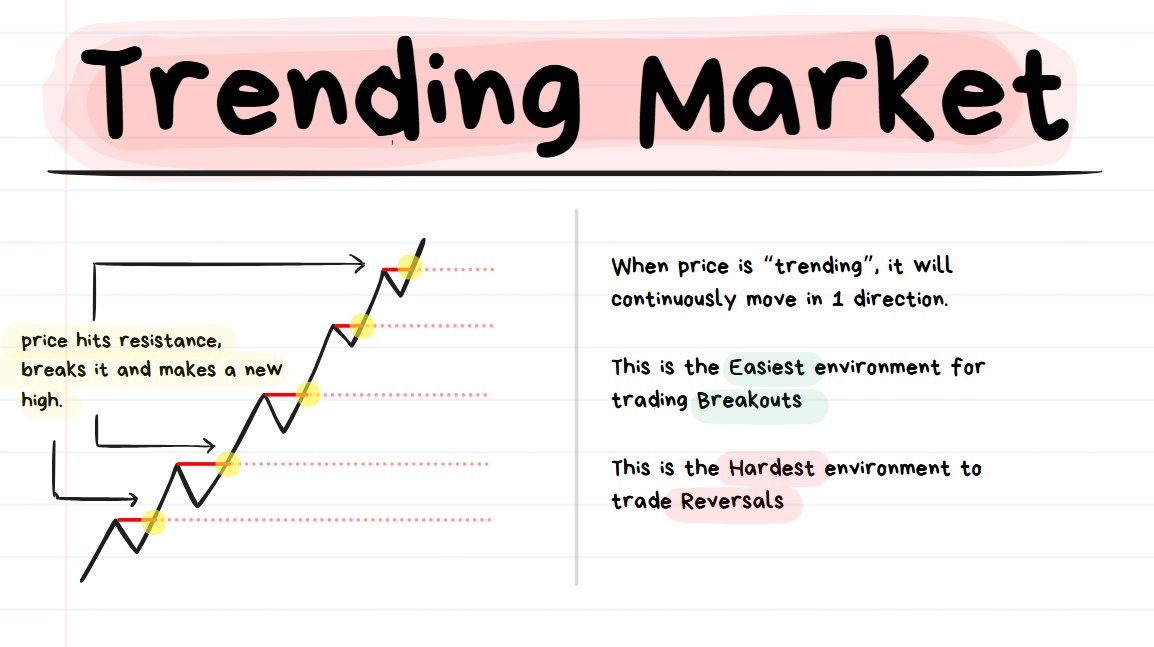

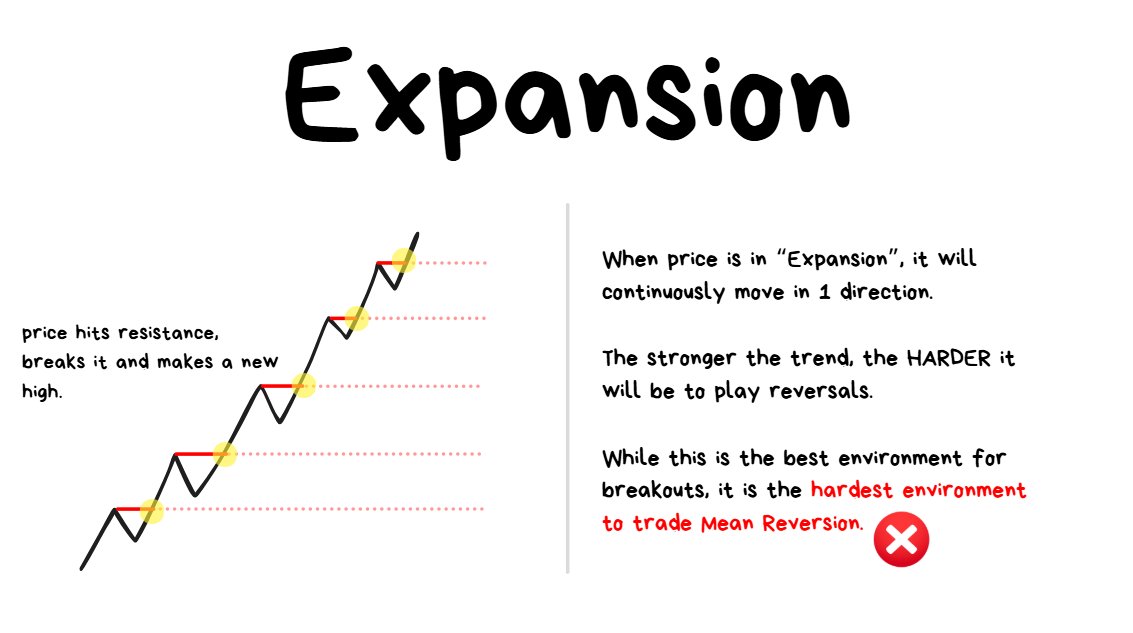

Momentum Markets (Trending)

❗️****TIP: “Trending” means that price is consistently moving in 1 direction. If it’s an up trend then price is consistently going up and if it’s a down trend then price is consistently going down.

When the Market Structure of a move appears to be Bullish or Bearish for a consistently long duration of time (it’s more about total # of candles rather than units of time, since this concept holds true for all timeframes), then you’re looking at Trending Price Action.

Common characteristic of strong Trending Price Action:

- Price hits a resistance and then effortlessly breaks through it, drifting to the next resistance.

- Then when it reaches the next level, it breaks through that again and the cycle continues.

This type of environment is:

- ✅the BEST for trading breakouts

- ❌the WORST for trading reversals

🤓NOTE TO READER: This next concept had a huge impact not just on my trading but also in the overall quality of my decision-making. Of all the things discussed in this article, I hope this specific concept is the one that gets retained in your memory.

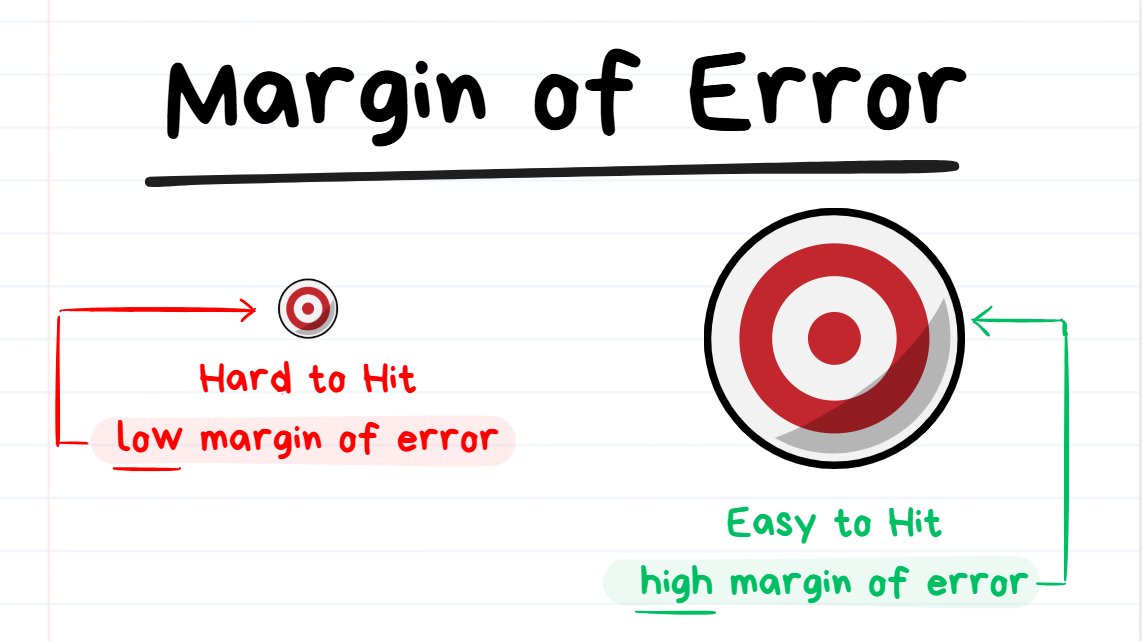

🧠 Margin of Error

If your goal was “just hit the target”, it would make more sense to play on the 2nd Target rather than the 1st Target.

There is a reason why some environments are great for reversals and others are great for breakouts.

The reason is due to the “Margin of Error” that’s available.

- High Margin of Error = there’s a lot of breathing room for mistakes. You can make errors and still get away with it.

- Low Margin of Error = there is barely any breathing room for mistakes. You need perfect execution and even the slightest error will result in failure.

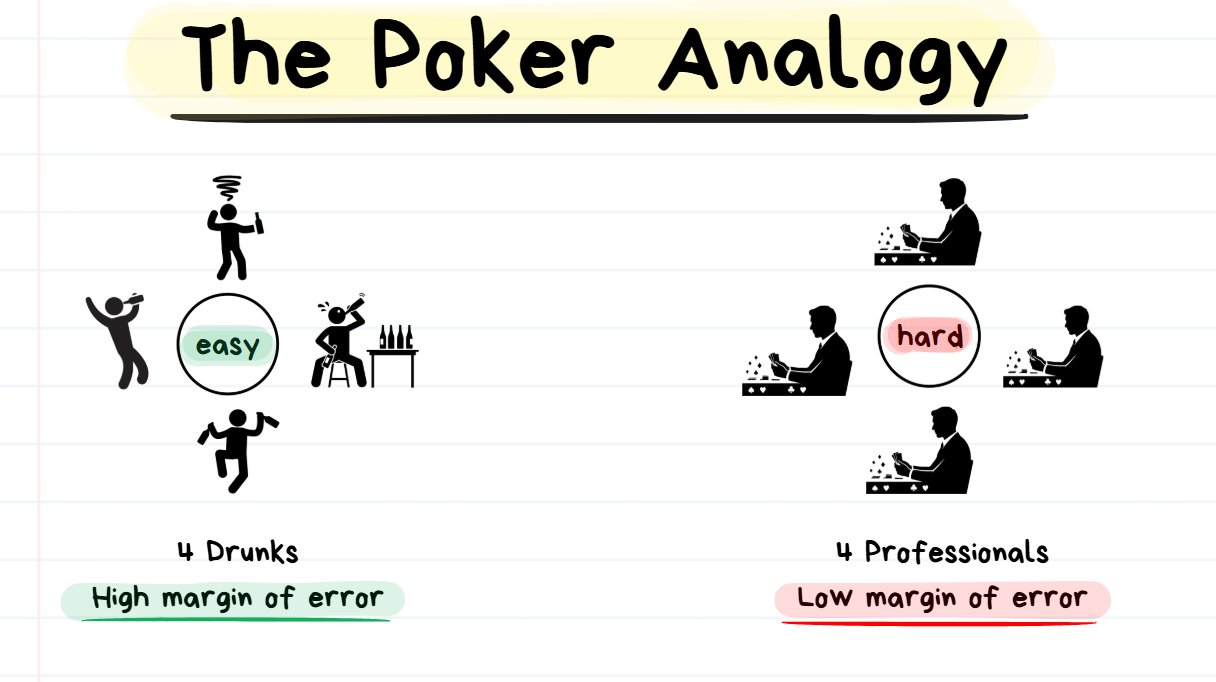

I want to quickly give the Poker analogy for this ↓

If your skill is the same but you play in an easier environment = you will have a higher earning potential.

- Saturday Night: Imagine playing Poker against 4 drunk players on a Saturday night

- Tuesday Morning: Imagine playing poker against 4 professionals on a Tuesday morning

Despite you having the exact same level of execution skill, it’s more likely that you perform better against the 4 Drunk Players rather than the 4 Professionals.

With the 4 Drunk Guys, you can make plenty of mistakes and you won’t be exploited for them. They will make plenty more errors than you, so you just have to be there to take advantage of the mistakes. Your margin of error is HIGH in this situation.

With the 4 Professionals, every mistake you make is a really big deal. You will be punished very harshly for every error and you will need to play perfectly. Your margin of error is LOW in this situation.

Imagine that BOTH situations (playing against the drunks or the pros) had the SAME PAYOUT… Then it would be a no-brainer to just only play against the drunks and to stay away from playing against pros.

🤓NOTE TO READER: Below I will explain how Margin of Error is relevant in Trading ↓

betting on Outcome #2 is easier than Outcome #1

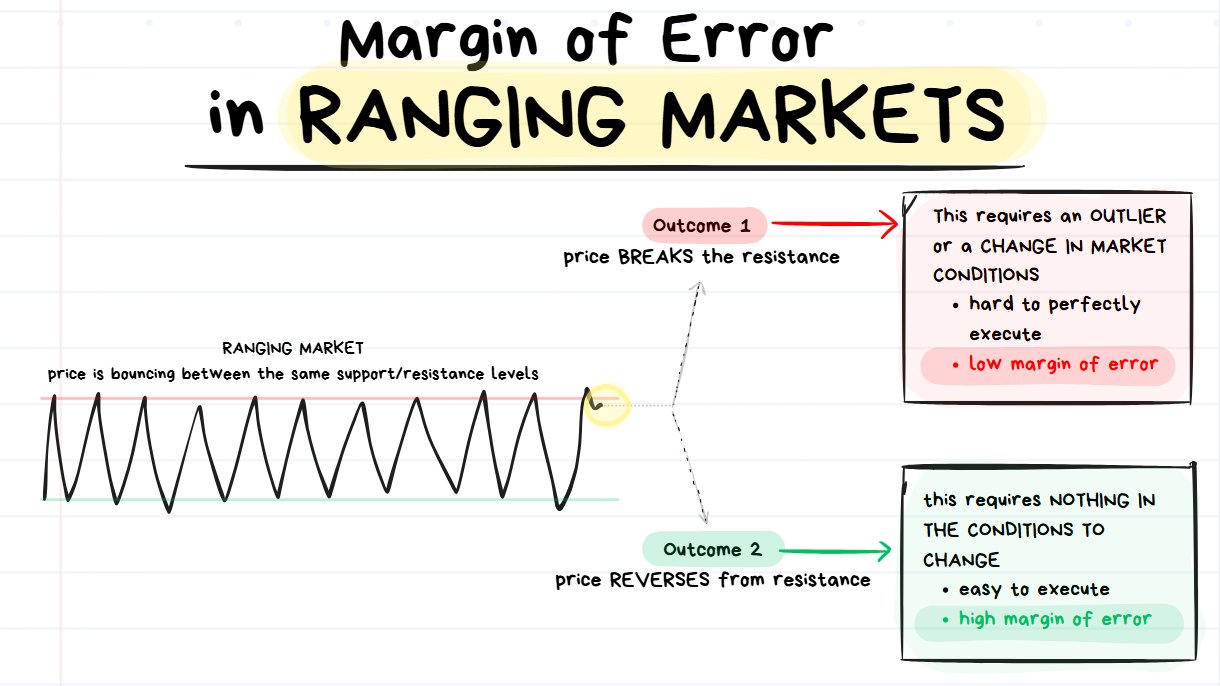

When price is stuck in a range and then approaches a resistance level there are 2 possible things that can happen:

- OUTCOME #1: The market environment changes and price does something COMPLETELY DIFFERENT to before. The price BREAKS the level and shoots upwards. This has a low margin of error.

- OUTCOME #2: Nothing changes in the market environment. Price REVERSES from the level once again and moves down. This has a high margin of error.

Let’s compare the margin of error with playing the reversal and playing the breakout.

🎯Timing the ENTRY:

- Reversals: Whether you played the reversal on the 1st touch of resistance, the 2nd, 3rd, 4th…. 9th…. every single one of them would have been winners.

- Breakouts: If you went for the breakout every single time that price touched the resistance, every single trade would have failed and resulted in a loss.

🎯Timing the EXIT:

- Reversals: Every single trade that was taken as a short from resistance immediately started going down. This means that it doesn’t even matter how the exit is executed, almost every single variation of taking profit would work. “Close after 10 candles” = profitable. “Close once price reaches the next support level” = profitable. “Close at the midpoint of the range” = profitable. “Close with a Trailing SL in profit” = profitable… the point is that every variation of trying to exit the trade would likely work.

- Breakouts: Since every single trade that was taken as a long from resistance immediately started going down, exiting for a profit would be insanely difficult. The only way a trade would exit in profit is if the Trader was catching the small “blip” in price as price wicked through the level and they managed to close it just perfectly in time before it turned around… but even with this method they would be catching tiny scraps. All other variations of trying to exit a Breakout Trade on the previous price action would fail and result in losses.

THE POINT ↓

As we can see, this price action gives A LOT OF ROOM for mistakes when trading reversals and VERY LITTLE ROOM for mistakes when trading breakouts.

A low quality reversal strategy would perform very well in this environment however even a highly optimized breakout strategy would really struggle in this environment.

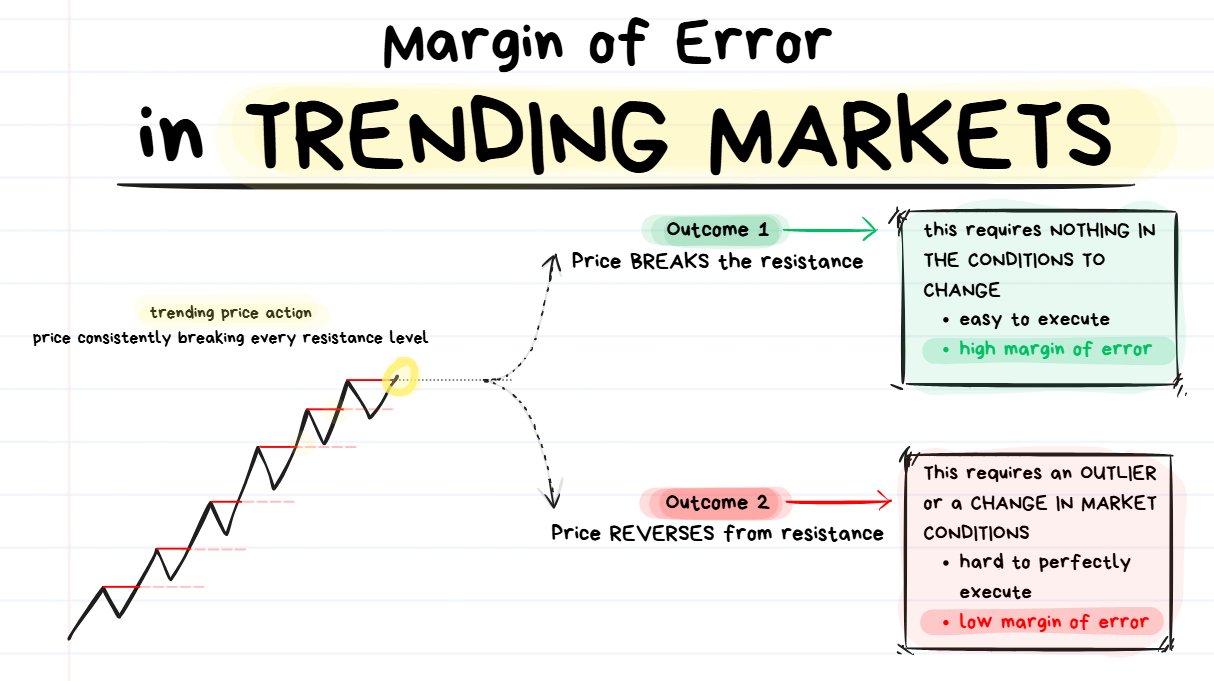

**🤓**NOTE TO READER: The little section below with the Trending Markets might sound a bit repetitive. I just really want to emphasize the point here.

Betting on Outcome #1 is going to be easier than betting on Outcome #2.

When price is consistently trending in 1 direction and then approaches a resistance level there are 2 possible things that can happen:

- OUTCOME #1: The market environment changes and price does something COMPLETELY DIFFERENT to before. The price REVERSES from the level and falls down. This has a low margin of error.

- OUTCOME #2: Nothing changes in the market environment. Price BREAKS the level once again and continues to move upwards. This has a high margin of error.

Just like in the previous example, let’s compare the Margin of Error with both the outcomes.

**🎯**Timing the Entry:

- Breakout: If you entered earlier or later, on the 1st level or the 2nd or 3rd… it wouldn’t matter. Every single time you would have went for the breakout you would have won. The only way you would lose the trade is if the A) the conditions change or B) You get unlucky with an “outlier spike” to the downside.

- Reversals: Every single attempt at shorting the resistance would fail. The only way you could win the next attempt at shorting resistance is if you get lucky with the conditions changing in your favor or if the price randomly spikes down. It will require perfect execution since your entry will need to be based on a “change of conditions” rather than “conditions remaining the same”, which is much more challenging to do.

🎯Timing the Exit:

- Breakouts: Again here even if you were ambitious with the targets or very conservative, you would win all of the breakout trade opportunities on the left. Even if you were looking to exit with a trailing SL or something else like a MA crossover, you would likely exit with a winning trade regardless of what settings you put in your indicator or trailing SL.

- Reversals: Either you would need to go for really perfect/precise tiny winners to snipe the tiny pullbacks (which would be very dangerous and hard to do) or you will need a really clean exit if the conditions were to change. Basically shorting all of the resistances on the left hand side would be very difficult to do successfully.

Summary: Lesson 3

Every trade fits one of three decisions: 1️⃣→ Bet on a breakout (momentum). 2️⃣→ Bet on a bounce (mean reversion). 3️⃣→ Take no trade.

Your job as a Trader: identify the environment and choose the option with the highest margin of error (most room for mistakes).

1. Market Structure

- Bullish: higher highs + higher lows

- Bearish: lower lows + lower highs

- Break of structure: confirmed only when price breaches the most recent swing high/low.

2. Market Environments

A. Mean-Reverting (Ranging)

- Price repeatedly bounces between similar highs/lows.

- ✅ Best for reversals

- ❌ Worst for breakouts

B. Momentum (Trending)

- Price consistently breaks through levels and continues in one direction.

- ✅ Best for breakouts

- ❌ Worst for reversals

3. Margin of Error 🧠

- High margin of error: Easy environment, you can be imperfect and still win.

- Low margin of error: Hard environment, one mistake and you lose. Think poker: playing against drunks (easy) vs pros (hard). You want to trade where mistakes are forgiven.

4. Applying It

In ranges → reversals have high margin of error. In trends → breakouts have high margin of error. Trade with the environment, not against it.

🤓NOTE TO READER: Well done for pushing this far into the article. Just 1 final lesson to go. ↓

Lesson 4: Live Trade Examples + 5 Bonus Resources

So I’m getting really close to the image limit on this Article (yes… X articles have image limits) so unfortunately I can’t ramble on with more theory.

This final Lesson will include:

- Live Trade Examples and Explanations

- 5 Bonus Resources on Price Action related concepts

Live Trade Examples and Explanations

⚠️Quick Disclaimer: I have “cherry-picked” winning trade screenshots below. I can assure you that I do not have a 100% winrate , it’s actually sitting somewhere between 55-60%~.

🤔Quick Context: There are many influencers who say things like “you should only be shorting resistance, longing it is stupid!” Unfortunately they don’t have a clue what they’re talking about. Under specific circumstances (when margin of error is really low) shorting resistance can be a really bad idea. I want to emphasize this with 5 examples below.

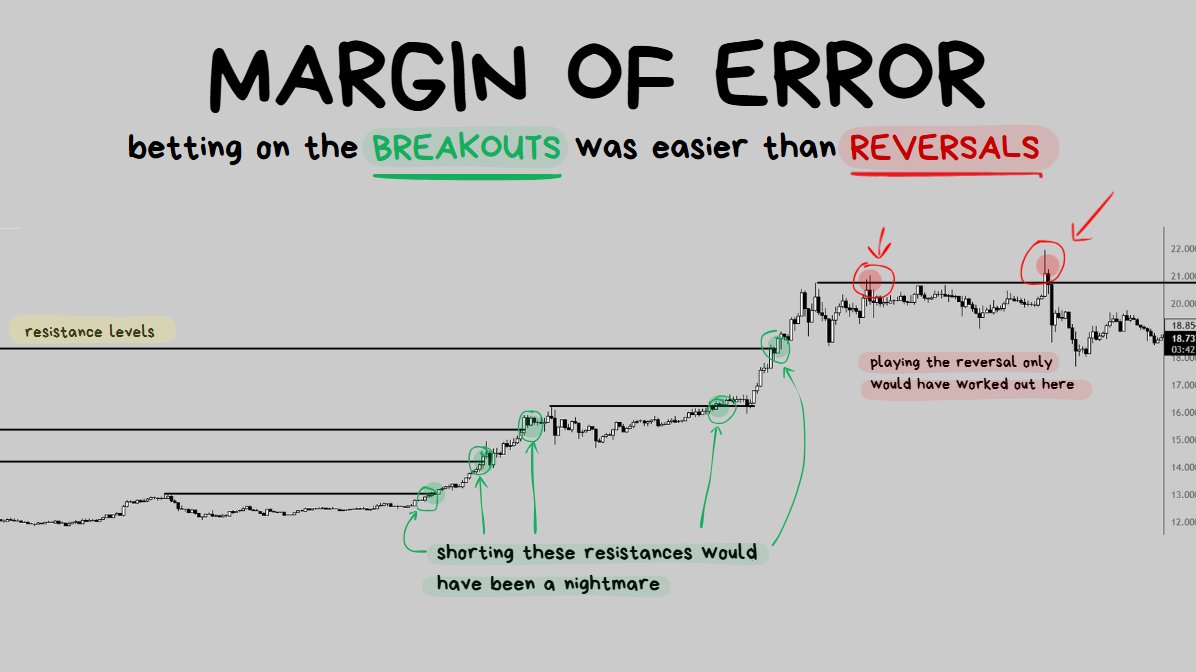

Trade 1: Momentum Long

Jul 18, 2023

target hit +1.99% ty

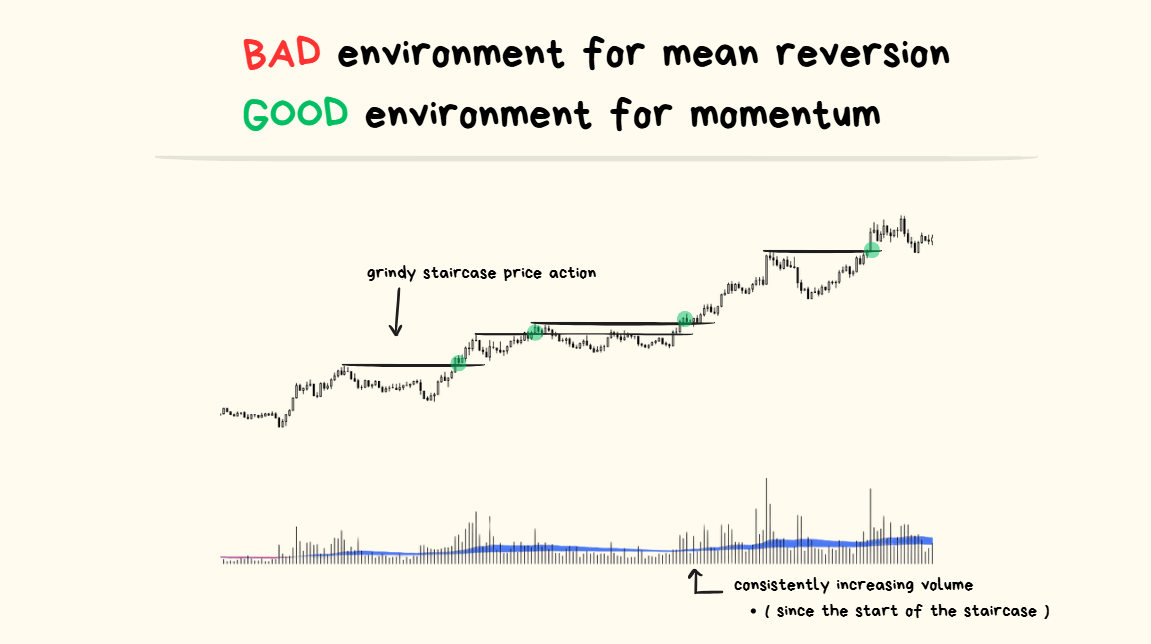

Price was consistently breaking resistances over and over again.

The play here was “whatever was happening, I’m going to bet that nothing is going to change and it’s just going to keep happening.”

Extra Confluences:

- price action looked like a “slow grindy staircase” (good for breakouts, bad for reversals)

- the volume was increasing over time (good for breakouts, bad for reversals)

Trade #2: Momentum Long

Jul 18, 2023

first trade hit target, +1.58% ty, next please

Looks pretty much identical to the trade above:

- Slow grindy staircase price action

- Price breaking out of every visible resistance on the left hand side

- Consistently increasing volume over time

This is a perfect example of “would rather be long until I’m wrong rather than short until I’m right.”

All Traders who were furiously shorting every resistance were not having a fun time during this trend.

Trade #3: Momentum Long

Jun 22, 2023

target hit +5.6% next please

This one is a bit more of a “steeper” and “more extreme” example, but the concept remains the same.

- The market structure was bullish (higher highs and higher lows)

- Price kept slicing through every resistance like a hot knife going through butter

- Volume was consistently increasing over time

Margin of error for breakout trading was very high but for reversals it was very low.

Even if I botched the entry and mistimed the exit the market would have rewarded me… but for trading the reversal I would need absolute perfect and very precise execution.

Trade #4: Momentum Long

Jul 10, 2023

target hit +6.7% tyvm

You must be tired of seeing the exact same price action, same thing in volume, same behavior of price exploding through every visible resistance…

… if yes, then get used to it because this is how consistent execution feels like.

Taking the exact same trade in the same conditions with similar outcomes over and over again.

I’m trying to drill the repetition here to show that these specific scenarios are generally VERY UNFAVORABLE for going for the reversal trade which inversely makes it VERY FAVORABLE to attempt going for the breakout instead.

Trade #5: Momentum Long

Jun 4, 2023

Target hit +1.59% onto the next

Same exact thing. Margin of error is really high on this one.

- I could have entered a few candles earlier, a few candles later…

- I could have exited a little bit earlier or a little bit later

- I could have used a slightly different timeframe

- .. and most of the variations of how this trade could have possibly been taken likely would have ended up as a winner.

Staircase-like price action (cleanly breaking through every resistance) on increasing volume is REALLY NICE for trading breakouts and I will continue to repeat it over and over again.

🤓NOTE TO READER: Hopefully my words and this price action pattern gets tattooed into your memory.

5 Bonus Resources on Price Action

Below I’m going to dump 5 Bonus resources/materials which you may find helpful.

Enjoy! ↓

1. How I trade Breakouts

Jul 31, 2025

2. How I trade Reversals

Oct 1, 2025

3. How I use Crypto Screeners to make it easier to tell if I should be focusing on Breakouts or Reversals

Oct 14, 2025

4. Volume Masterclass

Oct 23, 2025

5. Thread on Price-Action Confirmations

Oct 14, 2025

Trade Entry “Confirmations” I notice traders regularly asking questions about this topic Here’s a small Thread of some Resources: (1/4)

Article Summary

Lesson 1: How Price Actually Moves

- Price moves because of supply and demand, not secret algorithms.

- Makers = limit orders that add liquidity.

- Takers = market orders that consume liquidity.

- When market orders eat through the limit orders at one price, price shifts to the next.

- In short: 👉 Price = the result of market orders hitting the orderbook.

Lesson 2: Support & Resistance

- S/R levels aren’t magical lines, they’re zones where clusters of limit orders sit.

- Price reacts violently when big limit orders are hit.

- It’s not about “strong” or “weak” levels; it’s about how much money is sitting there.

- Round numbers and previous highs/lows attract heavy order flow.

- Key setups: Daily highs/lows = consistent and reactive. 1-hour highs/lows = great for intraday trades.

- 👉 Focus on liquidity clusters, not artistic lines.

Lesson 3: Ranging vs Trending Structure

- Every trade decision = 1️⃣ Bet on a breakout (momentum) 2️⃣ Bet on a bounce (mean reversion) 3️⃣ Don’t trade

- Bullish structure = higher highs/lows. Bearish structure = lower highs/lows. A break in structure = breach of the last swing high/low.

- Ranging markets: best for reversals, worst for breakouts.

- Trending markets: best for breakouts, worst for reversals.

🧠 Margin of Error Concept

- Some environments forgive mistakes; others punish them.

- High margin of error = easy to win even with sloppy execution.

- Low margin of error = need perfect timing.

- Like poker: trading against drunk players (forgiving) vs pros (punishing).

- In ranges → reversals have higher margin of error.

- In trends → breakouts have higher margin of error. 👉 Trade where mistakes are forgiven, not where precision is mandatory.

Lesson 4: Live Trade Examples + 5 Bonus Resources

- Real trades illustrate repetition and consistency: “Same setup, same behavior, same outcome.”

- Breakout longs during trending markets show: Staircase price action. Increasing volume. High margin of error = even imperfect entries/exits work.

- The point: You make consistent money by repeatedly executing the same high-probability setups in forgiving environments.

I am very grateful to you for giving me your Time and Attention, your 2 most valuable assets.

🌶️

Source

Written by @spicyofc · View original post · Published: 2025-09-02

Risk Management Guide for Traders

There are many important things to manage, but nothing is as important as Risk.

I’m a former Prop Trader and I’ve been trading Crypto for 8 Years.

First I want to say thank you for taking time out of your day to click on this article and give it a read. Your time and attention are very valuable resources, so I am grateful for you to give some of it to me.

In exchange, I will give you everything I know about Risk Management.

I have done my best to simplify everything in here for you.

✍️ Let’s get started ↓

Overview

- Lesson 1 ) The Expected Value (EV) Equation

- Lesson 2 ) The Monte Carlo Simulation

- Lesson 3 ) What is Leverage and Liquidation

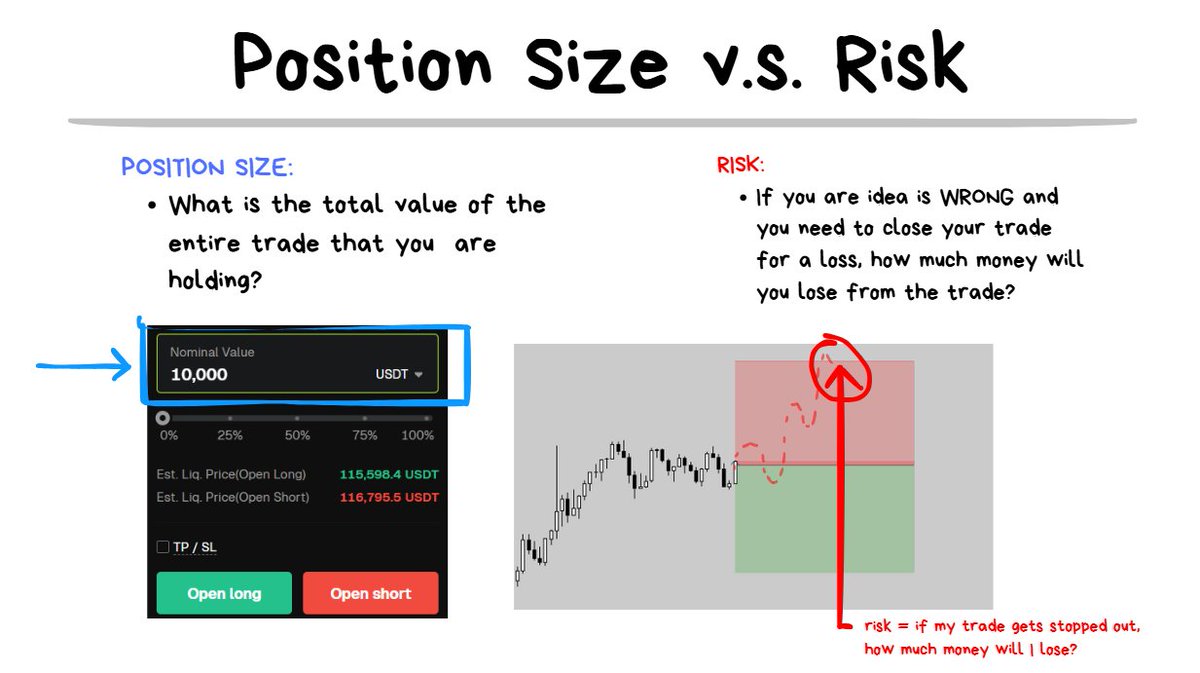

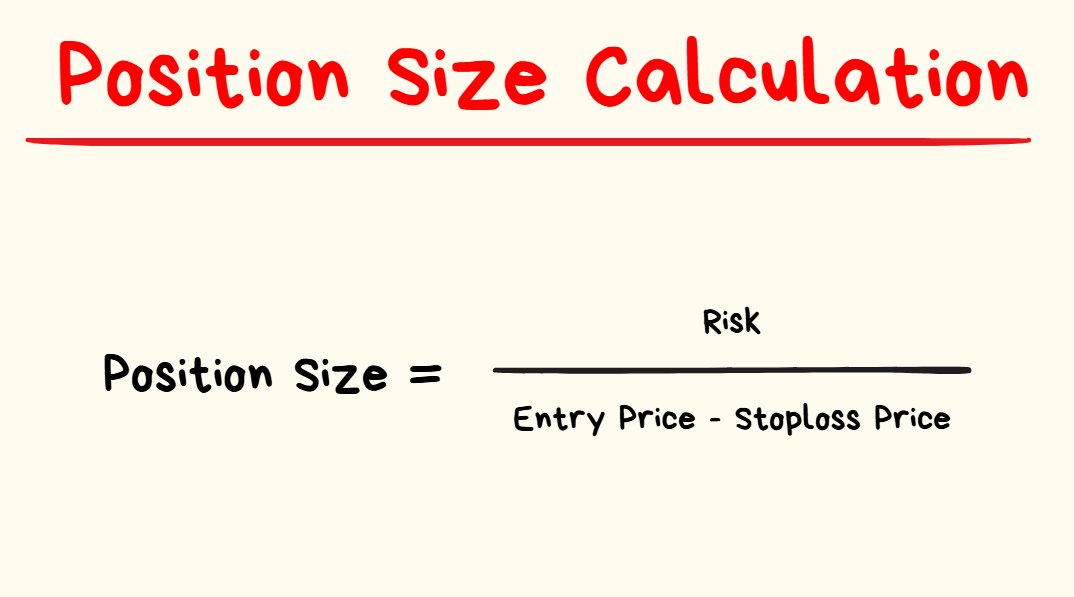

- Lesson 4 ) The difference between “Position Size” and “Risk”

- Lesson 5 ) Risk of Ruin + Good Bet Sizing

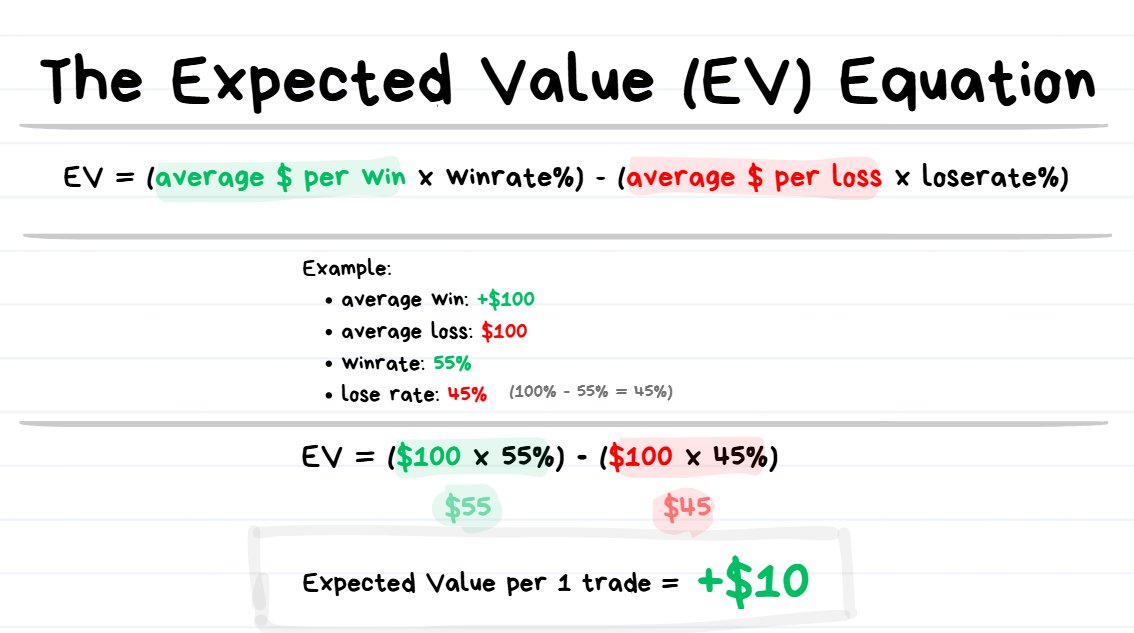

Lesson 1: The Expected Value (EV) Equation

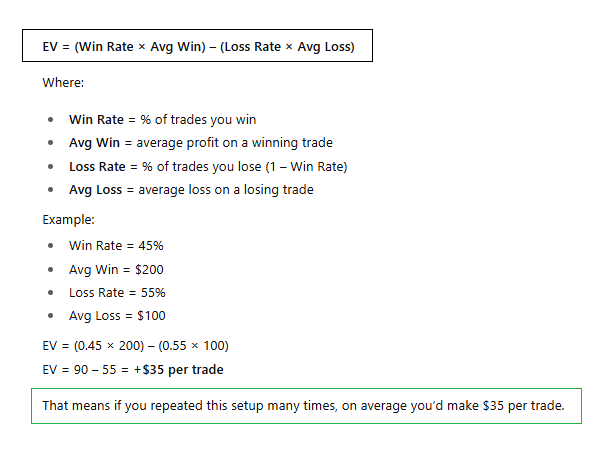

EV= (Average Win x Win%) − (Average Loss x Loss%)

❗️TIP: Expected Value = the average outcome you can expect if you repeated the same decision over and over.

Every single Trader NEEDS to know what Expected Value is and how to calculate it.

🤔Why is EV so important?

- The Expected Value of a Trade allows us to estimate what our expected profit will be over the next N number of trades.

In the image example I shared above, if you have an expected value of +$10 per trade, then if you take 1000 of this exact same trade then your average “expected profit” should be roughly $10 x 1000 = $10,000.

- If you have a POSITIVE EXPECTED VALUE (+EV) , your trades will win money over time.

- If you have a NEGATIVE EXPECTED VALUE (-EV), your trades will lose money over time.

In the section below I will talk about the Monte Carlo Simulation which helps visualize this. ↓

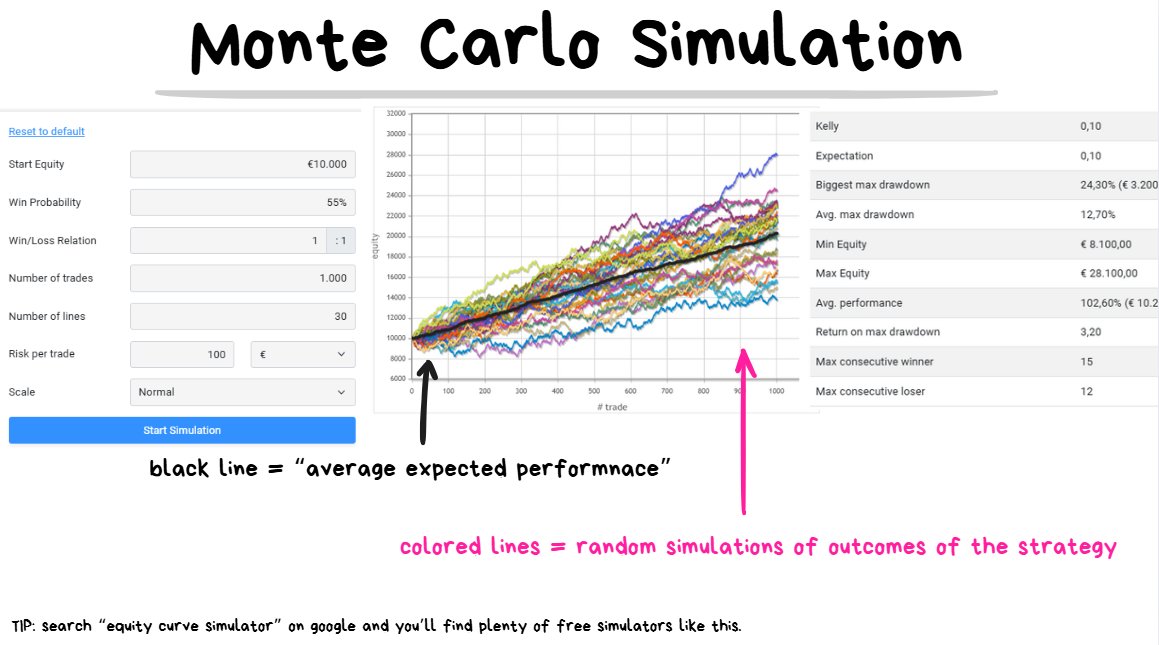

Lesson 2: The Monte Carlo Simulation

In this Lesson I’m going to cover a few things:

- The Monte Carlo Simulation

- Variance

- The Law of Large Numbers

- How these 3 things above related to Trading

This might look scary because of numbers, fancy names and graphs, but I promise it’s fairly simple to understand.

I believe having a basic understanding of these 3 topics will make everything to do with Risk Management easier to digest.

First let’s quickly cover the Monte Carlo Simulation ↓

30 simulations of how performance can look like with a 55% winrate, 1R strategy over the next 1000 trades. This is a profitable (+EV) strategy.

❗️TIP: Monte Carlo simulation = running lots of random “what if” scenarios to see all the possible outcomes after taking N number of trades.

A Monte Carlo Simulation can help us manage expectations and also give us a rough idea for how profitable our strategy is.

We input our starting balance, winrate %, average win/loss ratio and the # of trades, and the simulation will spit out random combinations for how our performance can look like.

The thick black line visualizes the “average expected outcome”.

So if our EV per trade is +$10 and we take 100 trades, our total profit will be “roughly” +$1000~ . If we take 1000 trades with the same strategy then our total profit will be “roughly” +$10,000.

Notice the emphasis on the word “roughly”. This is because it cannot be guaranteed and there can be a bit of variance.

Secondly, let’s quickly talk about Variance ↓

“Randomness” plays a role in our trading performance, whether we like it or not.

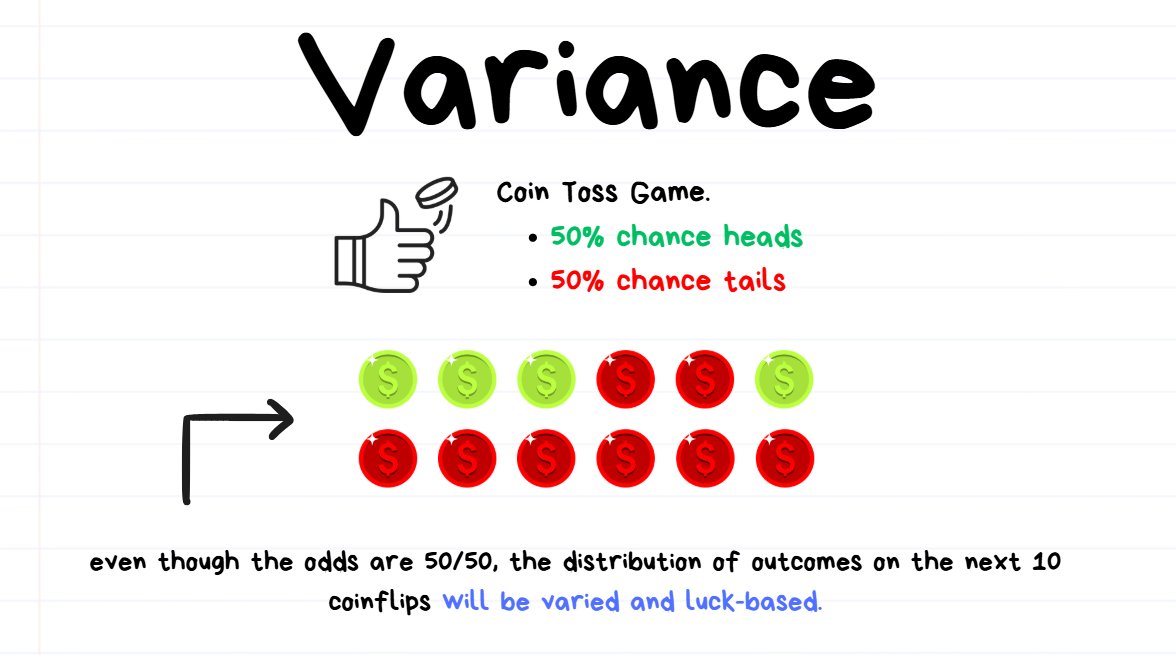

🧠Here is a Coin Flip analogy

- Imagine you are playing a Coin Toss game with a 50% chance of getting either heads or tails.

- If you flip the coin 10 times, it is possible to get heads 8 times and tails 2 times. Despite the chance of landing on heads is 50%, it landed on heads 80% of the time.

- This DOES NOT mean that the coin is rigged and has a 80% chance of landing on heads.

- It just simply means that the coin has not been flipped enough times for the probabilities to properly play out.

- The difference between “actual outcome” (80%) and “probability” (50%) is the variance (80% - 50% = 30%)

- If you were to flip the coin 10,000 times, you might get 5050 heads and 4950 tails. Even though the the raw difference is +50 more heads than expected, in percentage terms there is only 0.5% (50 ÷ 10000) of variance.

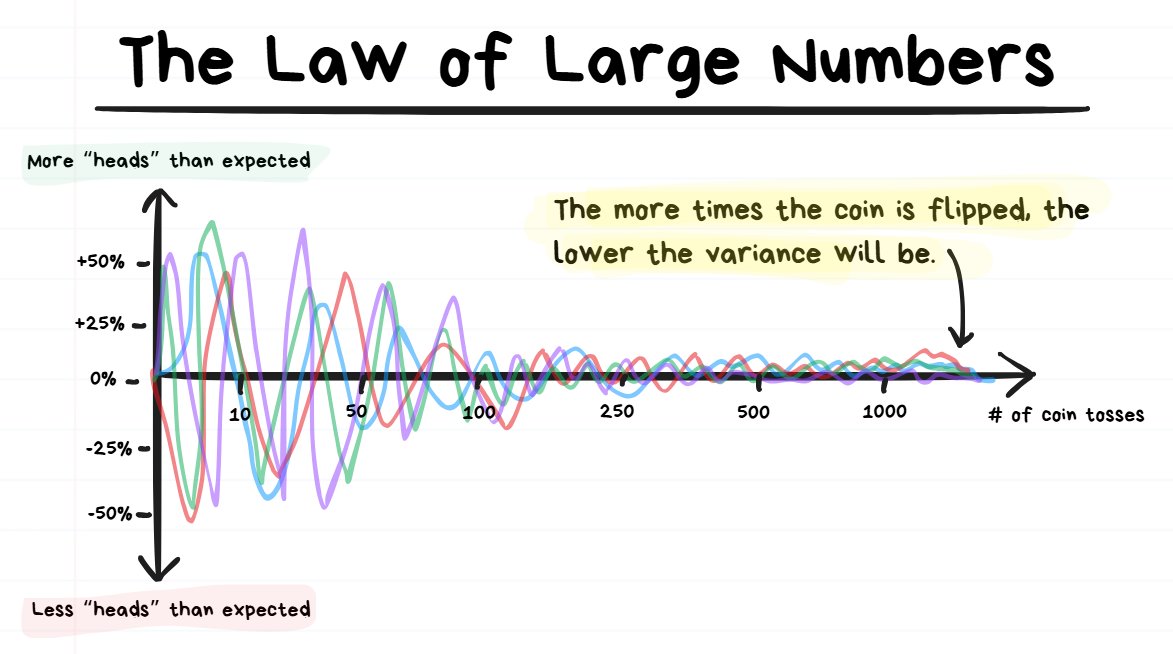

Thirdly, let’s quickly discuss The Law of Large Numbers ↓

The more times that a coin is tossed, the closer the Variance gets to 0.

❗️TIP: The “Law of large numbers” means the more times you repeat something random, the closer your results get to the true average.

If you play the coin toss game only 10 times, there is going to be a lot of variance in the % of times that the coin landed on heads.

If you play the coin toss game 10,000+ times, there is going to be very little variance in the % of times that the coin landed on heads.

Basically the more you times an event happens, the closer the outcomes will start to move towards the “real probability”.

How does a Monte Carlo Simulation, Variance and Law of Large numbers all relate to Trading?

The Monte Carlo Simulation allows us to manage our expectations (baed on the variance) over how our next N number of trades are going to play out. The more trades taken, the less variance we can expect.

- How much expected profit should we see after N trades?

- How many consecutive wins we can expect to see?

- How many consecutive losses can we expect to see?

- How much of our account is it “normal” to lose with this kind of winrate and risk/reward ratio after N trades?

It’s also a “slap-in-the-face” reality check about certain truths:

- Even highly profitable strategies can go through extended periods of drawdown. (Drawdown = how much % have you lost in the account)

- Even high win-rate strategies can go on large consecutive lose streaks.

- Even terrible, low win-rate strategies can go on large consecutive win streaks.

- The outcome of the next trade we take DOES NOT MATTER. What matters is the outcome of the next 100+ trades we take.

The Main Takeaway

→ Sometimes you’ll make a good trade and lose.

→ Sometimes you’ll make a bad trade and win.

It’s going to happen because of variance/luck.

Judging whether or not you made the good trade based on 1 outcome is not the way to go.

Two Extreme Examples ↓:

- You take a trade based on a pattern which has a 90% success rate with a Risk/Reward ratio of 1: If you take the trade and it loses, it was still the right call. This is because if you were take the same trade 1000+ times and let the law of large numbers play out, you would be printing money. ✅

- Playing at a Slot Machine in a Casino: If you win once, that doesn’t make it a smart bet. You just got lucky due to variance. If you keep betting 1000+ times and let the law of large numbers play out, then you would get wiped out for all of your funds. ❌

The point: Don’t judge your trade quality based on whether the next trade is a win/loss. Instead judge them by their expectancy. You will need to be patient and sit through some variance before the profits start rolling in.

Lesson 3: What Is Leverage and Liquidation?

Leverage is probably one of the most misunderstood concepts for Traders.

🤓QUICK NOTE TO READER: Before reading everything below I want to make it clear that you DO NOT have to remember every single thing below, so don’t stress.

As long as you get a “basic understanding” of what leverage is, you’ll be fine.

👨🎓 Mini Test: Do You Understand Leverage?

(assume the entry price of both traders is the same)

What most people think Leverage is (but it is DEFINITELY NOT this ❌):

- A turbo profit multiplier, such when you slide it up it magically increases how much money you’re going to make on the trade.

- I promise you, leverage is NOT this.

What Leverage ACTUALLY is ✅****:

- A tool to reduce counterparty risk and also improve capital efficiency.

- Counterparty Risk = the funds that you risk by holding on an exchange. It is at risk because there is non-zero chance of the exchange rugging/scamming (e.g. FTX).

- Capital Efficiency = how efficiently you can use your money to generate more money. For Example: Needing $1000 of capital to make $1000/month is 100x more efficient than needing $100,000 of capital to make $1000/month.

🤓Before going further, let’s first get some clear definitions on some terms. Then we can return to learning more about Leverage. ↓

- Trading Account Balance: the total capital you are willing to use to execute trades.

- Exchange Account Balance: the amount of money you have deposited onto the exchange. This is naturally going to be a small % of what your entire trading account is. It is not recommended to have your all 100% of your entire trading account deposited onto an exchange.

- Margin: The required money that you need to put up in order to open a trade.

- Leverage: The multiplier of the money that you are borrowing from the exchange.

- Position Size: The total amount of whatever coin that you opened a trade in.

🤓NOTE TO READER: below is a post which shows a flow chart for how I manage deposits/withdrawals from exchanges. The point is to never be “over-exposed” on 1 exchange.

Aug 31, 2025

Serious Traders don’t keep 100% of their funds on an exchange. Leverage is a gift which allows using trading capital without needing to deposit it. Below is the system I use for topping up and withdrawing profits from CEX exchanges as an Altcoin Perp scalper ↓

Example: Leverage in Practice

Pretend you have $10,000 that you are willing to trade with. This is your Trading Account Balance.

You don’t want to deposit all $10,000 onto an exchange because what if the exchange decides to hold our funds, scam/rug or it gets hacked. So instead you deposit 10% of these funds onto the exchange. So $1000 gets deposited onto the exchange. Your Exchange Account Balance is now $1000.

You see a good trade opportunity in BTC and you want to long $10,000 worth of it. If you try to click “Buy”, it will say insufficient funds. Since you only have $1000 in your Exchange Account Balance, you will need to use Leverage to get the required funds to open the position.

- So you put the Leverage to 10x and then you try again and it works.

- Your Position Size (how much of the coin did you actually buy) on the Trade is $10,000.

- Your Margin (how much money did you need to put up “as collateral”) is $1000.

- Your Leverage is 10x.

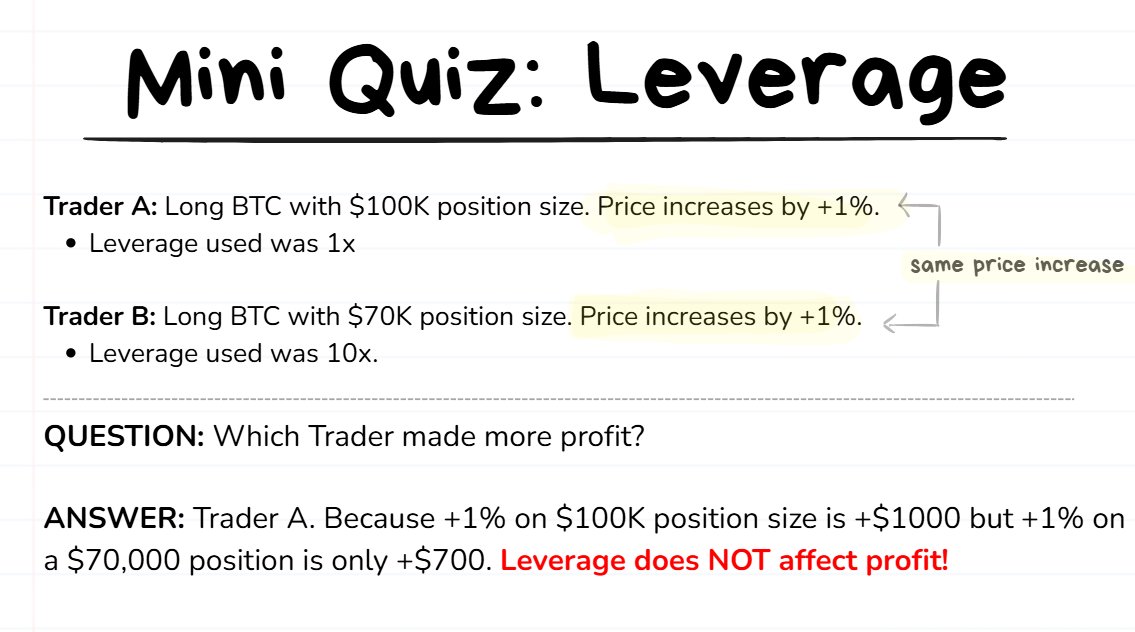

❗️TIP: The profit on a $10,000 position with 1x leverage or 100x leverage is going to be exactly the same. A $10,000 position will always just be a $10,000 position. You can change the leverage of a trade literally while in the trade, and it won’t do anything to the profit.

The Purpose of Liquidation

When you are getting leverage on a position, you are basically “borrowing” from the exchange. The money isn’t magically coming out of thin air 😂.